Fastenal (FAST) Stock Looks Fairly Priced After 12% Q1 Sales Growth

Fastenal Company FAST | 0.00 |

Fastenal (FAST) is back in focus after reporting a 12% rise in first quarter 2026 net sales, tied to share gains, broad-based demand, and ongoing efforts in digital tools and cost control.

Fastenal's recent 12% net sales growth and new board appointment of digital executive Vishal Talwar come against a backdrop of a 14.0% year to date share price return and a 5 year total shareholder return of 102.03%, suggesting momentum has been building over longer horizons even as the 1 day share price slipped 1.01%.

If Fastenal's mix of industrial demand and digital execution has your attention, this could be a good moment to broaden your lens and look at 35 power grid technology and infrastructure stocks

With Fastenal stock sitting close to analyst price targets and recent gains already reflected in multi year returns, the key question now is simple: is there still value on the table, or is future growth already baked into the price?

Most Popular Narrative: 0.8% Undervalued

Fastenal's most followed narrative pegs fair value at $46.49, almost exactly in line with the last close of $46.10. This puts the focus firmly on execution rather than a large valuation gap.

The company is expanding its Fastenal Managed Inventory (FMI) technology which currently represents over 43% of revenue, aiming to enhance revenue growth by increasing efficiency in customer supply chains.

Fastenal aims to increase its digital footprint to represent 66-68% of sales, up from 61%, potentially boosting revenue by optimizing purchasing and operational efficiency.

Want to understand why this fair value sits so close to the current Fastenal share price? The narrative leans on steady top line growth, slightly improving margins, and a future earnings multiple that assumes investors continue to pay a premium for this model. The exact growth pacing, margin lift, and valuation bridge are where the real story sits.

Result: Fair Value of $46.49 (ABOUT RIGHT)

However, there are still clear risks to the Fastenal narrative, including higher tariff costs on China sourced products and ongoing pressure on operating margins from elevated SG&A and freight expenses.

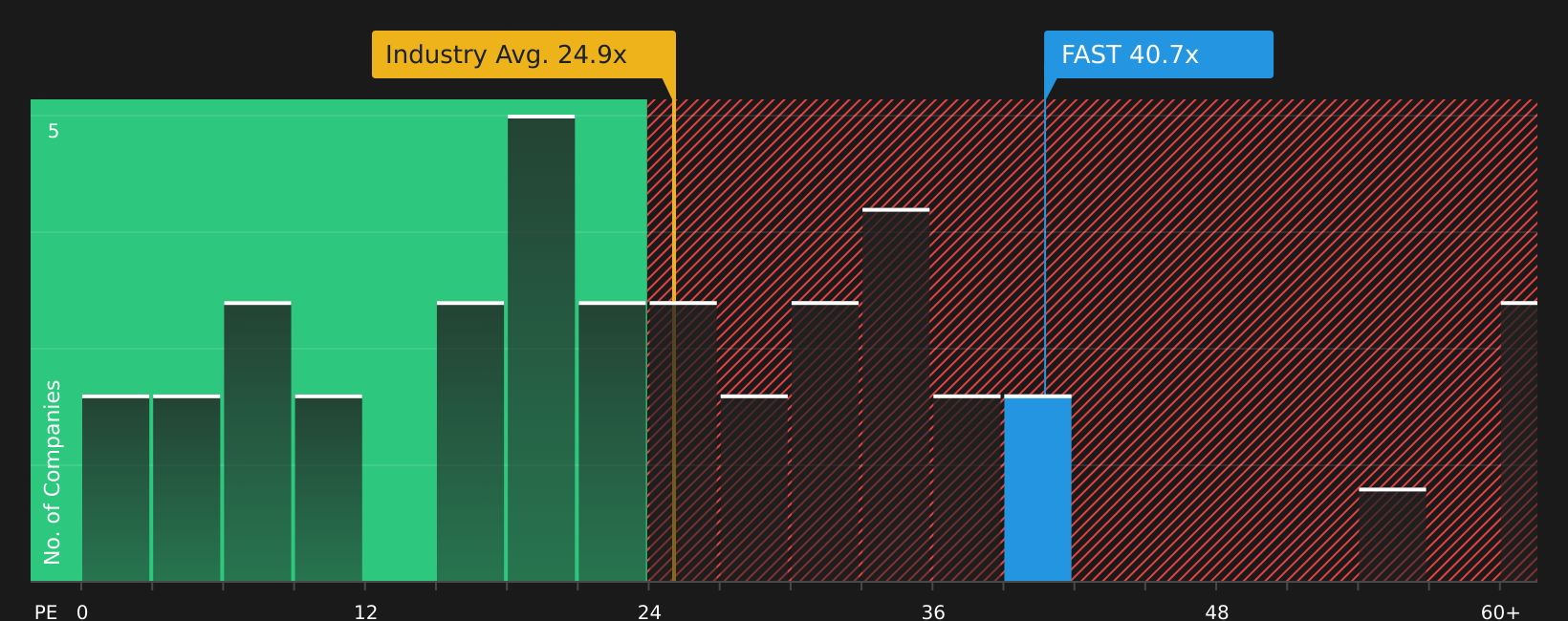

Another View: Fastenal Stock Through a P/E Lens

While the Fastenal fair value narrative points to a price around $46.49, the current P/E of 40.7x tells a tougher story. That multiple sits well above the US Trade Distributors industry at 24.4x, the peer average at 25.9x, and the fair ratio of 28.5x. This spread suggests the market could move toward a lower valuation multiple over time. For investors, that gap raises a practical question: is this quality profile worth paying such a premium for today, or does it add valuation risk if expectations cool?

To see how this premium stacks up against the underlying numbers, and where the fair ratio sits in more detail, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and concern around Fastenal leaves you undecided, take a closer look at the underlying data now and weigh both sides of the story with the 2 key rewards and 1 important warning sign

Looking for more investment ideas beyond Fastenal?

Fastenal may be front of mind today, but the next opportunity could be elsewhere, and you do not want to spot it after the market has already moved.

- Target future income by reviewing companies with resilient payouts and yields in the 9 dividend fortresses

- Hunt for quality at a sensible price using the 47 high quality undervalued stocks to see which stocks currently combine strong fundamentals with appealing valuations.

- Protect your capital first by scanning companies that score well on stability through the 68 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.