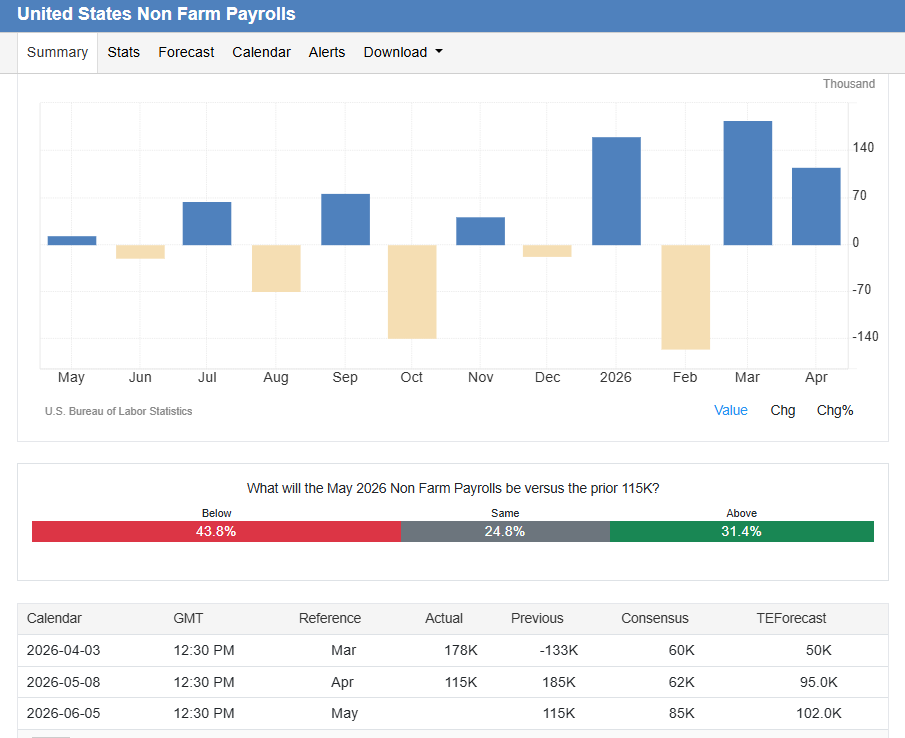

Later today the US Bureau of Labor Statistics releases the May nonfarm payrolls report—the first official monthly employment “report card” Kevin Warsh will review as Fed chair after his White House swearing-in this week.

The latest run of indicators suggests the balance may finally be tilting toward something more constructive, though still fragile.

Consensus looks for May payrolls to rise about 85k after April’s +115k, with the unemployment rate seen holding at 4.3% and average hourly earnings up +0.3% m/m (y/y easing to roughly 3.4%).

Time (Riyadh)

Indicator

Previous

Consensus

Forecast

03:30 PM

Non-Farm Payrolls MAY

115K

85K

102.0K

03:30 PM

Unemployment Rate MAY

4.3%

4.3%

4.4%

03:30 PM

Average Hourly Earnings MoM MAY

0.2%

0.3%

0.2%

03:30 PM

Average Hourly Earnings YoY MAY

3.6%

3.4%

3.5%

03:30 PM

Participation Rate MAY

61.8%

61.7%

03:30 PM

Average Weekly Hours MAY

34.3

34.3

34.3

03:30 PM

Government Payrolls MAY

-8K

9.0K

03:30 PM

Manufacturing Payrolls MAY

-2K

2K

3.0K

03:30 PM

Nonfarm Payrolls Private MAY

123K

85K

93.0K

03:30 PM

U-6 Unemployment Rate MAY

8.2%

8.3%

04:00 PM

Used Car Prices MoM MAY

-1.6%

04:00 PM

Used Car Prices YoY MAY

1.8%

The Fed’s problem is no longer wage-fueled overheating; it is supply-shock inflation from the Middle East conflict. That framing keeps the labor market data in a dual role:

It must confirm enough momentum to avoid a “stagnation” scare, yet not so much that it emboldens an already restless bond market repricing the chance of further tightening.

What to Expect—and How to Read the Prints

Readers should treat the May number as a composition story rather than a simple headline beat/miss.

Forecasters span a wide range—from +45k (Freedom Finance) up to +125k (Jefferies)—with models like Goldman Sachs tracking softer big-data signals near +60k and others flagging downside if Q1’s weather lift “recycles.” A print near consensus would be consistent with Chicago Fed-type trackers that see unemployment essentially flatlining around 4.3–4.32%.

Two previews complicate the narrative in opposite directions.

