IBM (IBM) Stock May Be 17% Below Fair Value After Chip Breakthrough

IBM Corp IBM | 0.00 |

International Business Machines stock has delivered a strong 175.0% return over the past five years, yet current valuation checks present a mixed picture, with the Discounted Cash Flow (DCF) intrinsic value estimate and earnings multiples both pointing to undervaluation while the broader score still signals caution.

- Over the last 5 years, International Business Machines has returned 175.0%, which puts more weight on whether today's price still offers a margin between market value and intrinsic value.

- Recent advances in areas such as sub 1 nanometer chip technology and quantum computing can support expectations for future cash flows, while a wide range of outcomes implied by options pricing highlights that uncertainty around those expectations is still high.

- International Business Machines screens as undervalued on both its Discounted Cash Flow (DCF) estimate and earnings multiples, but with only 2 of 6 valuation checks passing, the stock does not yet look like a straightforward bargain on the full set of metrics.

The issue now is whether International Business Machines' current share price around US$302.05 still leaves enough upside versus intrinsic value to compensate for that uncertainty.

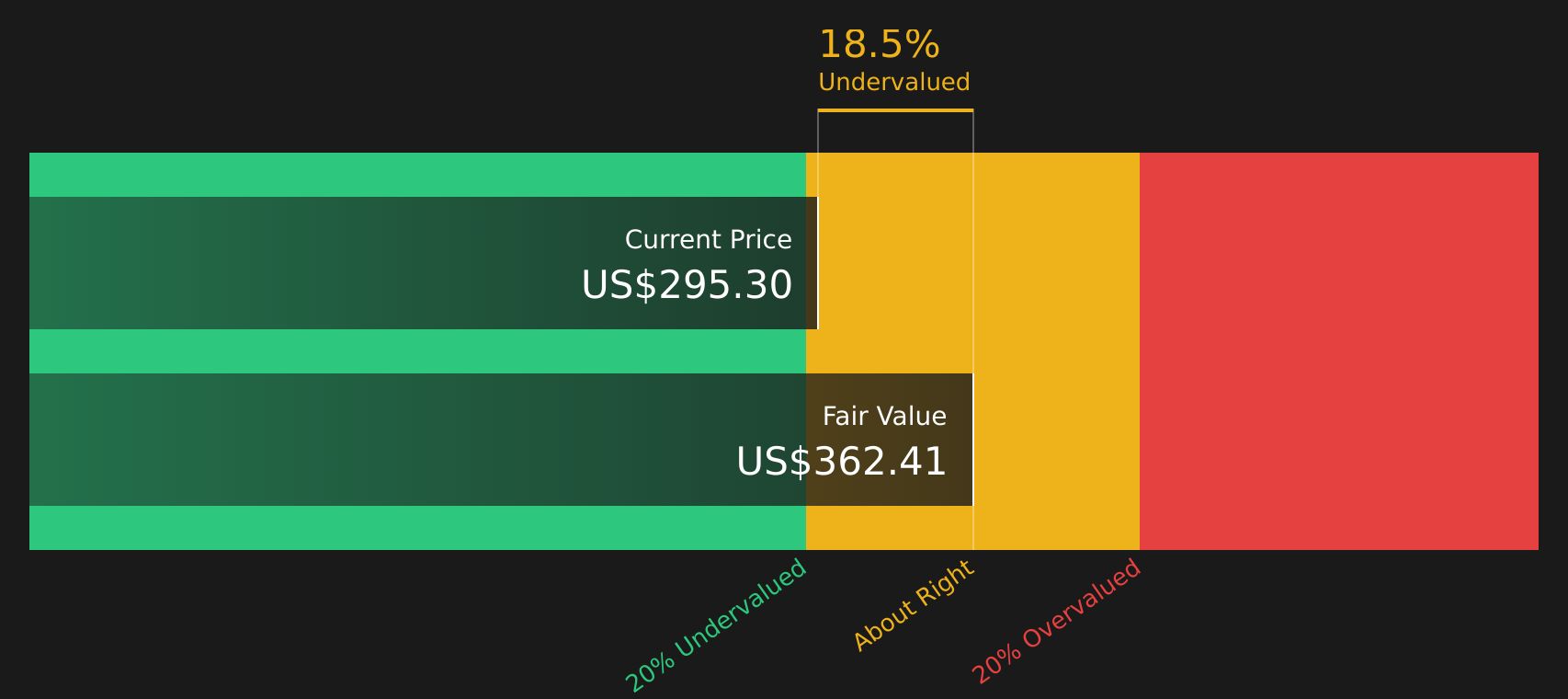

Is International Business Machines Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model values International Business Machines by projecting future cash that can be returned to shareholders and discounting it back to today. For IBM, the latest twelve month free cash flow sits at about $12.2b, and the model assumes that cash flows continue growing rather than contracting, using a two stage Free Cash Flow to Equity approach. On these inputs, the intrinsic value comes out at roughly $362 per share.

Against the current share price of about $302, the DCF implies International Business Machines trades at an intrinsic discount of roughly 16.7%, so the stock screens as undervalued on this cash flow view. The options market is currently pricing in a very wide one year range for IBM, with a potential $260 swing, which helps explain why the price has not fully closed that gap despite the cash flows supporting a higher value.

Overall, the Discounted Cash Flow (DCF) work suggests International Business Machines stock appears undervalued relative to the level of free cash it is expected to generate.

Our Discounted Cash Flow (DCF) analysis suggests International Business Machines is undervalued by 16.7%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is International Business Machines Still Cheap on Earnings?

The P/E multiple is a reasonable yardstick for International Business Machines, because earnings remain a key driver of how investors value this mature, cash‑generative tech company.

