Event Reminder | Get Ready for 3:30 PM Today (Thursday, June 25th)

Micron Technology, Inc. MU | 0.00 | |

Dow Jones Industrial Average DJI | 0.00 | |

NASDAQ IXIC | 0.00 | |

S&P 500 index SPX | 0.00 | |

ETF-S&P 500 SPY | 0.00 |

Event Report and Background

At 8:30 a.m. ET on Thursday, June 25, the Bureau of Economic Analysis will release the May Personal Consumption Expenditures (PCE) price index—the Federal Reserve’s preferred inflation gauge and, arguably, the single most consequential data drop since Kevin Warsh took over as Fed chair earlier this month.

Also will released at the same time are the following gauges:

| Time (Riyadh) | Indicator | Previous | Consensus | Forecast |

|---|---|---|---|---|

| 03:30 PM | Core PCE Price Index MoM MAY | 0.2% | 0.3% | 0.2% |

| 03:30 PM | Durable Goods Orders MoM MAY | 7.9% | -4.5% | -4.0% |

| 03:30 PM | GDP Growth Rate QoQ Final Q1 | 0.5% | 1.6% | 1.6% |

| 03:30 PM | Personal Income MoM MAY | 0% | 0.4% | 0.3% |

| 03:30 PM | Personal Spending MoM MAY | 0.5% | 0.6% | 0.7% |

| 03:30 PM | Initial Jobless Claims JUN/20 | 226K | 225K | 225.0K |

| 03:30 PM | PCE Price Index MoM MAY | 0.4% | 0.5% | 0.4% |

| 03:30 PM | PCE Price Index YoY MAY | 3.8% | 4.1% | 4.0% |

| 03:30 PM | Continuing Jobless Claims JUN/13 | 1810K | 1800K | 1815.0K |

| 03:30 PM | Core PCE Price Index YoY MAY | 3.3% | 3.4% | 3.3% |

| 03:30 PM | Core PCE Prices QoQ Final Q1 | 2.7% | 4.4% | 4.4% |

| 03:30 PM | PCE Prices QoQ Final Q1 | 2.9% | 4.5% | 4.5% |

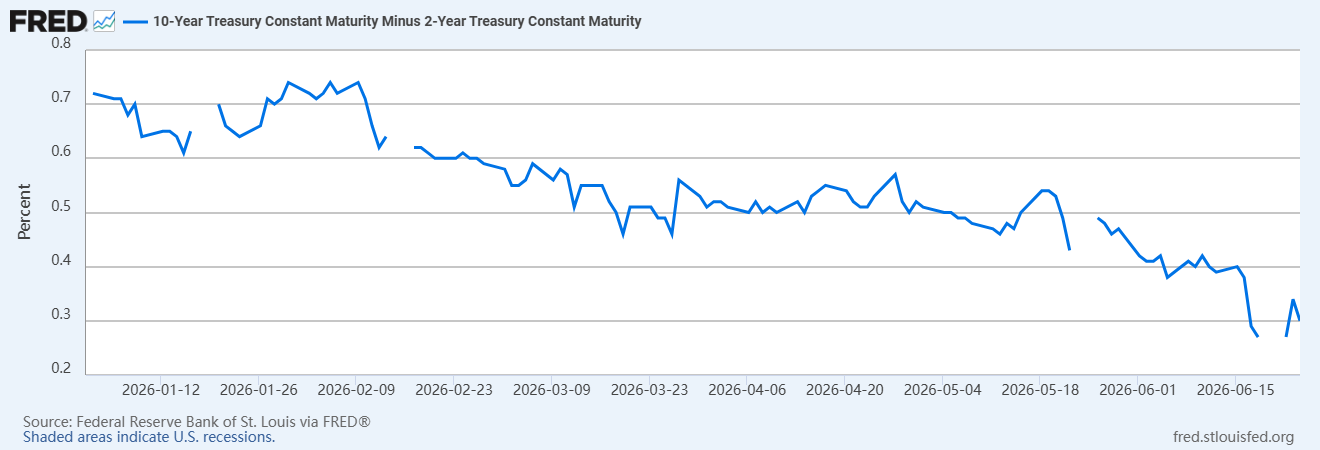

1) The timing could hardly be more charged.

Last week’s FOMC meeting, Warsh’s first in the chair, held rates at 3.50%–3.75%, and Warsh’s post-meeting tone was described by multiple desk strategists as unambiguously inflation-first.

Since then, the front end of the Treasury curve has repriced violently.

Into that fraught setup comes the May PCE, the first “clean” read on whether the Iran-war energy shock translated into broad-based price acceleration or stayed contained in the headline.

2) The macro crosscurrents are unusually messy.

On one hand, the US and Iran’s tentative peace framework and the reopening of the Strait of Hormuz have unwound the war premium.

