International Business Machines (IBM) Faces Starbucks Risk And AI Updates, Is The Rally Already Priced In?

IBM Corp IBM | 0.00 |

International Business Machines (IBM) stock has been reacting to two competing storylines: Starbucks moving to replace IBM maintenance tools with in-house AI software, and IBM rolling out new AI focused products like Lightwell and upgraded IBM Bob.

Over the past quarter, International Business Machines has seen a 90 day share price return of 27.97%, and a 1 year total shareholder return of 5.37%, suggesting recent momentum contrasts with more modest gains over a longer horizon.

The recent share price reaction, including a 1 day move that declined 2.23% and a 30 day share price return of 6.42%, reflects investors weighing the risk of clients like Starbucks shifting in house, against IBM’s AI focused launches such as Bob upgrades and the Lightwell rollout.

If IBM’s AI push has you thinking about where else AI is reshaping software, this is a good moment to scan 63 profitable AI stocks that aren't just burning cash.

International Business Machines is clearly executing on a big AI and mainframe modernization push, yet the stock’s sharp 90 day move and current price just above its latest analyst target raise a simpler question: is that strength already in the valuation?

Most Popular Narrative: 15.3% Overvalued

The most followed narrative on International Business Machines sets a fair value of $256.08 against the recent $295.30 share price, so it sees the current rally as running ahead of that estimate while still grounded in specific earnings, margin and multiple assumptions.

IBM represents a defensive growth technology investment transitioning into a software and AI led enterprise platform company. While topline growth remains moderate, improving mix (software), strong margins, and durable cash flows underpin a compelling long-term investment case, particularly for investors seeking exposure to enterprise AI with lower volatility than pure-play SaaS peers.

Want to see how that fair value number is built? According to kapirey, the narrative leans heavily on software mix, cash generation strength and a future earnings multiple that assumes IBM keeps shifting toward higher margin businesses.

Result: Fair Value of $256.08 (OVERVALUED)

However, International Business Machines still faces two clear swing factors: slower than expected AI adoption across its software and consulting franchises, and pressure if major clients accelerate in house replacements like Starbucks.

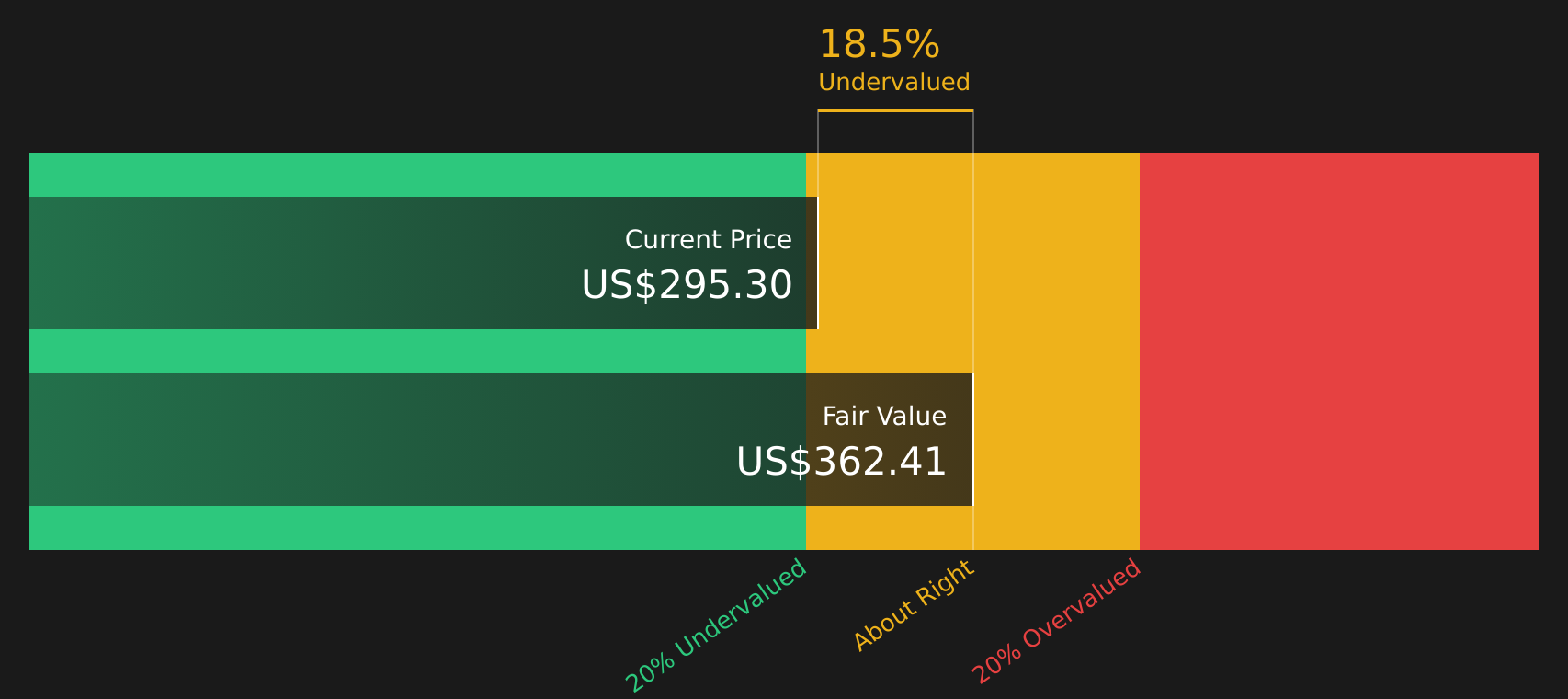

Another View: SWS DCF Fair Value For International Business Machines

The user narrative sees International Business Machines as 15.3% overvalued at $295.30 versus a $256.08 fair value, but our DCF model points the other way, with a fair value of $362.41 and the stock trading at an 18.5% discount. Two thoughtful models, two very different answers. Which assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out International Business Machines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With International Business Machines sitting between clear risks and real rewards, this is a good time to review the details yourself, decide what matters most for your portfolio, and then weigh those trade offs against the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond International Business Machines?

If IBM has sharpened your focus on what belongs in your portfolio next, do not stop here. The right list of fresh ideas can be just as important.

- Target steady compounding potential by checking companies with reliable income profiles and strong yields through the 9 dividend fortresses.

- Hunt for quality at a reasonable price by reviewing companies flagged as potentially mispriced using the 44 high quality undervalued stocks.

- Prioritize resilience by scanning companies with stronger financial footing and fundamentals via the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.