Is ASML Holding (ASML) Expensive Following Its Raised 2026 Revenue Outlook?

ASML Holding NV ADR ASML | 0.00 |

ASML Holding (NasdaqGS:ASML) has lifted its 2026 revenue outlook again after reporting Q2 net sales of €9.3b and net income of €2.9b, reinforcing its central role in advanced chip equipment.

ASML Holding's share price has moved sharply higher over the past year, with a 90 day share price return of 24.35% and a year to date share price return of 55.98%. The 1 year total shareholder return of 145.31% points to strong momentum around its role in AI focused chip equipment and recent upgrades to its 2026 outlook.

If ASML's run has you thinking about where else AI related spending could flow, it can be useful to scan a wider set of AI enablers through 52 AI infrastructure stocks

Bulls view ASML Holding's monopoly-style position in EUV and its raised 2026 guidance as evidence that the premium is justified, while bears worry that recent share gains already reflect a lot of AI optimism, so what do current valuation markers actually say?

Preferred P/E of 56x: Is it justified?

ASML Holding currently trades on a P/E of 56x, which prices in a lot of optimism, yet it still sits below several reference points investors often watch.

The P/E ratio compares the company’s share price to its earnings per share and is a quick way to see how much investors are paying for current profits. For a highly specialized chip equipment supplier like ASML, a higher P/E often reflects expectations that earnings can keep growing and that its position in advanced lithography supports strong profitability.

Here, ASML’s 56x P/E is below the US Semiconductor industry average of 62.6x and below the peer average of 60.5x. This means the stock is not the most aggressively priced within its group. However, our estimated fair P/E of 54.4x suggests the market valuation is slightly ahead of where the SWS fair ratio points, which is a level investors may watch if sentiment or growth expectations change.

Result: Price-to-earnings of 56x (ABOUT RIGHT)

However, ASML Holding’s premium P/E and heavy reliance on advanced lithography spend leave the story exposed if chip capital expenditure or AI infrastructure budgets cool faster than expected.

Another view on ASML Holding’s valuation

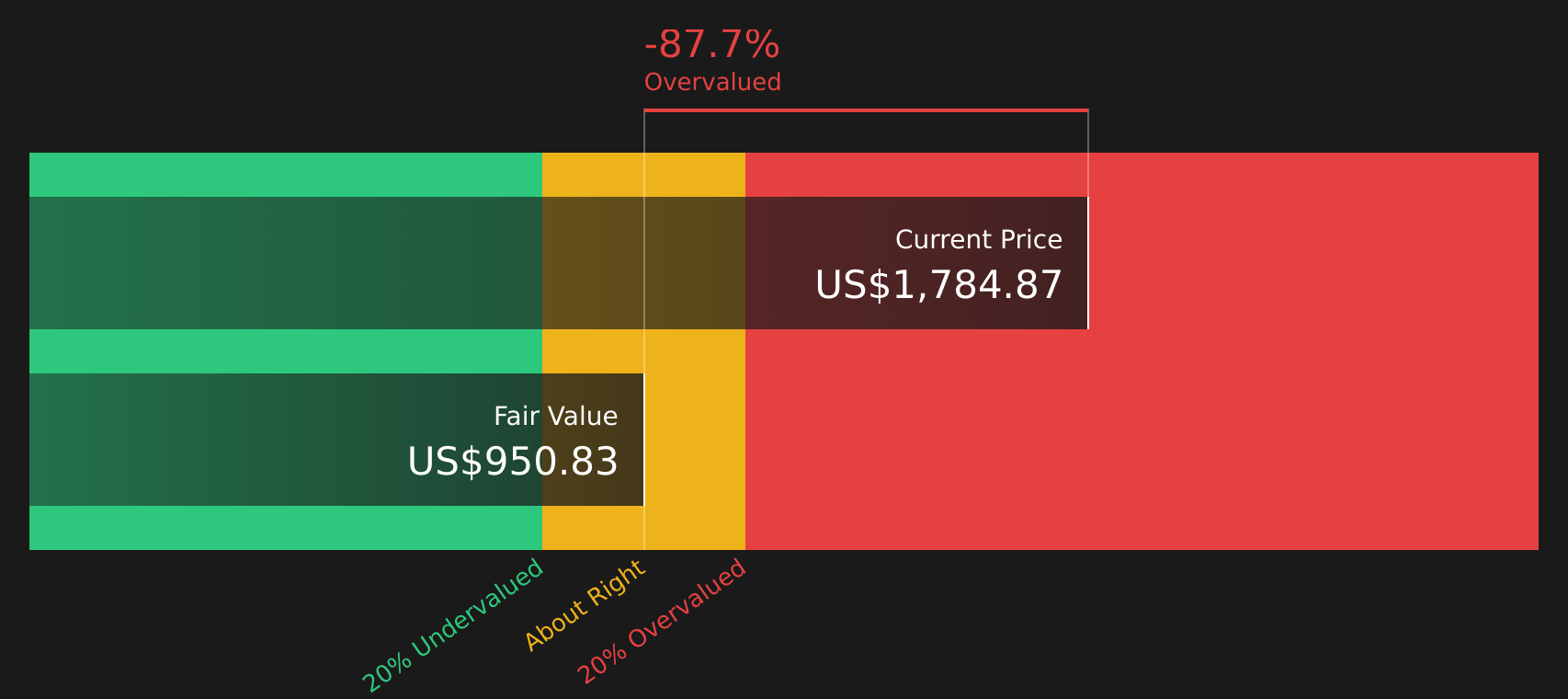

While the current 56x P/E for ASML Holding sits close to the 54.4x fair ratio, our DCF model presents a different perspective. At a share price of $1,815.27 versus an estimated future cash flow value of $942.78, the stock appears expensive, which raises the question of which signal you consider more informative.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASML Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With ASML Holding attracting strong interest, it can be helpful to move quickly from headline sentiment to your own scorecard of what really matters. To see what optimistic investors are focusing on, review the 3 key rewards

Looking for more investment ideas beyond ASML Holding?

ASML Holding may be front of mind right now, but you do not want to miss other stocks that could fit your portfolio goals and risk profile.

- Target resilience by scanning companies with healthier financial footing through the solid balance sheet and fundamentals stocks screener (48 results).

- Spot potential mispricings by reviewing the 47 high quality undervalued stocks that may align better with your return expectations.

- Strengthen your income stream by checking out the 10 dividend fortresses that aim to pair yield with durability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.