IBM (IBM) Stock Stays Reasonable On Earnings While Cash Flow Looks Rich

IBM Corp IBM | 0.00 |

International Business Machines stock has dropped sharply in recent weeks, yet valuation checks suggest the current US$211.20 share price may sit below what its fundamentals imply, with both the intrinsic value estimate from a Discounted Cash Flow (DCF) approach and earnings multiples pointing in the same direction.

- Over 5 years, International Business Machines has returned about 90.3%, which puts the recent pullback in the context of a long, solid run for holders who stayed invested.

- On the upside, IBM's push into AI infrastructure, quantum computing and hybrid cloud can support expectations for future cash flows. On the downside, recent earnings disappointment and client budget shifts away from some software and mainframe spending highlight the risk that those cash flows materialize more slowly than hoped.

- The value checks are mixed rather than emphatic, with International Business Machines screening as undervalued on a Discounted Cash Flow (DCF) estimate and earnings multiples, but passing only 3 of 6 valuation tests overall.

The issue now is whether the recent sell off in International Business Machines has simply created a discount to intrinsic value, or is instead the market pricing in weaker cash flow and earnings power than the optimistic case assumes.

Is International Business Machines Still Cheap on Cash Flow?

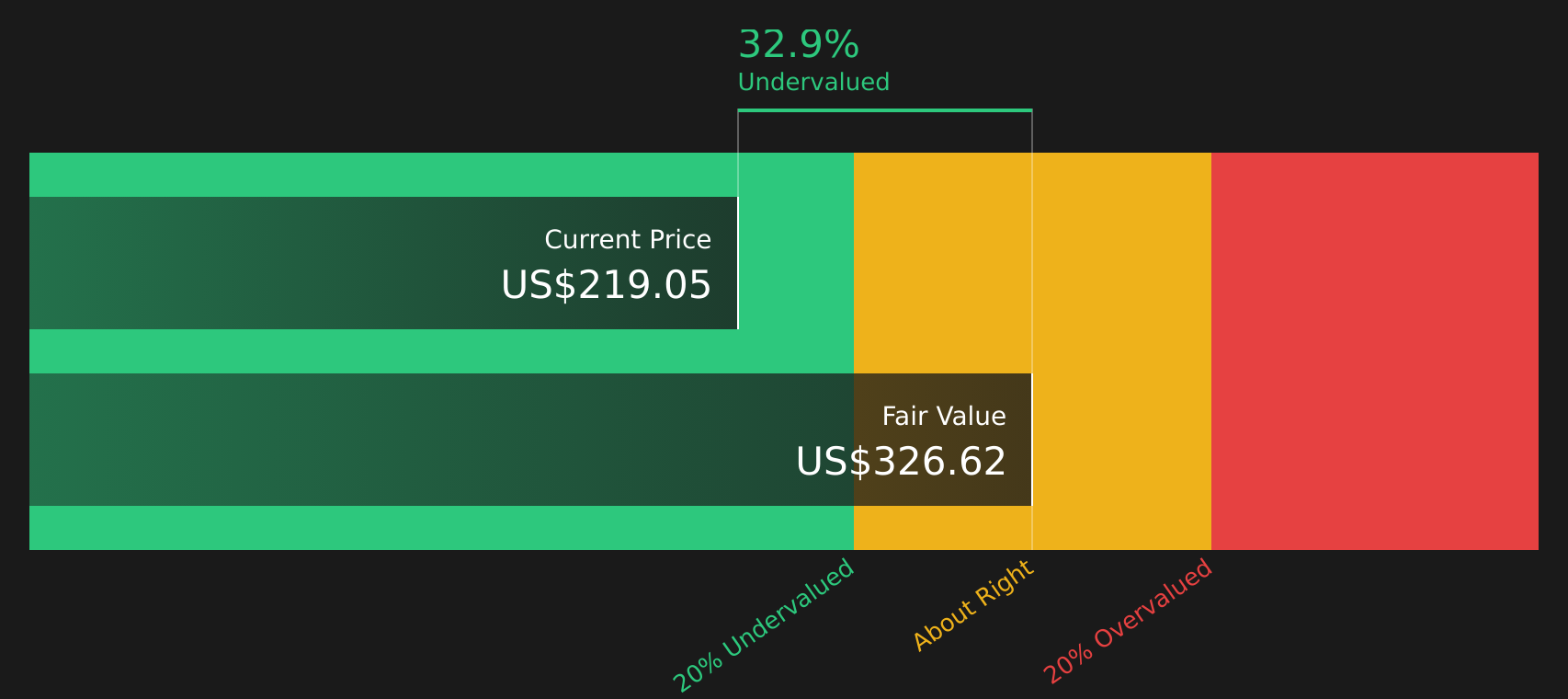

The Discounted Cash Flow (DCF) approach estimates what International Business Machines is worth based on the cash it can generate for shareholders. International Business Machines is modeled with a 2 stage Free Cash Flow to Equity framework, using latest twelve month free cash flow of about $12.2b and projecting growing cash flows over time. On these assumptions, the model points to an intrinsic value of about $328 per share.

Set against the recent $211.20 share price, that implies the stock screens as roughly 35.6% undervalued. The recent 25% single day drop after IBM’s Q2 earnings warning helps explain why the market price sits well below this cash flow based estimate, with investors clearly cautious about the timing and durability of those projected cash flows.

Overall, the DCF work suggests International Business Machines stock currently looks undervalued relative to its modeled cash generation.

Our Discounted Cash Flow (DCF) analysis suggests International Business Machines is undervalued by 35.6%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Is International Business Machines a Bargain on Earnings?

P/E is usually the cleanest way to compare a mature, diversified company like International Business Machines with its sector. On this basis, IBM currently trades at about 18.5x earnings, very close to the IT industry average of roughly 18.0x. However, it sits above a peer group average of around 10.5x, which suggests investors are still willing to pay a premium to those peers for IBM’s earnings profile.

