Intuitive Surgical (ISRG) Stock Looks Fully Priced After Its 34% Five Year Gain

Intuitive Surgical, Inc. ISRG | 0.00 |

Intuitive Surgical stock has delivered a 34.4% gain over the past five years, yet its current checks present a mixed picture, with the Discounted Cash Flow (DCF) intrinsic value estimate suggesting the share price is roughly in line with fair value while market multiples lean expensive.

- Over five years, Intuitive Surgical has returned 34.4%, which points to meaningful long term value creation for shareholders despite more recent price pressure.

- Adoption of the company’s robotic surgery platforms can support expectations for future cash flows, but ongoing regulatory attention and increasing competition may limit how much investors are willing to pay for that growth.

- With the stock scoring only 2 out of 6 on broader valuation checks, the current level appears expensive rather than a clear bargain.

For investors, the debate is whether Intuitive Surgical’s current price already reflects its cash flow potential, or if the recent pullback has left enough margin of safety to justify the premium multiples.

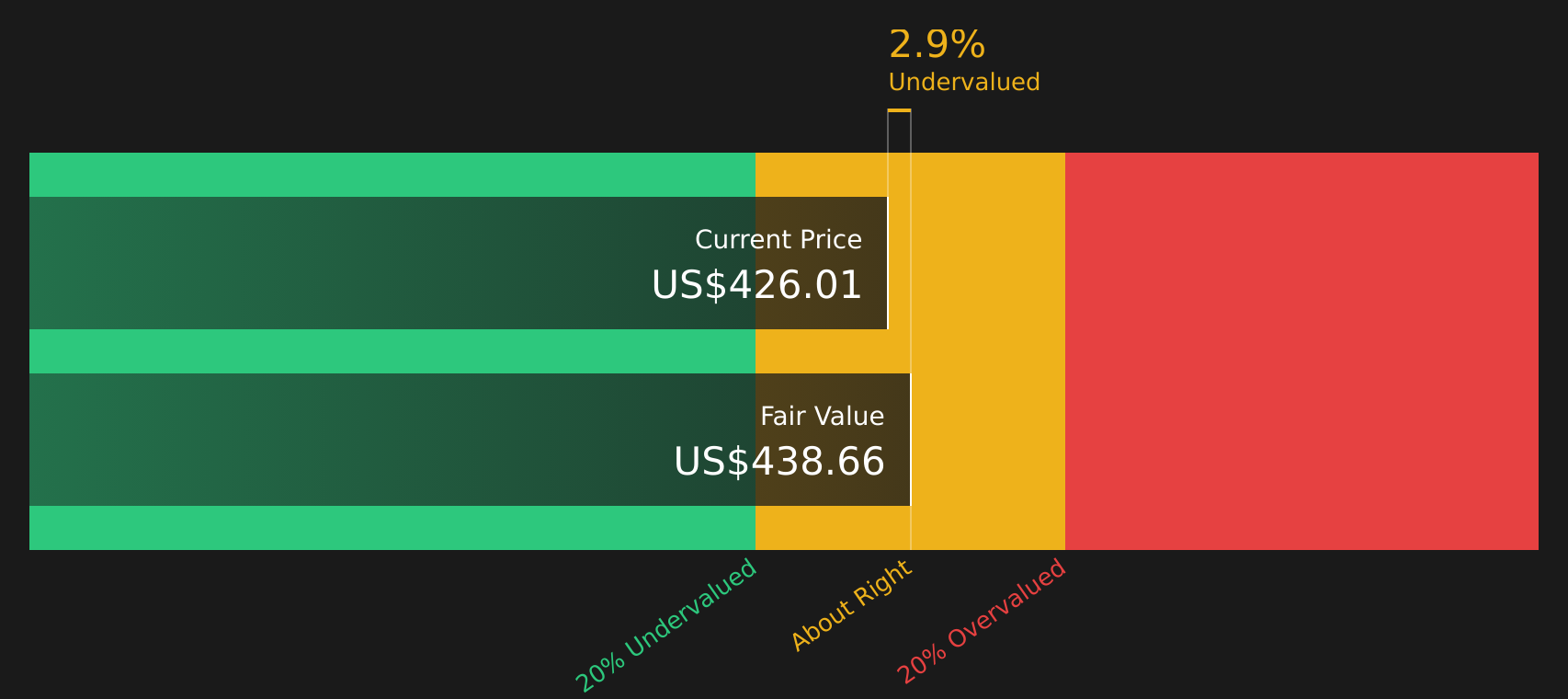

Is Intuitive Surgical Fairly Priced on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what Intuitive Surgical should be worth based on its projected cash generation. Intuitive Surgical currently produces about $2.3b in free cash flow over the latest twelve months, and the model assumes those cash flows continue growing rather than shrinking, consistent with expectations for its established robotic surgery platform.

Under these assumptions, the 2 Stage Free Cash Flow to Equity model points to an intrinsic value of about $439 per share. That is only around 2.9% above the current share price, which suggests Intuitive Surgical looks roughly fairly valued on a pure cash flow basis rather than offering a wide discount. The recent leadership changes and ongoing regulatory attention highlighted in recent news help explain why the market is reluctant to price the stock far above its cash flow estimate.

On this DCF view, Intuitive Surgical stock comes across as about fairly valued, with its current price already close to the model’s estimate of intrinsic worth.