On the other hand, May’s CPI already printed a three-year high of 4.2%, and producer prices remain hot on supply-chain pass-throughs from the war plus lingering tariff effects.

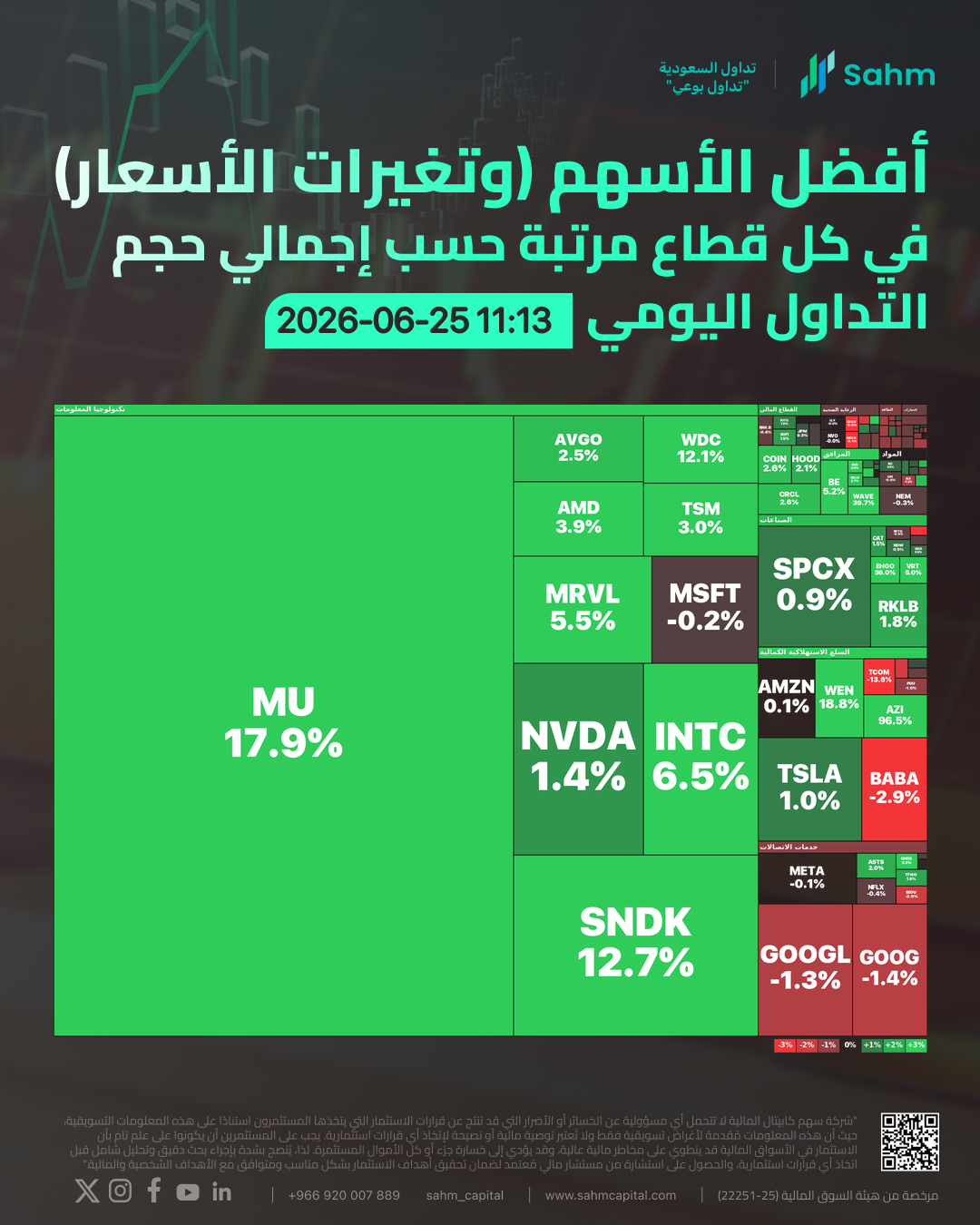

Meanwhile, Micron Technology, Inc.(MU.US)’s blowout fiscal Q3—revenue well ahead, Q4 guidance of roughly US$50 billion versus US$11.3 billion a year earlier, shares gainedpre-market—has handed tech a fragile sentiment lifeline.

Read more: Pre-Bell Movers | MU Picks up 17.9%; Here Are 20 Stocks Moving Premarket (Jun/25th)

But that lifeline only holds if PCE doesn’t force Warsh to accelerate the hawkish pivot.

Expectations and Interpretation

Consensus is firmly clustered:

FactSet and Dow Jones/WSJ surveys point to headline PCE +0.5% m/m, +4.1% y/y (up from 3.8% in April, the highest since April 2023), and core PCE +0.3–0.4% m/m, +3.3–3.4% y/y (up from 3.3% in April, also a multi-year high).

