Event Reminder | Get Ready for 3:30 PM Today (Thursday, July 2nd)

S&P 500 index SPX | 0.00 | |

NASDAQ IXIC | 0.00 | |

Dow Jones Industrial Average DJI | 0.00 | |

NASDAQ-100 NDX | 0.00 | |

S&P 500 index GSPC | 0.00 |

01

Event and Background

The US Bureau of Labor Statistics will release the June Employment Situation report tonight at 03:30 Riyadh time, moved to Thursday from the usual Friday due to the July 4 Independence Day holiday.

| Time (Riyadh) | Indicator | Previous | Consensus | Forecast |

|---|---|---|---|---|

| 03:30 PM | Non-Farm Payrolls JUN | 172K | 110K | 110.0K |

| 03:30 PM | Unemployment Rate JUN | 4.3% | 4.3% | 4.3% |

| 03:30 PM | Average Hourly Earnings MoM JUN | 0.3% | 0.3% | 0.2% |

| 03:30 PM | Average Hourly Earnings YoY JUN | 3.4% | 3.5% | 3.4% |

| 03:30 PM | Initial Jobless Claims JUN/27 | 215K | 220K | 210.0K |

| 03:30 PM | Continuing Jobless Claims JUN/20 | 1821K | 1810K | 1825.0K |

| 03:30 PM | Jobless Claims 4-week Average JUN/27 | 224.25K | 220.5K |

This is the second nonfarm payrolls report under Fed Chair Kevin Warsh, and global markets are watching intently for signals on the future path of interest rates.

Over the past 18 months, the US labor market was largely stagnant. Nonfarm payrolls have beaten expectations for several consecutive months, averaging 188,000 new jobs per month since March—a sharp contrast to last year's average of under 10,000 per month.

This recovery, achieved amid Middle East turmoil and oil price shocks, makes tonight's data especially significant.

02

Expectations and How to Interpret

Market consensus expects June nonfarm payrolls to add approximately 111,000 to 115,000 jobs, down from May's 172,000, with the unemployment rate holding at 4.3% for a fourth straight month.

Forecasts vary widely:

- Bloomberg's survey ranges from a low of 25,000 to a high of 200,000.

- Goldman Sachs projects 140,000 jobs, citing a World Cup boost of roughly 40,000 hires concentrated in leisure and hospitality, professional and business services, and trade and transportation. The bank also notes a historical tendency for June's initial payroll print to be revised downward—11 of the past 13 years show that pattern, especially in state and local education. Strike resolutions should add about 4,000 jobs.

- RSM's Joe Brusuelas is even more bullish at 180,000, pointing to AI-driven construction, healthcare demand, and World Cup effects.

- Conversely, Barclays expects only 100,000.

- Citi's Veronica Clark projects as low as 25,000, citing weak ADP data, declining small business hiring plans, falling Indeed job postings, and rising initial jobless claims.

