Event Reminder | Get Ready for 9:00 PM Tonight (Wednesday, June 17th)

S&P 500 index SPX | 0.00 | |

NASDAQ IXIC | 0.00 | |

Dow Jones Industrial Average DJI | 0.00 | |

NASDAQ-100 NDX | 0.00 | |

S&P 500 index GSPC | 0.00 |

Event Report and Background

The Federal Open Market Committee will announce its rate decision at 2:00 p.m. ET on Wednesday, June 17, followed by Kevin Warsh’s first solo press conference at 2:30 p.m.

| Time (Riyadh) | Indicator | Previous | Consensus | Forecast |

|---|---|---|---|---|

| 09:00 PM | Fed Interest Rate Decision | 3.75% | 3.75% | 3.75% |

| 09:00 PM | FOMC Economic Projections | |||

| 09:00 PM | Interest Rate Projection - 1st Yr | 3.1% | ||

| 09:00 PM | Interest Rate Projection - 2nd Yr | 3.1% | ||

| 09:00 PM | Interest Rate Projection - Current | 3.4% | ||

| 09:00 PM | Interest Rate Projection - Longer | 3.1% | ||

| 09:30 PM | Fed Press Conference |

This is not a normal policy meeting—it is the formal opening act of the post-Powell, Warsh-led Fed, landing in the middle of the most violent macro whipsaw of the 2026 cycle.

Just weeks ago, markets were still debating whether Warsh might eventually deliver the rate cuts Donald Trump appointed him to deliver. Then May’s data destroyed that illusion: payrolls printed +172,000, nearly double consensus, with the unemployment rate glued at 4.3%, while the Iran war energy shock pushed May CPI to a three-year high of 4.2%.

The bond market repriced violently, with the 10-year yield spiking toward 4.55% and tech taking a historic single-day beating.

Expectations and Interpretation

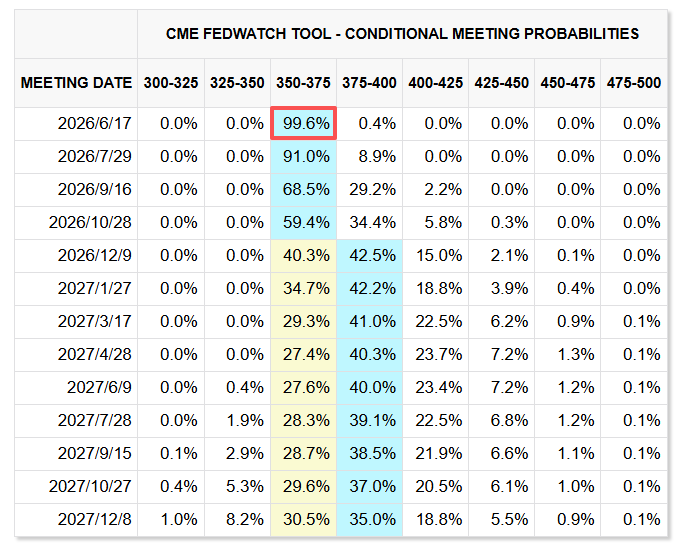

There is a 0% surprise factor on the rate decision itself.

Every desk on the Street expects the FOMC to hold the fed funds range at 3.50%–3.75%, and no one anticipates a cut or hike at this meeting. The entire focus is on communication: how Warsh frames the committee’s bias, how he handles the “dot plot” tradition he has spent years attacking, and what the updated economic projections imply about the path forward.

First, watch the policy statement’s wording on bias.

For months, hawkish FOMC voters have resisted the implicit “loose tilt” baked into the word additionalin the clause describing future adjustments. Stripping that word—making a hike and a cut equally on the table—is now treated as a fait accompli; one CNBC survey showed 88% of respondents expect the “easing bias” phrasing to be removed Wednesday.

Because Trump’s vocal ally Governor Milan has resigned to free the board seat for Warsh’s allies, the reliable dovish dissent that plagued recent meetings disappears, making a clean, possibly even unanimous vote far more likely if the statement is hardened.

Second, the “dot plot” and SEP drama.

Warsh has been explicit: he views over-engineered forward guidance and the dot chart as a constraint that trapped the Fed into bad 2021–2022 calls. Multiple Fed watchers—Bank of America, Goldman, Yale’s Bill English—expect Warsh to withhold his own dot this cycle, which would break a 14-year SEP convention.

The risk is optical: if the chair downweights the dots without offering a clear, credible substitute communication framework, markets may interpret it as “hiding” an even more hawkish internal consensus, which could unanchor short-term rate expectations. The safer interpretation is that Warsh is signaling a return to genuine, meeting-by-meeting discretion rather than path dependency.

Third, the economic projections themselves.

Even if the SEP is retained, the median path will formalize what trading desks already price: no 2026 cuts, with some officials now penciling in hikes. Citadel Securities argues the data already supports a 75bp optimal hiking path via the Taylor rule, with September as the most plausible first window; UBS went further and pushed the first cutall the way to 2027.

The Iran peace deal makes the immediate inflation threat messier rather than simpler: Warsh will acknowledge the oil drop as a tailwind, but he will also emphasize that lagged cost-push effects mean the committee cannot presume inflation is returning to 2% on autopilot. Expect the inflation upgrade and unemployment downgrade to do the heavy lifting in signaling that “higher for longer” is now the base case, not a threat.

Impact on Market Sentiment

For equities, the key realization is that the hold itself is already fully priced; what moves stocks is whether Warsh confirms a hostile, hike-prone regime or preserves a data-dependent off-ramp.

If Wednesday’s package is “hawkish on wording, cautious on guidance”—meaning the loose bias is gone, dots skew tighter, but Warsh repeatedly credits the oil drop and refuses to pre-commit to a hike—markets will treat it as a manageable continuation of the current regime. The recent oil crash already rebuilt a floor under risk assets; in that scenario, defensives, energy, and quality cyclicals outperform, while long-duration tech and low-quality small-caps stay heavy under the weight of 4%+ CPI and a 3.75% terminal ceiling.

The bigger danger for sentiment is a communication misstep: if Warsh leans too hard into hike odds, validates the 75bp Street-whisper path, or creates an information vacuum by gutting forward guidance without anchoring expectations elsewhere, the multiple compression that hit tech after the May jobs print could easily widen. The Nasdaq’s recent bounce is thin; without a clear “not hiking unless data forces it” signal, volatility will bleed back into risk assets fast.

Ultimately, Warsh’s first meeting is less about what the Fed does to rates today and more about whether he can project a Fed that is tough on inflation without looking like it is flying blind.

If he threads that needle, the post-peace-rally holds; if he doesn’t, the market will reprice the “Warsh premium” the hard way.