Bank of America, Goldman Sachs, and UBS all expect the print to mirror what CPI and PPI already telegraphed—energy the dominant driver of the headline, but core creeping higher on durable goods and core-services-ex-housing, which Morningstar’s Preston Caldwell notes has accelerated from 3.3% y/y in Q4 2025 to 3.7% now.

The interpretation framework splits along two axes.

First, headline vs. core.

A 4.1% headline is largely a “known known”—it bakes in May’s war-period gasoline spike, which has already reversed in June (AAA regular-grade gasoline is down about US$0.56/gallon since May 20, per UBS).

If core prints 3.4% or higher, that is the real problem: it tells Warsh and the committee that the inflation pulse is not just energy-one-off but also durable-goods renormalization—BofA’s Aditya Bhave and Mott Capital’s Michael Kramer both flag that durable goods prices were +3.3% y/y in April, a stark reversal from the pre-pandemic norm where they fell annually and acted as a structural deflation anchor. If that stickiness holds, the Fed’s current 3.50%–3.75% stance may genuinely not be restrictive enough.

Second, the peak narrative.

UBS, BofA, and Caldwell all argue May is likely the y/y peak for headline, with June–July deceleration as oil fades and tariff effects roll off. Core, though, may stay flat in June before slowing in July.

That distinction matters for Warsh: a hot print with a clear energy-driver excuse lets him stay data-dependent without pre-committing to July; a hot print withoutthat excuse (i.e., core overshoot + durable-goods persistence) forces his hand.

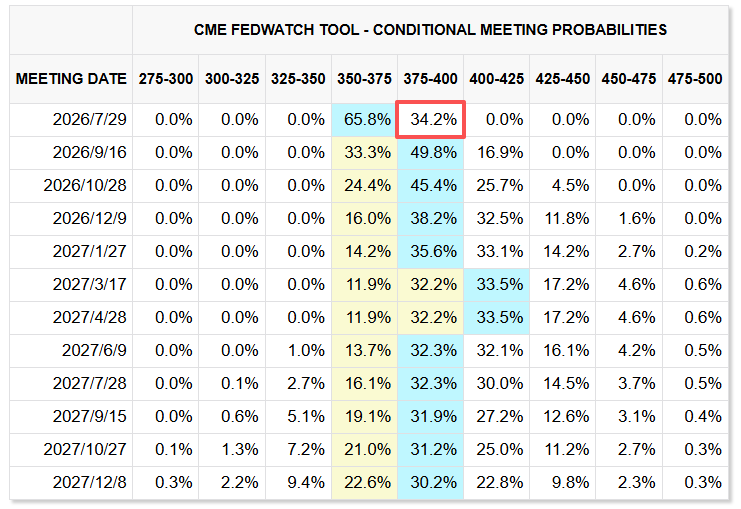

CME’s FedWatch shows only ~34% odds of a July hike as of Wednesday, but August futures flow suggests the street is leaning closer.

If PCE comes in +0.5% headline / +0.4% core or hotter, those odds reprice above 50% fast.

Impact on Market Sentiment

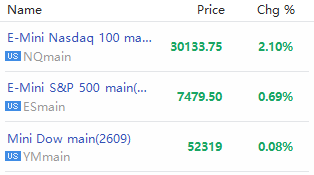

Equities walk into Thursday’s release on a split screen.

The Dow Jones Industrial Average(DJI.US) closed up 0.35% Wednesday on the oil-drop/rate-patience mix, while the NASDAQ(IXIC.US) slipped 0.43% and the S&P 500 index(SPX.US) was essentially flat—tech still bleeding under the weight of higher discount-rate pricing.

Futures Thursday morning showed Nasdaq 100 and S&P 500 gain, buoyed by the Micron print, but that bid is fragile.

If PCE confirms the hawkish base case, the discount-rate math hits exactly the cohort Micron is supposed to drag higher: long-duration, rate-sensitive growth and semis. Material one cautions explicitly that even a Micron EPS beat isn’t a clean buy signal—what matters is whether management confirms the AI-memory supply–demand tightness extends into 2026; a weak guide + hot PCE is a classic “sell the news” setup for semis.

Beyond tech, the rotation logic is straightforward.

Hotter PCE = push-out of cuts, maybe a hike = money flows toward high-rate-tolerant quality

(financials, selectors like the Dow’s composition) and away from duration-heavy growth.

For now, the path of least resistance:

PCE prints ~4.1%/3.4%, Warsh stays coy but hawkish-leaning into July, front-end rates grind higher, tech stays heavy, semis bifurcate on guides, and the Iran truce keeps a floor under risk as long as the strait stays open.

The real volatility kicker is if core surprises north of 3.5%—then the “Warsh hike” trade goes from whisper to consensus, and everything long duration reprices again.