Event Reminder | Get Ready for 9:00 PM Tonight (Wednesday, July 8th)

S&P 500 index SPX | 0.00 | |

NASDAQ IXIC | 0.00 | |

Dow Jones Industrial Average DJI | 0.00 | |

NASDAQ-100 NDX | 0.00 | |

S&P 500 index GSPC | 0.00 |

01

Event Preview

The Federal Reserve will release the minutes of its June FOMC meeting at 09:00 PM Riyadh time on Wednesday, marking the first set of official deliberation records under new Chair Kevin Warsh.

| Time (Riyadh) | Indicator | Previous | Consensus | Forecast |

|---|---|---|---|---|

| 08:00 PM | 10-Year Note Auction | 4.538% | ||

| 09:00 PM | FOMC Minutes |

The release carries unusual weight: in the post-meeting statement from June 17, Warsh has said he welcomes open debate among officials, framing it as “family disagreements” kept behind closed doors — which only raises the stakes for whether the minutes reveal any of that internal split.

For a Fed that has cut public communication sharply, with officials delivering only 18 speeches since the June meeting, down from 49 a year earlier and 55 two years prior, the minutes are the only meaningful window to fill the information void left by Warsh’s deliberate silence. The June meeting itself held the fed funds target at 3.5%–3.75%.

02

What to Expect

The broader macro backdrop frames how the minutes will land.

Markets currently price ~32 basis points of Fed hikes by year-end via SOFR swaps, implying one to two 25bp increases across the remaining four meetings.

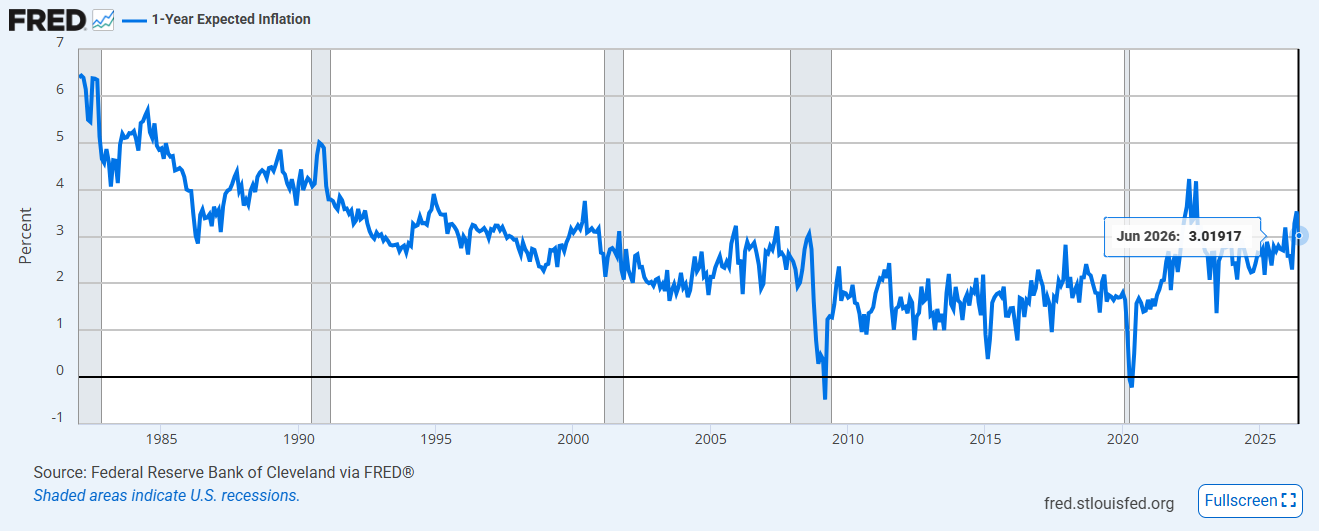

But Deutsche Bank warns of a stark cross-asset disconnect: one-year US inflation swaps have fallen to 2.1%, their lowest since 2024, on crude’s retreat, yet hike pricing remains elevated.

Morgan Stanley adds that even after last week’s softening on the back of a weaker June ADP and nonfarm print, embedded tightening expectations are still too high.

Four key angles will drive interpretation.

- First, inflation wording: markets will scan for references to “persistent” or “sticky” non-energy inflation, and check whether previous forward-guidance phrasing such as “some further tightening may be appropriate” is retained or dropped.

- Second, AI and productivity: Warsh mentioned monitoring AI’s supply-side effects at the ECB Sintra forum; any sign the full committee discussed the AI capex boom’s long-term productivity boost would signal the Fed sees room to stay patient on hikes.

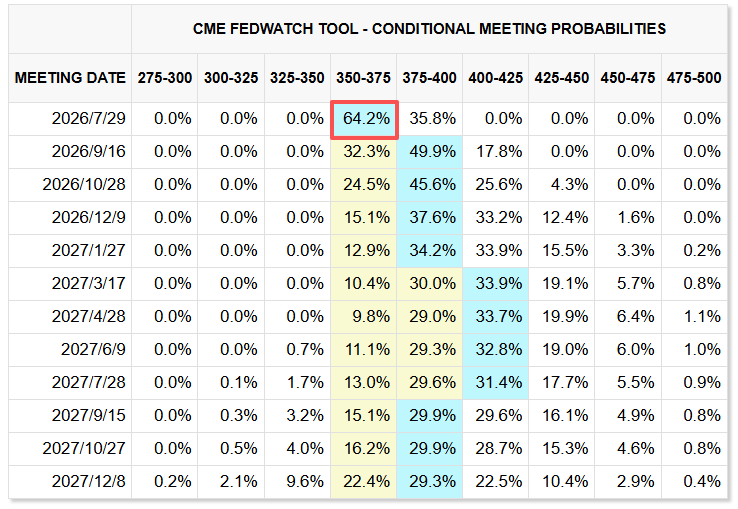

- Third, voting concentration: the minutes’ distinction between “some participants” (usually non-voters), “most participants” and “the Committee” will reveal whether hawkish voices pushing for September hikes hold voting power — the June dot plot showed 9 of 18 officials expected at least one 2026 hike, though Warsh himself did not submit a projection.

- Fourth, early signs of dissent: the April minutes noted three officials wanted stronger hike language in the statement; any increase in that count, or sharper opposition, would raise the stakes for the September meeting.

Impact to Sentiment

Equity markets are poorly positioned for a re-acceleration of hike pricing, per Deutsche Bank: the S&P 500 index(SPX.US) remains near record highs, credit spreads are tight, and financial conditions are among the loosest in a decade, even as futures embed further tightening. That mismatch means the minutes’ tone will drive outsized moves.

If the minutes lean hawkish — more dissent for tighter language, no meaningful discussion of AI patience, retention of sticky inflation wording — hike pricing will climb, pressuring rate-sensitive growth names and widening the cross-asset gap, with volatility likely to pick up if the minutes are overly sparse.

Wrightson ICAP’s Lou Crandall has warned vaguer Fed communication tends to raise asset price swings, and Englander notes a total lack of hike discussion alongside data that supports tightening could dent Warsh’s credibility, adding another layer of risk.

If the minutes instead confirm the Fed sees room to wait — AI debate is substantive, inflation language softens, dissent does not widen — it would validate Morgan Stanley’s view that current tightening pricing is excessive, likely triggering a relief rally across equities, particularly tech-heavy indices that had priced in steeper hawkish repricing earlier this month.

Traders have already started hedging: SOFR call options betting on a pivot to cuts by year-end have seen heavy uptake since Warsh’s slightly softer comments at Sintra, reversing earlier positions betting on a July hike.