Intuitive Surgical Stock And 2 Cash Rich Picks for Higher Interest Rates

Intuitive Surgical, Inc. ISRG | 0.00 |

With the Federal Reserve talking tougher on inflation and signaling a possible rate hike within months, investors are rethinking how comfortable they feel with heavily indebted companies. Higher borrowing costs can put more pressure on weaker balance sheets, while cash rich, low debt businesses may have more room to adjust. This article looks at 3 stocks from a Cash Rich, Low Debt Companies screener that appear closely tied to the current interest rate story. The focus is on how their financial footing might help or hurt as money becomes more expensive, and what that could mean for long term investors watching Fed Chair Kevin Warsh’s next move.

Intuitive Surgical (ISRG)

Overview: Intuitive Surgical develops robotic and digital tools such as the da Vinci Surgical System and Ion endoluminal platform that help doctors perform minimally invasive procedures, particularly in surgery and lung diagnostics. The company pairs its systems with instruments, training, services, and data tools so hospitals can run large, technology driven surgery programs.

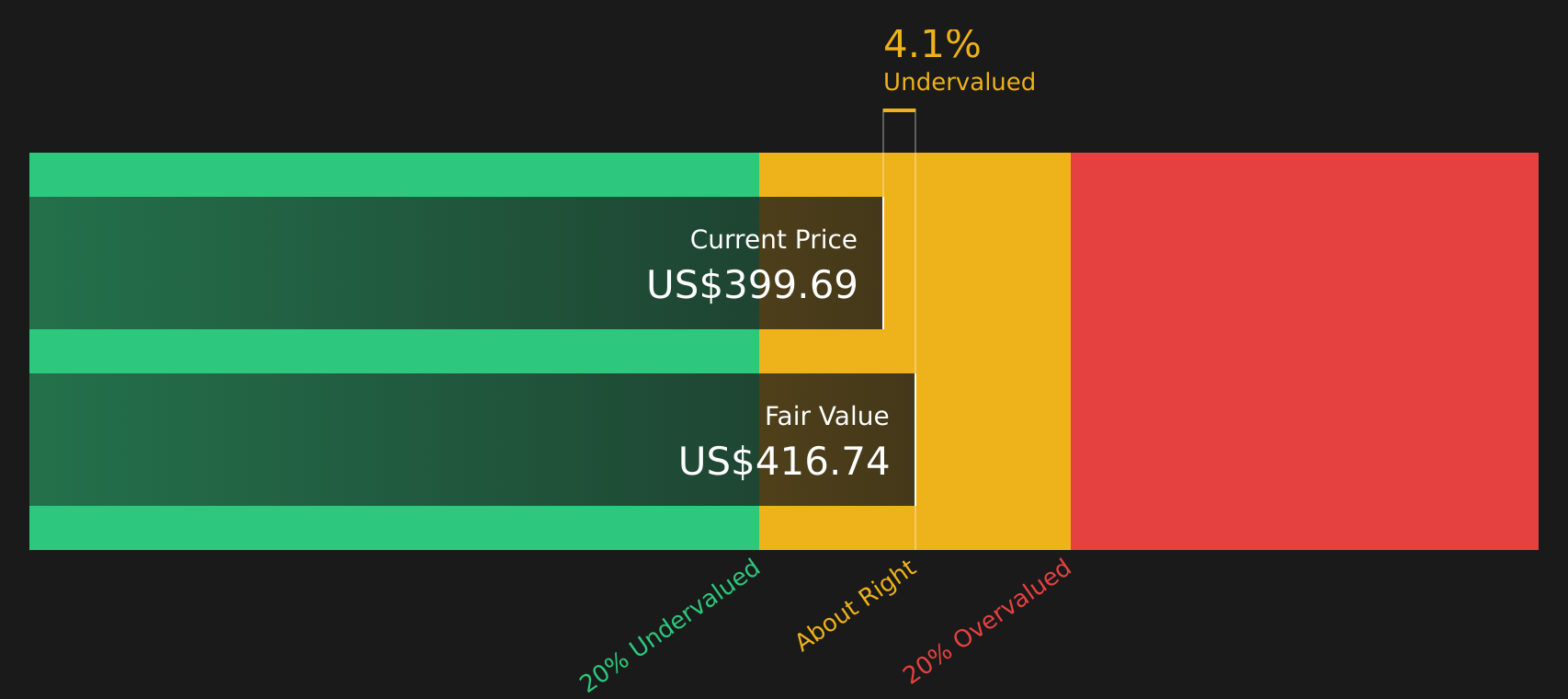

Operations: Intuitive Surgical generates about US$10.6b in revenue, almost entirely from surgical and medical equipment, with roughly US$7.1b from the United States and US$3.5b from other countries.

