Event Reminder | Get Ready for 3:30 PM - 5:00 PM Today (Tuesday, July 14th)

Jpmorgan Chase JPM-A | 0.00 | |

Citigroup Inc. C | 0.00 | |

Bank of America Corp BAC | 0.00 | |

Goldman Sachs Group, Inc. GS | 0.00 | |

Morgan Stanley MS | 0.00 |

Tonight’s Dual Test

Markets are bracing for a packed Tuesday in Washington.

At 3:30 PM Riyadh time, Tuesday, the Bureau of Labor Statistics releases the June CPI report — the first monthly print since the Iran-war oil spike began to reverse, and arguably the single most consequential data point for the Fed’s July 29 decision now that the central bank’s focus has visibly tilted from employment back to stubborn inflation.

Roughly ninety minutes later at 5:00 PM Riyadh time, Fed Chair Kevin Warsh opens two days of semi-annual congressional testimony, starting with the House Financial Services Committee, followed by the Senate on Wednesday morning alongside the June PPI release.

| Time (Riyadh) | Indicator | Previous | Consensus | Forecast |

|---|---|---|---|---|

| 03:15 PM | ADP Employment Change Weekly | 21.0K | ||

| 03:30 PM | Core Inflation Rate MoM JUN | 0.2% | 0.2% | 0.2% |

| 03:30 PM | Core Inflation Rate YoY JUN | 2.9% | 2.9% | 2.9% |

| 03:30 PM | Inflation Rate MoM JUN | 0.5% | -0.1% | 0.0% |

| 03:30 PM | Inflation Rate YoY JUN | 4.2% | 3.8% | 3.9% |

| 03:30 PM | CPI JUN | 335.12 | 334.71 | |

| 03:30 PM | CPI s.a JUN | 333.979 | 334 | |

| 03:55 PM | Redbook YoY JUL/11 | 11.5% | ||

| 05:00 PM | Fed Chair Warsh Testimony | |||

| 06:30 PM | 6-Week Bill Auction | 3.635% |

The timing is deliberate:

CPI lands hours before Warsh faces lawmakers, meaning the report will either arm him with ammunition to sound tougher or force him to explain why the "price stability" pledge he doubled down on in last week’s semi-annual monetary policy report hasn’t yet translated into action.

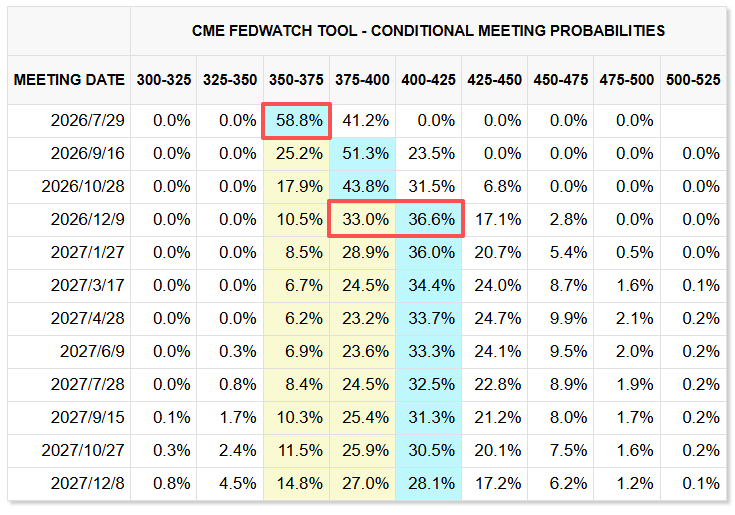

Futures pricing currently shows a July hike near 41.2%, up from under 40% early Monday after the US weekend air strikes on Iran and renewed threats around the Strait of Hormuz; by year-end, the combined probability of at least one 25bp or 50bp hike sits around 70% per CME FedWatch, with two hikes now the modal scenario.

What to Expect

The street consensus pencils in 3.8% y/y for headline CPI (down from 4.2% in May) and -0.1% m/m — the first negative monthly print since the pandemic’s 2020 onset, driven by gasoline, which AAA data show has dropped 76 cents/gallon (-17%) since the May 20 peak.

June US CPI YoY (Unadjusted)

| Forecast Value | Institutions |

|---|---|

| +3.7% | JPMorgan Chase, RBC, Standard Chartered, TD Securities, Jefferies, UBS, Wells Fargo |

| +3.8% | Citibank, Bank of America, Barclays, Union Bank, HSBC, ING, Nomura, Morgan Stanley, Deutsche Bank |

| +3.9% | Pantheon Macroeconomics, ABN AMRO, BNP Paribas, Goldman Sachs, Helaba, Capital Economics, Société Générale, UniCredit, Lloyds Bank, BMO |

| +4.0% | Berenberg, DBS Bank, SMBC, Scotiabank |

Natixis’s Christopher Hodge captures the framing: inflation breadth is near historic norms, the Iran energy shock hasn’t bled widely into core goods, but the pressure is "weak and transitory" at best.

Core is where the debate lives.