Intuitive Surgical is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

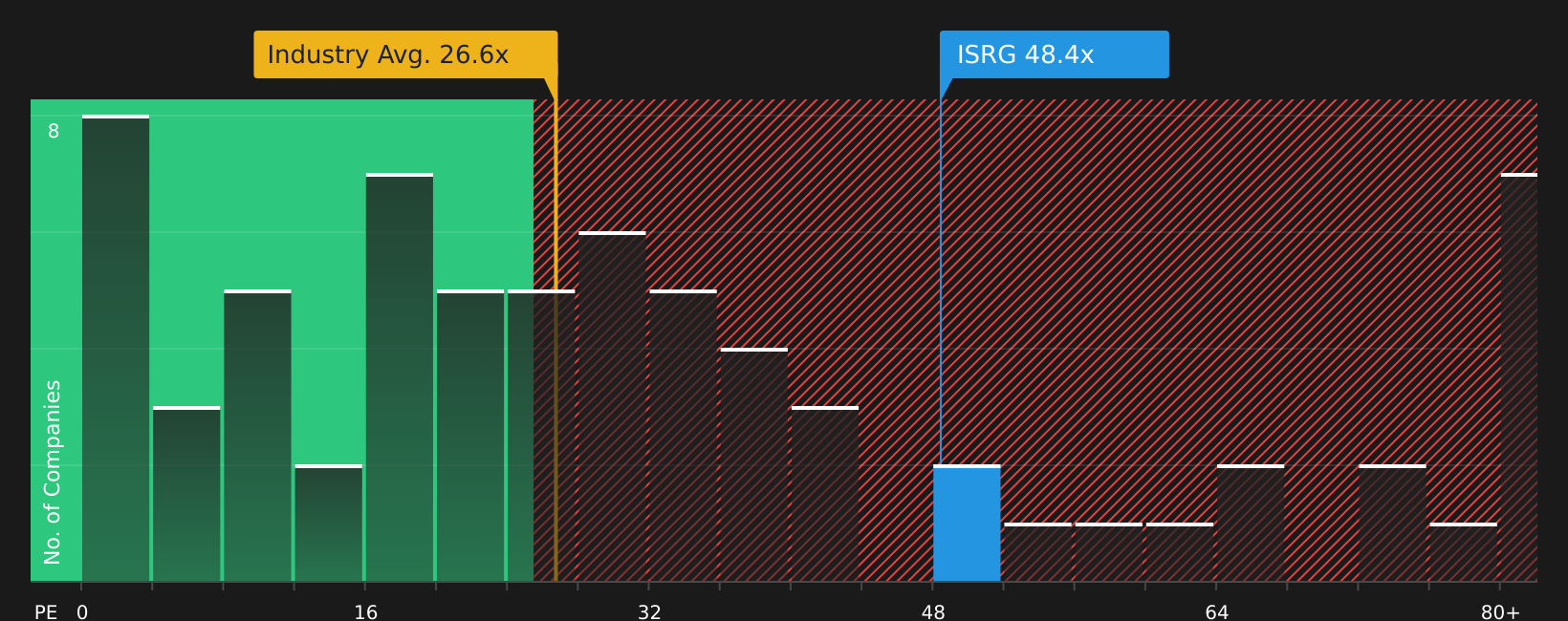

Does Intuitive Surgical Look Pricey on Earnings?

The P/E ratio fits Intuitive Surgical well because earnings are a key focus for many investors watching its profitability. Intuitive Surgical currently trades on about 50.6x earnings, compared with an average P/E of roughly 26.5x across the wider Medical Equipment industry and a peer average of 26.3x, so the stock carries a substantial premium on this measure.

A more tailored fair P/E ratio that accounts for Intuitive Surgical’s size, margins and risk profile sits closer to 34.1x, which is well below the current 50.6x. That gap suggests investors are paying a high price for each dollar of current earnings, even after considering company specific strengths and risks highlighted in recent news.

On the P/E multiple, Intuitive Surgical stock screens as clearly overvalued relative to both its sector and a more customised fair value benchmark.

The Intuitive Surgical Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Intuitive Surgical pick up where the valuation puzzle leaves off by spelling out which assumptions about Intuitive Surgical's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price. Each narrative links a specific fair value estimate to a clear story about the company’s potential catalysts and risks, so you can see over time which scenario appears to be unfolding on the Community page.

Community views on Intuitive Surgical sit wide apart, with some investors focused on the strength of its ecosystem while others fixate on pricing pressure and regulatory risk.

Bull case: 20% undervalued

"ISRG’s robust business model and strong moat come from this recurring revenue, as hospitals must continuously purchase instruments, maintenance services, and software updates…"

Bear case: roughly fairly valued

"Intensifying global healthcare cost pressures and expanding government regulation are expected to force more aggressive pricing controls and reimbursement scrutiny in key markets…"

Do you think there's more to the story for Intuitive Surgical? Head over to our Community to see what others are saying!

The Bottom Line

For Intuitive Surgical, the Discounted Cash Flow (DCF) view points to a share price that already sits close to intrinsic value, while the P/E multiple suggests the stock is overvalued versus peers and a tailored fair ratio. That split reflects a business that generates solid cash flows, yet is still priced richly on earnings expectations. With broader valuation checks screening weak, the key question is whether Intuitive Surgical can keep justifying its premium multiples through sustained growth in its robotic surgery ecosystem or whether sentiment cools and the valuation settles closer to industry norms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.