Market Cap: US$142.3b

Intuitive Surgical stands out in a rate hike setting because it couples a strong net cash position and consistent free cash flow with a business model where roughly 83% of revenue comes from recurring instruments and services tied to its installed base of over 9,500 da Vinci systems. That financial strength may help Intuitive Surgical absorb higher funding costs while continuing to invest in upgrades such as the da Vinci 5 platform. At the same time, recalls and regulatory scrutiny add some operational risk. Earnings growth, high quality cash generation, and broad analyst optimism contrast with a rich P/E and governance questions around executive pay. This creates a situation where the quality case is clear, but the debate on valuation and risk remains open.

Intuitive Surgical’s rich P/E and strong cash position pose a significant question for investors, and the turning point may be hidden inside the DCF valuation analysis for Intuitive Surgical

Vertex Pharmaceuticals (VRTX)

Overview: Vertex Pharmaceuticals is a biotechnology company that develops and sells medicines for serious diseases, with a core franchise in cystic fibrosis and a growing portfolio in sickle cell disease, beta thalassemia, acute pain, kidney disorders, type 1 diabetes and other rare conditions. Its treatments reach patients worldwide through pharmacies, hospitals and clinics, with headquarters in Boston and operations across the United States, Europe and other international markets.

Operations: Vertex Pharmaceuticals generates about US$12.2b in revenue from pharmaceuticals, with roughly US$7.7b from the United States, US$3.6b from Europe and US$1.0b from other regions.

Market Cap: US$118.9b

Vertex Pharmaceuticals stands out in a rising rate setting because its high net cash balance, negligible debt and strong operating cash flows reduce exposure to more expensive borrowing, even as it invests in a broad pipeline beyond cystic fibrosis. Investors get a mix of high returns on equity, recent profitability and share buybacks, but also concentration risk in CF, ongoing R&D and regulatory uncertainty that could challenge future margins. With the stock trading on a higher P/E than the wider biotech industry but below some peers, and analysts expecting future growth from drugs like CASGEVY and JOURNAVX plus nephrology programs, the key question is whether this balance of quality, pipeline potential and risk is already reflected in the price or if the market is underestimating what comes next.

Vertex Pharmaceuticals’ growth story in CF, gene editing and nephrology is accelerating, but the real tension is whether the current price fully reflects that potential or not. The analysis report for Vertex Pharmaceuticals stops just short of answering the biggest open question.

Regeneron Pharmaceuticals (REGN)

Overview: Regeneron Pharmaceuticals is a US based biotech company that discovers, develops, manufactures, and sells medicines for serious diseases, with major products in eye disorders like wet age related macular degeneration, inflammatory conditions through Dupixent, cancer, cardiovascular disease, and rare genetic disorders.

Operations: Regeneron Pharmaceuticals generates about US$14.9b in revenue from the discovery, development, and commercialization of medicines for serious diseases.

Market Cap: US$63.4b

Regeneron Pharmaceuticals offers a mix of high quality biologic franchises such as EYLEA and Dupixent, a deep pipeline across oncology, gene editing, and siRNA, and a balance sheet built around net cash and liquidity that can cushion higher interest costs if Fed policy tightens. At the same time, the company faces pressure from biosimilar competition, pricing scrutiny on flagship drugs, and a history of earnings decline that puts more weight on pipeline execution and new approvals such as cemdisiran for gMG. With experienced governance, active partnerships and share repurchases in play, the key question is whether the current valuation fully reflects this blend of resilience, funding risk and long term optionality in a higher rate environment.

Regeneron Pharmaceuticals looks like a classic case where resilient franchises and a deep pipeline may be masking a more complex risk reward trade off. The analyst forecasts for Regeneron Pharmaceuticals could show why the real story might just be getting started.

The three stocks covered here are just a starting point, with the full Cash Rich, Low Debt Companies screener surfacing 486 more businesses that pair strong balance sheets with equally compelling stories across different sectors and regions in the Cash-Rich, Low-Debt Companies screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you, so you can focus on the highest conviction opportunities in this theme.

Take Control of Your Investment Journey

If Intuitive Surgical or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Others Catch On?

Fresh ideas can move from quiet to flying fast as momentum builds and prices shift. Spot potential breakouts that are under the radar for now, before the crowd acts.

- Target durable income streams while rates shift by reviewing a curated group of high yield stocks in the 7 dividend fortresses before payouts or prices are repriced.

- Explore companies involved in machine learning by scanning hand picked businesses powering infrastructure, chips and platforms through the 49 AI infrastructure stocks while they may still be under the radar.

- Consider potential electrification trends by checking a focused shortlist of miners and producers in the 8 top copper producer stocks before any demand pressures are fully reflected in the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.