June US Core CPI YoY (Unadjusted)

| Forecast Value | Institutions |

|---|---|

| +2.7% | Deutsche Bank |

| +2.8% | ABN AMRO, Citibank, Union Bank, Goldman Sachs, HSBC, JPMorgan Chase, Nomura, Pantheon Macroeconomics, Jefferies, Société Générale, TD Securities, UBS, Wells Fargo, Morgan Stanley |

| +2.9% | Bank of America, Capital Economics, ING, SMBC, Danske Bank, Scotiabank, Standard Chartered, UniCredit, Helaba |

| +3.0% | BNP Paribas |

Consensus looks for +0.2% m/m and +2.8% y/y (vs. 2.9% prior).

Goldman Sachs goes slightly softer at +0.17% m/m, flagging four sub-components: soft autos, tame housing, modest travel-services uptick, and residual seasonal drags.

But upside channels are building. The Fed’s own June minutes flagged AI capex, the Iran war and tariffs as the trio of forces keeping inflation sticky. Governor Chris Waller, speaking Monday in New York, laid down the clearest line in the sand: if core comes in hot again this week, the FOMC will need to consider tightening "in the near term."

Then there’s Warsh’s testimony.

Since taking over, he has scrapped forward guidance, skipped his dot-plot, cut the June statement to ~130 words, and kept public speeches to 18 since the meeting vs. 49 a year ago.

The June minutes showed "quite a divide" on the rate path but little clarity on Warsh’s own reaction function.

What markets want tonight isn’t forward guidance — he’s made clear he won’t give it — but a readable mapping of how he’ll move rates when inflation, oil and tariffs all shift.

Equity Impacts

The cross-currents for stocks are unusually messy.

Q2 earnings kick off this week with Jpmorgan Chase(JPM-A.US), Citigroup Inc.(C.US), Bank of America Corp(BAC.US), Goldman Sachs Group, Inc.(GS.US), Morgan Stanley(MS.US) and Wells Fargo & Company(WFC.US), plus ASML Holding NV ADR(ASML.US) and TSMC Supply Chain(UB1552.US) giving a fresh read on the AI trade — a potential offset if results impress.

But high-frequency rate repricing is the nearer threat.

Goldman’s Ben Snider runs the history:

Over the past seven Fed hiking-cycle initiations, the S&P 500 averaged a ~2% decline over the following three months, with 1997’s one-and-done 25bp hike still producing a ~10% drawdown before a three-month bounce.

Since 1995, when markets first price in at least 25bp of hikes, the S&P’s three-month average and median returns both sit near zero.

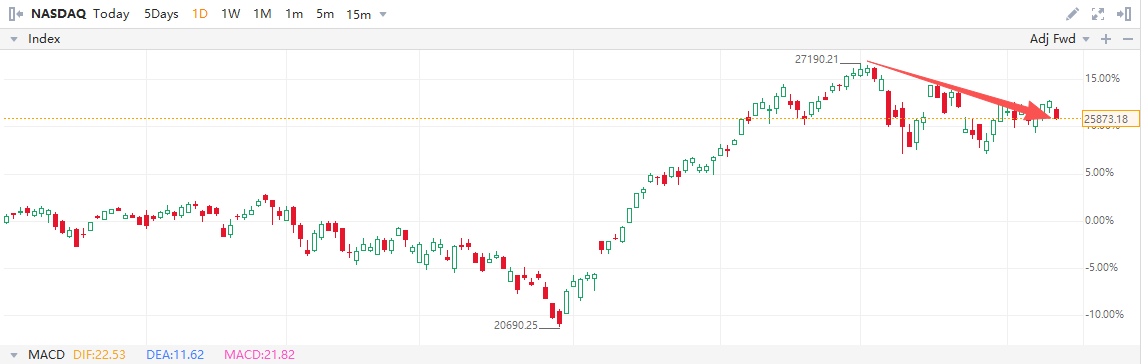

The vulnerability this time is the AI complex itself.

Goldman estimates AI-related names account for 42% of S&P 500 index(SPX.US) market cap and 38% of 2026e EPS; hyperscalers have ramped debt issuance and capex, making cost of capital matter more than in any prior cycle.

If Treasury volatility reverts to 2022–23 tightening-period levels, Goldman sees the S&P’s P/E compressing ~6%.

Sector-wise, IT has historically outperformed when hike pricing first emerges, financials lag, and balance-sheet-weak names with floating-rate exposure are most exposed.

The path dependency is straightforward:

- A soft core print (~0.15–0.18% m/m) + Warsh offering even a vague reaction-function sketch likely cools July hike pricing back toward 30–35%, giving equities and rates-sensitive tech room to breathe into bank earnings.

- A hot core (≥0.25% m/m) + Warsh staying opaque or leaning into "price stability" hawkishness pushes July to coin-flip or beyond, with the S&P retesting the 2–3% drawdown zone Goldman’s template implies, and AI-heavy names disproportionately hit.

- The oil variable sits atop everything: if Strait of Hormuz stays live, even a soft June CPI gets overwritten by July’s rebound risk, and Warsh’s testimony will be parsed less for what he says about June and more for whether he sounds willing to move before September.