International Business Machines currently trades on a P/E of about 26.5x, compared with an IT industry average of roughly 18.0x and a peer average near 10.5x. On simple comparisons, that puts IBM at a premium to both its sector and many direct peers. However, the tailored fair P/E ratio for the stock is about 32.8x, reflecting the mix of IBM's earnings profile, market position in areas such as AI, quantum and mainframes, and its risk characteristics.

The gap between the current 26.5x and the fair 32.8x shows that, even after strong interest in International Business Machines and recent product announcements, the stock trades below the level implied by this earnings-based framework.

Overall, the P/E analysis indicates International Business Machines appears undervalued on earnings relative to the fair multiple implied by its fundamentals.

The International Business Machines Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the valuation work on International Business Machines leaves off by spelling out which future paths for growth, margins and earnings would make the stock worth materially more or less than today’s price, and they sit on Simply Wall St's Community page. Each one is framed as a thesis about International Business Machines' business that can be tracked over time, rather than a one off snapshot, so you can see how the reasoning holds up as new information arrives.

Community narratives on International Business Machines sit far apart, with one side seeing upside from AI and quantum and the other stressing execution and valuation risk.

Bull case: 23% undervalued

"IBM's early leadership and commercial progress in quantum computing and advanced automation, as well as sustained investment in mission-critical infrastructure (Power11, watsonx, agentic AI), position it not just as a catch-up play, but as an innovation front-runner..."

Bear case: roughly fairly valued

"Uncertain macroeconomic conditions and competitive pressures could affect Consulting and Software segments, with currency volatility posing further risks to revenue and growth..."

Do you think there's more to the story for International Business Machines? Head over to our Community to see what others are saying!

The Bottom Line

For International Business Machines, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiples point to the stock looking undervalued, yet the broader set of valuation checks remains weak. That mix suggests there may be a valuation gap, but not one that is clearly wide enough to ignore the risks already flagged by the options market and the debate around execution. The crux from here is whether IBM can convert its positions in areas such as AI, quantum and core infrastructure into durable cash flows that justify a higher multiple, rather than the current discount turning into a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.