A more tailored check that tries to account for International Business Machines' size, margins, sector and risk points to a fair P/E of about 33.1x. Set against the current 18.5x, that indicates the stock changes hands at a sizeable discount to where this framework would typically place it. For investors, that gap suggests the market is pricing IBM’s earnings more cautiously than the fair ratio implies.

On a P/E basis alone, International Business Machines stock looks undervalued relative to this fair multiple benchmark.

The International Business Machines Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for International Business Machines link the valuation puzzle to clear, testable assumptions about the company's future growth, margins and earnings, and they sit on the Community page. Each one connects a specific story about International Business Machines' potential catalysts and risks to an estimated fair value, so you can observe how the business develops and assess which version of events appears closest to reality over time.

The community is split on International Business Machines, with one camp leaning into AI and quantum upside and the other focused on execution and competition risks.

Bull case: 28% undervalued

"IBM's continued investment in generative AI and integration through acquisitions such as HashiCorp is set to enhance their software capabilities, potentially boosting software revenue and supporting long-term margin expansion through high-value recurring revenue…"

Bear case: 8% overvalued

"Intensifying dominance of hyperscale cloud providers such as Amazon, Microsoft, and Google is expected to further restrict IBM's ability to capture large cloud contracts and cloud-native workloads, increasingly relegating IBM to less strategic segments and capping long-term revenue growth as customers consolidate spend with the largest platforms…"

Do you think there's more to the story for International Business Machines? Head over to our Community to see what others are saying!

The Bottom Line

For International Business Machines, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple work point in the same direction, with the stock screening as undervalued rather than fully priced. The broader set of checks is mixed rather than emphatic, so the gap between intrinsic value and market price appears more like a potential opportunity than a clear mispricing.

What is likely to be decisive from here is whether IBM converts its AI, hybrid cloud and quantum ambitions into durable cash flow and earnings, or whether execution and competitive pressures continue to weigh on that outlook, turning the current discount into a value trap instead of upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.