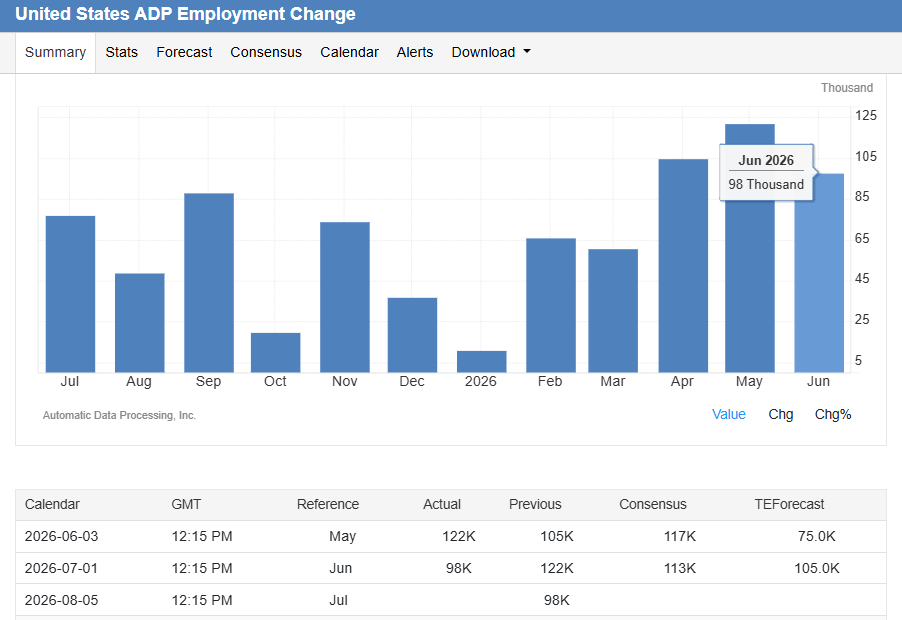

Wednesday's ADP report showed private payrolls slowing to 98,000 from 122,000, with healthcare again dominating—a concentration that, if repeated, could suggest the recent broadening is fragile.

Wage data also matters.

Average hourly earnings are expected to rise 0.3% month-on-month and 3.5% year-on-year, a slight acceleration from May's 3.4%. But with headline PCE inflation at 4.1%, wage growth still lags prices.

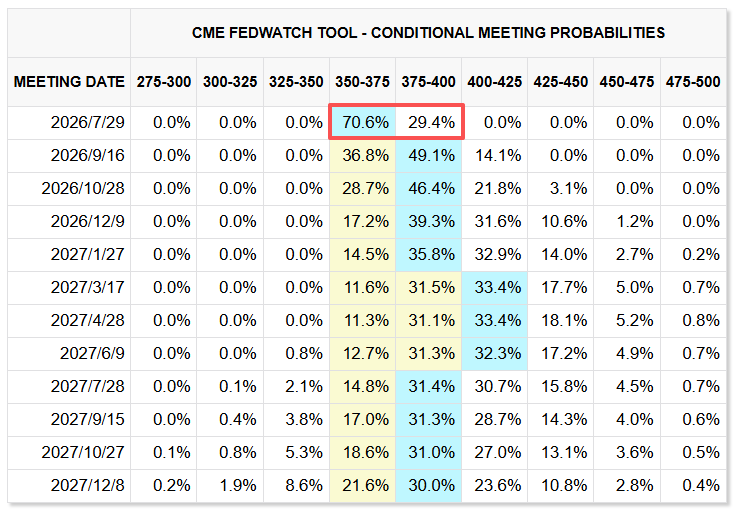

Fed Chair Warsh, speaking at the ECB forum gave no direct signal on the July meeting. The market currently prices a 70.6% chance of no change in July and a 29.4% chance of a 25-basis-point hike.

03

Impact on Equity Sentiment

JPMorgan provides a clear scenario framework.

- If payrolls exceed 160,000 (5% probability), the S&P 500 could fall 0.5% to rise 1.5%, reflecting rate-hike fears.

- Between 130,000 and 160,000 (25% probability), stocks gain 0.75% to 1.25%.

- The sweet spot is 100,000 to 130,000 (40% probability), where the S&P rises 0.5% to 1%—strong enough to confirm stabilization, not strong enough to trigger a hike.

- Below 100,000 (25% probability for 70,000–100,000, 5% for under 70,000), equities decline 0.5% to 2% as growth worries resurface.

Goldman's rates trader Brandon Brown notes that July hike pricing is currently around 8 basis points. A payrolls number above 100,000 combined with unemployment at or below 4.3% would push the odds of a July hike to 50-50, pending the mid-month CPI report.

Goldman's STIR trading desk adds that given Warsh's hawkish stance, the bar for a July hike is low—payrolls above 150,000 or unemployment rounding down to 4.2% could be enough. Short-end rates positioning is already heavily short, meaning a strong number could trigger a sharp repricing.