IBM (IBM) Stock After Mixed Returns And AI Cloud Growth Narrative

IBM Corp IBM | 0.00 |

Short-term traders and long-term holders alike may be asking the same question about International Business Machines right now: is the current share price giving you fair value for the risk you are taking?

Over the past week the stock gained 3.7%, and it is up 3.0% over the last month, even though the year to date return is down 11.4% and the 1 year return is down 9.3%, compared to a much stronger 112.2% return over 3 years and 123.9% over 5 years.

Recent headlines around International Business Machines have focused on its positioning in software and services, as investors reassess how legacy technology providers fit into portfolios. These stories set the backdrop for the mixed share price performance, with sentiment shifting between interest in its long-term role in enterprise technology and caution about nearer term returns.

On Simply Wall St's valuation checks, International Business Machines scores 3 out of 6 for value. The detailed breakdown is available on its valuation score. This sets up a closer look at different valuation approaches next and an even more comprehensive way to think about fair value at the end of this article.

Approach 1: International Business Machines Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what International Business Machines is worth today by projecting its future cash flows and discounting them back to a present value using a required rate of return.

International Business Machines currently generates trailing twelve month free cash flow of about $12.2b. The Simply Wall St model applies a 2 Stage Free Cash Flow to Equity approach, using analyst forecasts where available and then extrapolating further cash flows. For example, projected free cash flow for 2030 is $21.8b, with interim years such as 2026, 2027 and 2028 also forecast in the model, and longer term figures extrapolated beyond the analyst horizon.