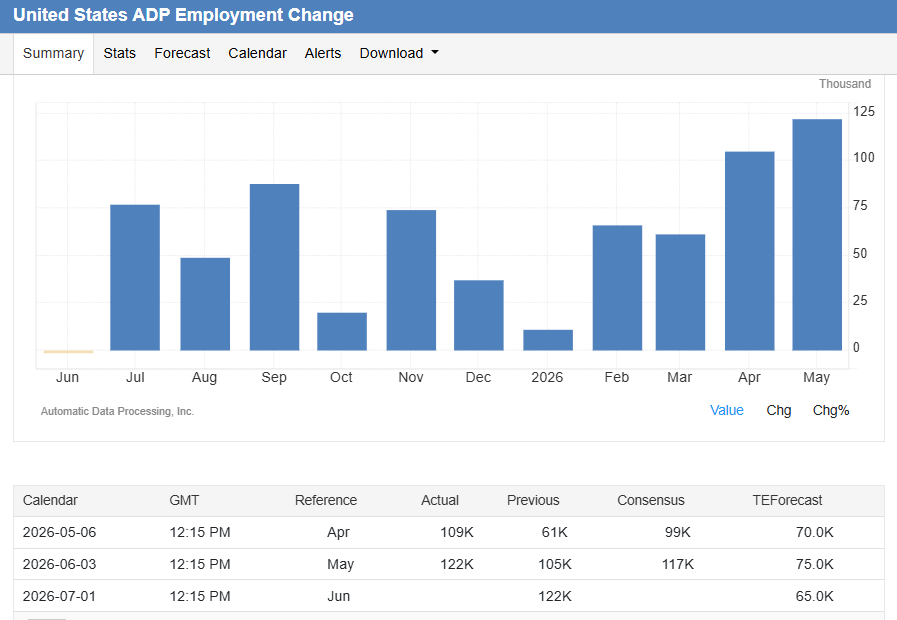

On the upside, ADP showed private employment up +122k in May—the strongest since January 2025—broad-based across education/health (+57k) and trade/transport/utilities (+36k), with job-stayer pay up 4.4% y/y.

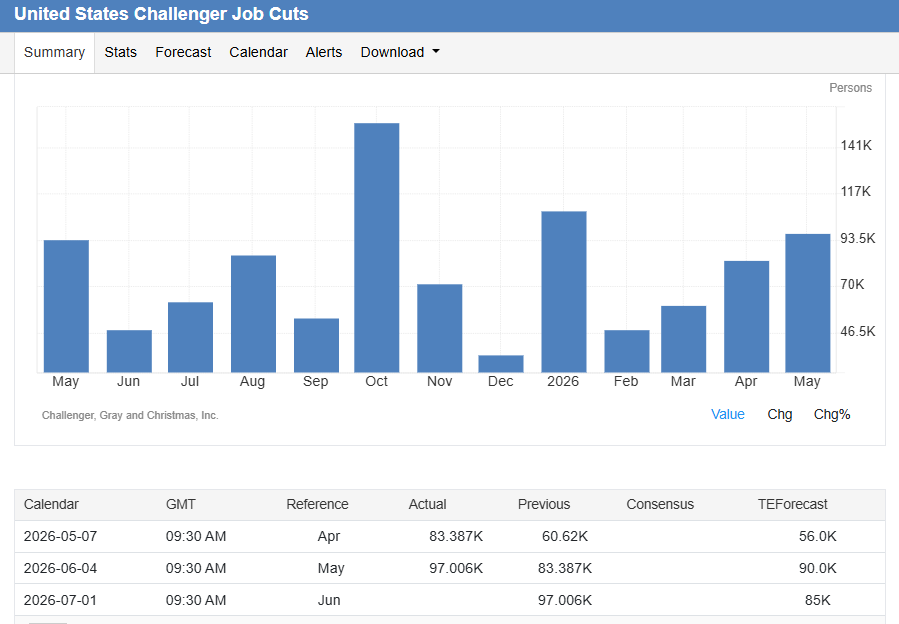

On the downside, Challenger data warned that announced layoffs hit 97,006 in May, a May high since 2020, with AI cited as the leading stated reason for cuts for a third straight month (roughly 38,579 AI-related announcements).

The message for interpretation is straightforward:

If payrolls land near +85k but the unemployment rate holds and hours/wages don’t re-accelerate, officials will call it a “stable, slightly improving” labor market that doesn’t force their hand.

If payrolls jump toward +100k–+130k, markets will care less about the “growth is good” angle and more about whether that strength shows up alongside stickier price expectations born of energy and tariff-related cost pressures.

Conversely, a sub -40k print wouldn’t necessarily scream recession in a supply-constrained market, but it would revive the uglier “zero-hire, eventual wider layoffs” fear—especially with AI-driven restructuring already visible in tech.

Impact on Equity Sentiment and the Rates Backdrop

For equities, the takeaway from desks like JPMorgan’s scenario mapping is asymmetric:

The “best” zone for risk assets is a solid-but-not-hot print around +70k to +100k, where growth looks alive yet doesn’t pour gasoline on the inflation/rates move higher. Roughly, they assign the highest win-probability (around 40%) to the +70k to +100k bucket, with a modest positive reaction;

Outcomes above +130k lean toward yield/curve sensitivity and valuation pushback;

Outcomes below +40k risk a stagflationary “growth scare” bid for defensives and a drag on cyclicals.

In short: stronger is not automatically better once the tape starts worrying about the next Fed move rather than the last one.

Why rates matter here:

Futures still imply the June 16–17 FOMC is effectively locked (no move expected), but the market has already edged toward pricing a 25bp hike by next March, and Fed commentary—including voting-FOMC hawks and the Beige Book—has openly kept “further tightening” on the table if inflation proves stickier.

That makes the payrolls report less about triggering an immediate hike and more about validating or undermining the hike-premium already building in the long end.