Hecla Mining (HL) Valuation Rechecked After Strong Metals Prices And Upgraded Production Outlook

Hecla Mining Company HL | 19.11 | -0.05% |

Hecla Mining (HL) is back in focus after higher gold and silver prices coincided with solid 2025 production figures and fresh 2026 guidance, which has reinforced interest in the miner’s earnings power and balance sheet strength.

That renewed focus comes after a sharp pullback in the short term, with a 1 day share price return of 7.79% and 7 day share price return of 19.04% at a last close of US$21.31. This comes even though the 90 day share price return is 53.53% and the 1 year total shareholder return is very large, helped by higher metal prices, solid 2025 production, new 2026 guidance and the planned sale of its Quebec assets.

If this move in precious metals is on your radar, it could be a good moment to size up other miners using our screen of 7 top silver producer stocks as potential ideas to research further.

After a very large 1 year total return and strong 2025 production, along with a price target of US$26.65 compared with a last close of US$21.31, investors may ask whether there is still a buying opportunity or if the market already reflects future growth in the current price.

Most Popular Narrative: 73.4% Undervalued

According to the most followed narrative for Hecla Mining, a fair value of $80 per share sits well above the last close of $21.31, which naturally raises questions about how such a gap is justified.

Hecla Mining: Stock Price Estimate at $100 Silver

Key Assumptions

1. 2025 Production:

Silver: 20M oz.

Gold: 175K oz.

2. Prices:

Silver: $100/oz.

Gold: $4,000/oz.

3. Free Cash Flow (FCF): ~$1.6B annually.

4. Shares Outstanding: ~400M.

This narrative, built by RockeTeller, is based on a high free cash flow run rate, rich precious metal pricing and a premium cash flow multiple to reach its fair value. It focuses on the production scale, margin assumptions and FCF multiple at the core of that $80 figure, and how they interact to support such a large gap to today’s price.

Result: Fair Value of $80 (UNDERVALUED)

However, this depends on very aggressive silver and gold price assumptions and a rich 20x FCF multiple, which could decline if metal markets or sentiment shift.

Another View: Rich Multiples Signal Caution

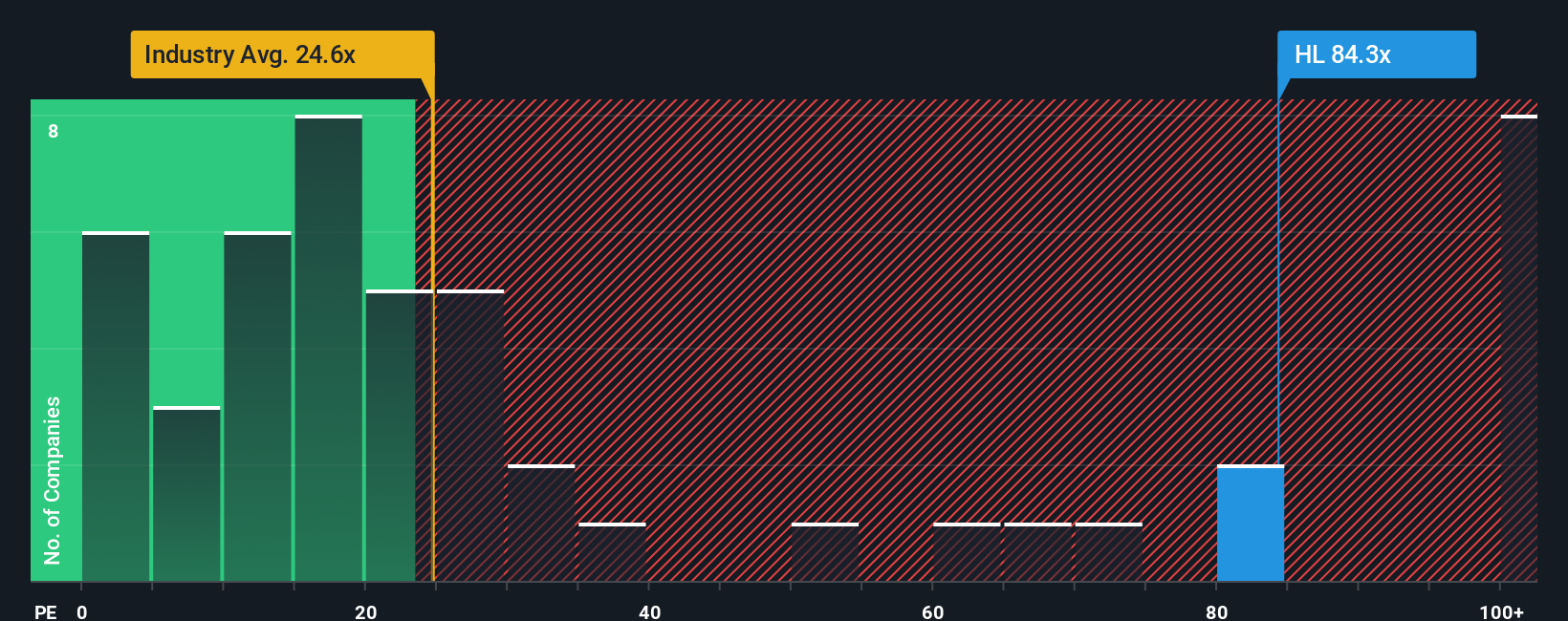

That $80 fair value hinges on very bullish metal prices and a premium cash flow multiple, but the current P/E of 71.9x tells a different story. It is well above the US Metals and Mining industry at 26.3x, peers at 28x, and even the fair ratio estimate of 31.6x.

In practical terms, you are paying a much higher price for each dollar of earnings than both peers and the level our fair ratio suggests the market could move toward. If sentiment cools or expectations reset, how much room is there for that gap to close without putting pressure on the share price?

Build Your Own Hecla Mining Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom Hecla view in just a few minutes: Do it your way.

A great starting point for your Hecla Mining research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Hecla has your attention, do not stop there. Cast a wider net across other opportunities that might suit your style and risk comfort.

- Target potential value opportunities early by scanning our list of screener containing 25 high quality undiscovered gems that the market may not be paying close attention to yet.

- Strengthen the quality of your watchlist by zeroing in on companies from the solid balance sheet and fundamentals stocks screener (46 results) that focus on financial resilience.

- Add more income focused ideas to your radar by reviewing the 15 dividend fortresses that might suit a returns plus income approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.