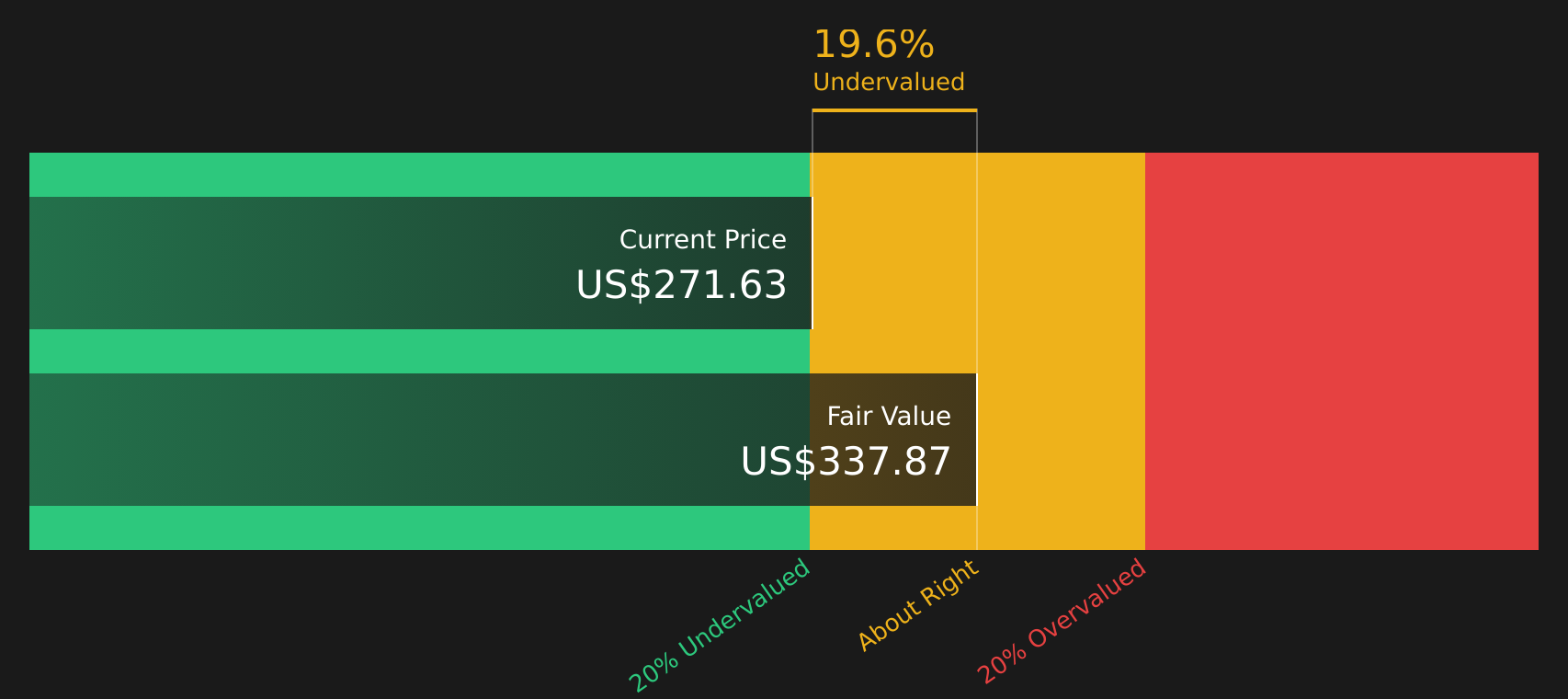

Bringing all of these projected cash flows back to today, the DCF model arrives at an estimated intrinsic value of $338.87 per share. Compared with the current share price, this implies the stock is 23.8% undervalued on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests International Business Machines is undervalued by 23.8%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Approach 2: International Business Machines Price vs Earnings

For profitable companies like International Business Machines, the P/E ratio is a useful way to relate what you pay for the stock to the earnings it currently generates. Investors typically accept a higher or lower P/E depending on what they expect for future earnings growth and how much risk they see in those earnings.

International Business Machines currently trades on a P/E of 22.6x. That compares with an IT industry average P/E of 16.1x and a peer group average of 9.8x, so the stock is priced at a higher earnings multiple than both its sector and peer benchmarks. Simply Wall St also calculates a proprietary Fair Ratio of 34.3x, which is the P/E level suggested by factors such as earnings growth characteristics, profit margins, industry, market capitalization and specific risk profile.

This Fair Ratio is more tailored than a simple comparison with peers or industry averages because it adjusts for company specific traits rather than assuming all stocks should trade on the same multiple. Comparing the current P/E of 22.6x with the Fair Ratio of 34.3x indicates that, on this framework, International Business Machines trades at a discount to the level implied by its characteristics.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your International Business Machines Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so here is Narratives, a simple tool on Simply Wall St’s Community page that lets you attach a clear story about International Business Machines to your numbers. It does this by linking your view on its future revenue, earnings, margins and fair value to the current share price, updating that view automatically when fresh news or earnings arrive, and allowing you to see how different investors can reach very different fair values. For example, one Narrative might anchor on a higher fair value around US$390 based on stronger AI, hybrid cloud and quantum adoption, while another anchors closer to US$195 with more caution about competition and margins. You can then compare where your own fair value sits versus the live market price and use that gap, alongside other research, to help frame your own decisions.

For International Business Machines, however, we will make it really easy for you with previews of two leading International Business Machines Narratives:

These summaries let you compare one view that leans into upside from quantum, software and margin expansion, with another that treats the recent news as attractive but potentially skewed in terms of risk and reward. Use them as starting points to test against your own expectations on growth, profitability and valuation.

Fair value: US$302.05 per share

Implied undervaluation versus the last close of US$258.27: about 14.5%

Assumed annual revenue growth: 5.18%

- Analysts frame International Business Machines around hybrid cloud, AI, mainframe refresh and acquisitions such as HashiCorp, with these elements expected to support revenue growth and margin expansion if execution aligns with forecasts.

- The narrative builds to a consensus price target of US$281.32, supported by forecasts for 2028 revenue of US$74.4b, earnings of US$10.5b and an assumed future P/E of 33.7x, discounted at 9.7%.

- Key risks focus on macro sensitivity in Consulting and Software, competition around Red Hat and virtualization, and currency volatility. These factors could all lead to outcomes that differ from the fair value estimate of about US$302.05 per share.

Fair value: US$256.08 per share

Implied overvaluation versus the last close of US$258.27: about 0.9%

Assumed annual revenue growth: 6.0%

- This narrative views International Business Machines as a large enterprise technology company with solid software, consulting and infrastructure franchises, but questions how much of the transformation toward hybrid cloud and AI is already reflected in the share price.

- It highlights strengths such as recurring software revenue, consulting relationships and mainframe replacement cycles, while also pointing to execution risk in AI, competition from hyperscalers and reliance on moderate growth to support current trading multiples.

- On these assumptions, a fair value of about US$256.08 per share is close to the recent market price and implies limited valuation buffer if growth, margins or capital allocation outcomes fall short of expectations.

If you want to go beyond the summaries and see how other investors are framing these bullish and bearish cases, as well as where they set their own fair values and risk flags, it is worth reviewing the full range of community views for International Business Machines through See what the community is saying about International Business Machines.

Do you think there's more to the story for International Business Machines? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.