Is ASML Holding (NasdaqGS:ASML) Fairly Valued As Earnings Near?

ASML Holding NV ADR ASML | 0.00 |

ASML Holding (ASML) edged 1.22% higher in the latest session, outpacing the S&P 500, as investors looked ahead to the company’s July 15, 2026 earnings release and closely watched expectations for EPS and revenue.

At a share price of $1,768.65, ASML Holding has posted a 22.09% 3 month share price return and a 51.97% year to date share price return, while the 1 year total shareholder return of 122.60% suggests momentum has been strong even through shorter term pullbacks such as the 4.04% share price decline over the past week.

If ASML Holding has you looking at the broader semiconductor supply chain, this is a good moment to see what other AI related plays are doing through our screener of 52 AI infrastructure stocks.

After the sharp run in ASML Holding’s share price over the past year, followed by a recent pullback, investors may now be asking whether the current valuation already reflects most of the positive developments or if there is still meaningful upside potential ahead.

Preferred P/E of 58.8x: Is it justified?

ASML Holding trades on a P/E of 58.8x at a last close of $1,768.65, which screens slightly cheaper than both its peer group and the wider US semiconductor industry on this metric.

The P/E ratio compares the company’s current share price to its earnings per share and is a common way investors gauge how much they are paying for each dollar of profit. For a large, profitable semiconductor equipment supplier like ASML Holding, this multiple reflects what the market is willing to pay today for earnings that are expected to grow and remain resilient through the cycle.

Relative to the peer average P/E of 60.4x and the US semiconductor industry average of 61.3x, ASML Holding trades at a modest discount. This suggests the market is not pricing it at the very top of the group despite its track record of earnings growth and very high current and forecast return on equity. Against an estimated fair P/E of 53.3x, however, the shares sit above the level that regression analysis suggests the multiple could move toward over time. This points to some valuation pressure if growth expectations do not fully play out as implied.

Result: Price-to-earnings of 58.8x (ABOUT RIGHT)

However, there are clear risks to watch, including ASML Holding’s sensitivity to semiconductor equipment spending cycles and potential shifts in demand for advanced lithography tools.

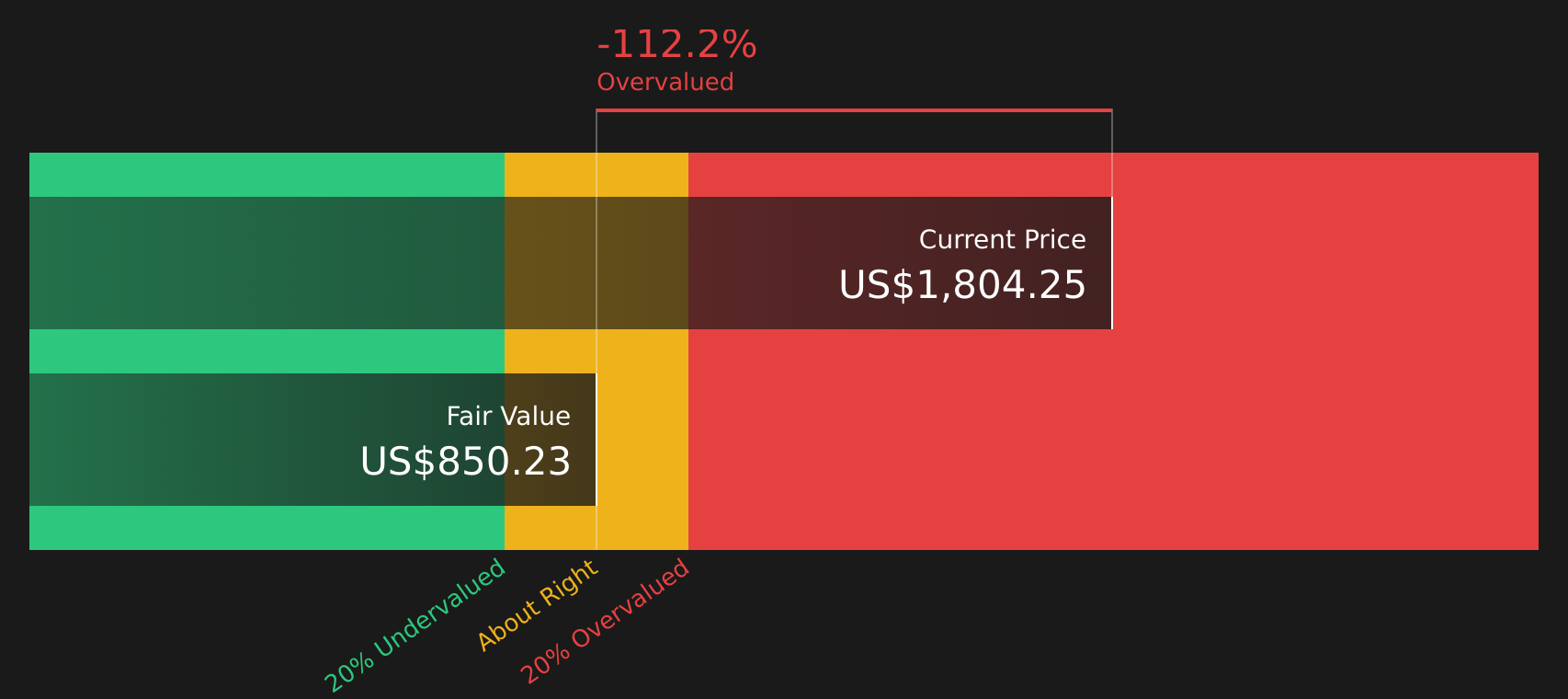

Another View on ASML Holding: Cash Flows Paint a Tougher Picture

While ASML Holding appears only slightly expensive on a P/E of 58.8x versus a fair ratio of 53.3x, our DCF model indicates a much wider gap. The current $1,768.65 share price stands well above an estimated future cash flow value of $872.71, which raises the question of which signal to place greater weight on.

To see how the SWS DCF model addresses this gap and what assumptions support it, take a closer look at the full valuation breakdown through Look into how the SWS DCF model arrives at its fair value..

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASML Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this ASML Holding story seems to balance caution and optimism, consider reviewing both the potential benefits and the risks by checking the 3 key rewards.

Looking for more ASML Holding sized investment ideas?

Do not stop at ASML Holding; use the Simply Wall St screener to uncover fresh stock ideas that could better match your risk, income, and growth preferences.

- Target stability first by checking companies highlighted in the 72 resilient stocks with low risk scores that may better fit a cautious approach.

- Hunt for value by scanning the 44 high quality undervalued stocks where strong fundamentals and pricing can line up more attractively.

- Boost your income focus by reviewing the 9 dividend fortresses and see which stocks offer higher yields with supporting financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.