Event Reminder | Get Ready for 3:30 PM Today (Friday, May 8th)

S&P 500 index SPX | 0.00 | |

NASDAQ IXIC | 0.00 | |

Dow Jones Industrial Average DJI | 0.00 | |

NASDAQ-100 NDX | 0.00 | |

S&P 500 index GSPC | 0.00 |

01

Event Report and Background

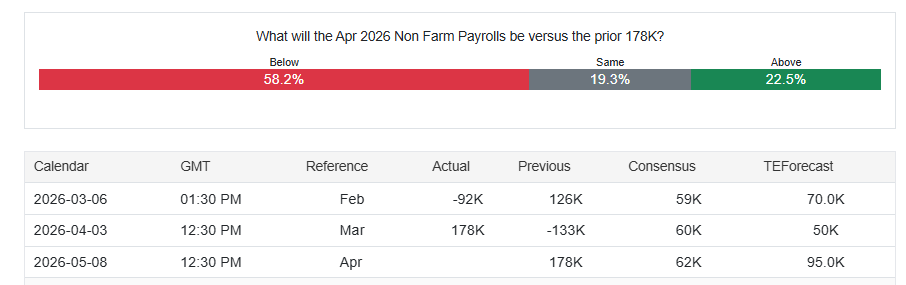

The US Bureau of Labor Statistics will release the April employment report on Friday, May 8, 2026, at 8:30 AM ET.

| Time (Riyadh) | Indicator | Previous | Consensus | Forecast |

|---|---|---|---|---|

| 03:30 PM | Non-Farm Payrolls APR | 178K | 62K | 95.0K |

| 03:30 PM | Unemployment Rate APR | 4.3% | 4.3% | 4.3% |

| 03:30 PM | Average Hourly Earnings MoM APR | 0.2% | 0.3% | 0.2% |

| 03:30 PM | Average Hourly Earnings YoY APR | 3.5% | 3.8% | 3.6% |

| 03:30 PM | Participation Rate APR | 61.9% | 61.7% | |

| 03:30 PM | Average Weekly Hours APR | 34.2 | 34.2 | 34.2 |

| 03:30 PM | Government Payrolls APR | -8K | -12.0K | |

| 03:30 PM | Manufacturing Payrolls APR | 15K | 5K | 8.0K |

| 03:30 PM | Nonfarm Payrolls Private APR | 186K | 75K | 83.0K |

| 03:30 PM | U-6 Unemployment Rate APR | 8% | 8.0% |

This key labor market snapshot arrives amidst a complex economic landscape shaped by persistent inflation, ongoing geopolitical tensions, and emerging signs of a structural transformation within the job market itself.

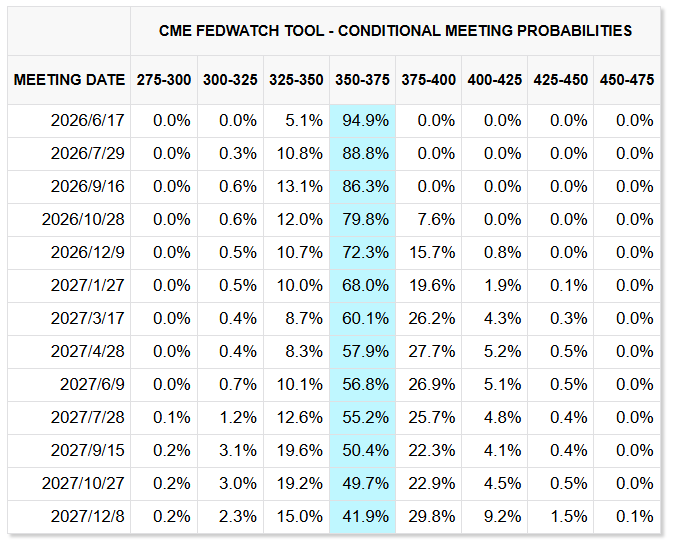

The report's significance is heightened as markets continue to digest the implications of the Personal Consumption Expenditures (PCE) data released the prior day, which reinforced the Federal Reserve's resolve to maintain a restrictive monetary policy stance for an extended period.

The backdrop is one of apparent contradiction.

The US labor market is frequently described as robust and resilient, yet underlying data reveals profound changes. Economists note the market is undergoing a structural remake, moving away from its pre-2020 growth trajectory due to demographic aging, significantly reduced net immigration, and the accelerating integration of artificial intelligence (AI), which is beginning to reshape job functions and industry landscapes.

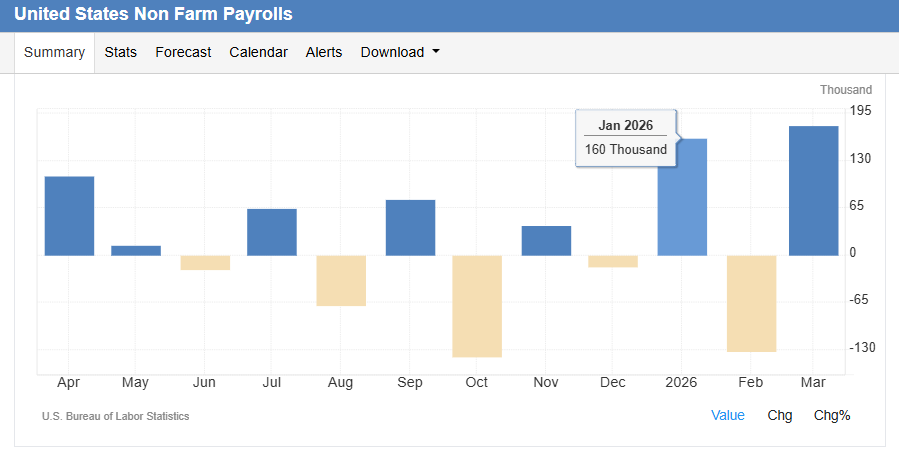

This has resulted in a volatile monthly nonfarm payroll print in early 2026, with January adding approximately 160,000 jobs, February losing 133,000, and March rebounding with a gain of 178,000. The three-month average through March stands at 68,333.

