From TACO To NACHO: Why Wall Street Is Suddenly Pricing A Long Oil Shock — And What Could Break The AI Bull Run

PHLX Semiconductor SOX | 0.00 | |

Exxon Mobil Corporation XOM | 0.00 | |

Chevron Corporation CVX | 0.00 | |

Shell Plc Sponsored ADR SHEL | 0.00 | |

BP PLC Sponsored ADR BP | 0.00 |

- Why hasn’t oil fully surged yet?

Because U.S. export growth and China’s reduced imports temporarily absorbed the global supply shock. - Why is June critical for markets?

Current buffers may run out by summer, forcing oil prices to reprice sharply higher. - Why does NACHO matter more than past geopolitical scares?

Markets are shifting from betting on quick de-escalation to pricing a long-term energy shock. - Who wins and loses under NACHO?

Energy and shipping sectors benefit, while AI momentum trades and rate-sensitive growth stocks face pressure.

For most of 2025, global markets lived by one acronym: TACO — Trump Always Chickens Out. Every tariff escalation, military threat, or geopolitical flare-up was treated as temporary noise. Traders bought every dip, expecting eventual de-escalation.

Now, Wall Street is rotating into a far more dangerous framework: NACHO — Not A Chance Hormuz Opens.

And unlike TACO, this trade is not about political theater. It is about a structural supply shock colliding with one of the most crowded AI-driven momentum rallies in market history.

Brent crude climbing back above $105 may only be the beginning.

The Market Is Finally Realizing This Is Not A “Temporary Spike”

The biggest shift in recent weeks is psychological.

For months, markets repeatedly priced in imminent peace headlines between the U.S. and Iran. Every rumor of negotiations triggered sharp oil selloffs. Yet the Strait of Hormuz — the artery responsible for roughly 20%-30% of global oil and LNG flows — has remained effectively under dual military control since late February.

Now the market is beginning to accept a harder truth:

Even if the Strait reopens tomorrow, the global energy system cannot simply restart overnight.

That realization is at the heart of the emerging NACHO trade.

According to recent reports from both Morgan Stanley and Citigroup, the world has so far avoided a full-scale oil shock only because two temporary buffers absorbed the disruption:

- The U.S. dramatically increased crude exports.

- China sharply reduced imports and relied on inventory drawdowns.

Together, those adjustments masked what Morgan Stanley estimates was effectively a supply gap of roughly 9 million barrels per day.

But those buffers are not infinite.

That is why June is increasingly viewed by energy desks as a potential “judgment month.”

If the Hormuz disruption extends deeper into summer:

- U.S. export flexibility could tighten,

- China may need to resume imports,

- global inventories could fall dangerously low,

- and crude prices may need to rise sharply to ration demand.

Morgan Stanley’s bullish scenario now sees Brent potentially surging toward $130-$150 if the blockade persists into late summer. Citi continues to maintain a near-term $120 upside scenario.

That changes everything for equities, rates, inflation, and sector leadership.

Why This Matters Beyond Oil

The key mistake many investors still make is treating the Hormuz crisis as an isolated commodity event.

It is becoming something much bigger:

- a global inflation shock,

- a supply-chain repricing event,

- and potentially a regime shift away from pure AI momentum trading.