02

Expectations and Interpretation

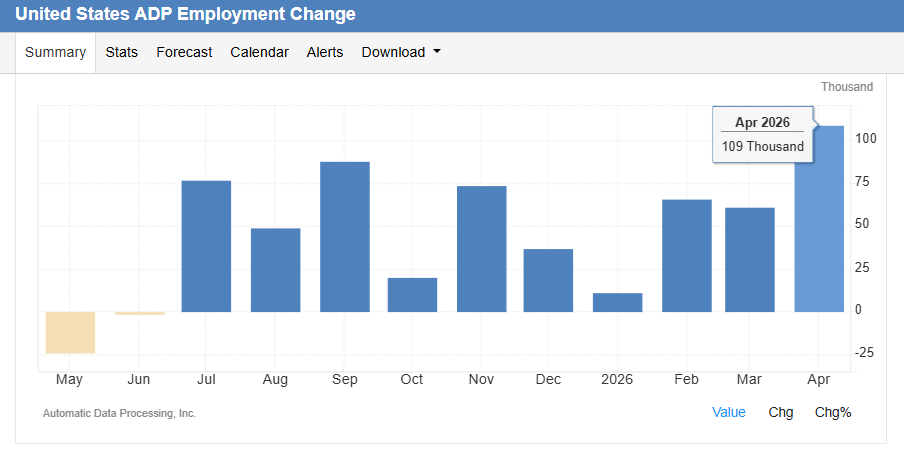

The recent ADP National Employment Report, a separate measure of private-sector payrolls, showed an addition of 109,000 jobs in April, marking the fastest pace of hiring since January 2025. However, the ADP report covers only the private sector and uses a different methodology, meaning it does not directly forecast the government's broader nonfarm payrolls figure.

The consensus for nonfarm payroll, on the other hand, among economists surveyed forecasts that the US economy added 67,000 nonfarm payrolls in April, with the unemployment rate expected to hold steady at 4.3%. This anticipated figure, roughly one-third of March's increase, may appear weak on the surface. However, analysts caution against overinterpreting a single month's data given the current volatility and advise focusing on the smoothed trend. An addition of 67,000 jobs would align closely with the recent three-month average.

The interpretation of the headline number will be nuanced. Economists point to a significantly lowered "breakeven" rate of job growth needed to keep unemployment stable—now estimated to be as low as 25,000 per month—due to the aforementioned structural headwinds of demographics and immigration. Therefore, a gain near 70,000 would be viewed as solid, resilient, and consistent with a labor market that is stabilizing at a slower, more sustainable pace of growth. Gregory Daco of EY-Parthenon notes that such a figure would still be above the long-term trend and sufficient to potentially lower the unemployment rate slightly.

Market participants will dissect the report's internals with equal vigor.

The strength of service-providing sectors, particularly education and health services which led the ADP gains, will be watched versus goods-producing industries. Wage growth, as measured by average hourly earnings, will be a critical variable.

Combined with the still-elevated PCE inflation reading, strong wage growth would underscore persistent inflationary pressures, reinforcing the "higher-for-longer" interest rate narrative.

Conversely, a moderation in wage gains could offer the Fed a glimmer of hope that labor market cooling is helping to ease price pressures.

03

Impact on Market Sentiment

The equity market's reaction will likely be bifurcated and highly sensitive to the wage component.

A report that meets or modestly exceeds expectations on job growth, coupled with subdued wage inflation, could be received positively. It would suggest the economy is achieving a smoother normalization—cooling sufficiently to alleviate inflation concerns without tipping into a downturn.

This "Goldilocks" scenario could provide broad-based support, potentially benefiting rate-sensitive growth stocks the most as it might temper fears of further Fed hawkishness.

However, a combination of strong headline job growth and robust wage increases would present a dilemma.

While indicative of economic strength, it would validate the Fed's cautious stance, likely pushing out expectations for rate cuts further and causing Treasury yields to rise. In this environment, cyclical and value-oriented sectors might find support, but technology and high-valuation growth stocks could face renewed selling pressure due to the higher discount rate applied to future earnings.

Conversely, a significantly weaker-than-expected report, especially if accompanied by a rise in the unemployment rate, would swiftly shift the narrative towards concerns about an economic slowdown. This could trigger immediate risk-off sentiment, negatively impacting consumer discretionary and industrial stocks. However, it might also spark a rally in bonds and reignite a bid for long-duration growth equities on anticipations of a more dovish Fed pivot.

The market is navigating a "low-hire, low-fire" environment that feels stable in aggregate but masks underlying churn and anxiety.