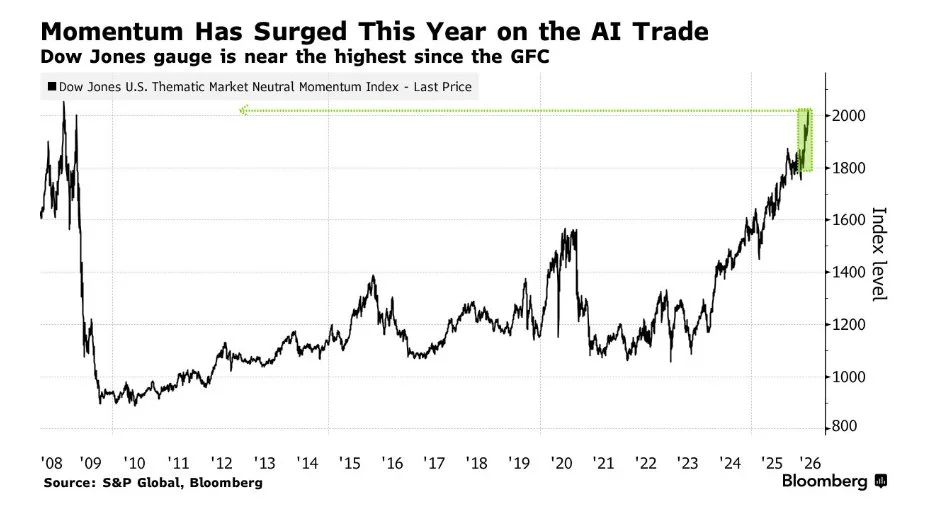

This is especially important because the current equity rally already looks extremely crowded.

The PHLX Semiconductor(SOX.US) has surged over 66% from its March lows, while AI-linked megacaps continue to dominate global equity inflows. Momentum positioning, according to several Wall Street prime brokerage desks, is now near historical extremes.

Historically, that combination becomes fragile when:

- inflation expectations rise,

- bond yields stay elevated,

- and energy prices accelerate simultaneously.

That is exactly what NACHO threatens to create.

Higher oil prices do not just hurt consumers. They also:

- reduce the probability of Fed rate cuts,

- pressure long-duration growth valuations,

- raise freight and logistics costs,

- and compress margins across airlines, chemicals, manufacturing, and consumer sectors.

In other words, the AI bull market may remain intact structurally — but the macro backdrop supporting hyper-aggressive momentum chasing is deteriorating rapidly.

The Bond Market Is Already Flashing Warnings

One of the clearest signals is no longer coming from oil itself, but from rates markets.

Investors are increasingly repricing the possibility that central banks stay restrictive for longer because of persistent energy inflation.

That matters enormously because the 2025 AI rally has depended heavily on:

- falling inflation expectations,

- stable long-end Treasury yields,

- and assumptions that global liquidity conditions would improve.

A sustained oil shock threatens all three.

If Brent stabilizes above $110-$120:

- headline CPI could reaccelerate globally,

- real yields may rise,

- and the “multiple expansion” driving many AI stocks could begin reversing.

That does not necessarily mean a bear market.

But it does raise the odds of:

- violent sector rotation,

- sharp momentum unwinds,

- and a transition from speculative AI chasing toward hard-asset and cash-flow-oriented trades.

The NACHO Related Assets to Watch

The market is increasingly separating into two camps:

- sectors hurt by structurally higher energy costs,

- and sectors that directly benefit from prolonged supply disruption.

Integrated Oil Majors

- Exxon Mobil Corporation(XOM.US)

- Chevron Corporation(CVX.US)

- Shell Plc Sponsored ADR(SHEL.US)

- BP PLC Sponsored ADR(BP.US)

These firms benefit from higher upstream margins and stronger free cash flow.

U.S. Shale & Exploration

If Middle East supply remains constrained, U.S. shale becomes strategically more valuable.

Oilfield Services

Longer-term supply shortages typically trigger higher global drilling and infrastructure spending.

Tankers & Shipping

War-risk insurance premiums and rerouted shipping lanes significantly raise tanker rates.

Energy ETFs

- Spdr Select Fund-Energy Select Sector(XLE.US)

- VanEck Vectors Oil Services ETF(OIH.US)

- United States Oil Fund Lp Units(USO.US)

These provide broader exposure to the NACHO theme without single-stock concentration risk.

The Market’s Biggest Question: Is This A Shock — Or A New Regime?

The core debate now is no longer whether oil can spike temporarily.

It is whether the world is entering a prolonged period where:

- energy supply remains structurally fragile,

- shipping routes stay militarized,

- inventories remain tight,

- and inflation becomes harder to suppress.

That is why NACHO matters.

The trade is not really about whether Hormuz physically reopens tomorrow morning.

It is about whether global markets are finally transitioning from:

- pricing short-term geopolitical headlines,

to

- pricing a persistent energy-risk regime.

If that transition continues, the second half of 2026 may look very different from the AI-driven melt-up that dominated the first half of the year.