Is Block (SQ) A Potential Opportunity After Recent Share Price Weakness?

Block XYZ | 0.00 |

With Block on many watchlists, the key question for you is whether the current share price properly reflects what the company might be worth over the long run.

Recently, the stock closed at US$66.63, with returns of 4.0% over the past year, 4.6% over three years, 2.3% year to date, a fall of 8.9% over the past month, and a decline of 4.5% over the last week. This may suggest shifting views on both potential and risk.

Recent news coverage has focused on how Block fits into the broader diversified financials space and how investors are weighing its role in the digital payments ecosystem. Commentary has also highlighted how sentiment around growth-focused financial technology stocks has been changing. This provides important context for the recent share price moves.

On Simply Wall St’s valuation checks, Block scores 3 out of 6. The rest of this article will walk through what that means by looking at different valuation methods, before finishing with a more holistic way to think about the stock’s value.

Approach 1: Block Excess Returns Analysis

The Excess Returns model looks at how much earnings Block can generate above the return that investors typically require on its equity, then sums those “excess” profits over time to estimate what the stock might be worth today.

For Block, the model starts with a Book Value of $36.48 per share and a Stable EPS of $5.45 per share, based on weighted future Return on Equity estimates from 9 analysts. The implied Average Return on Equity is 12.04%. Against a Cost of Equity of $3.39 per share, this points to an Excess Return of $2.06 per share, which is the value created above the required return.

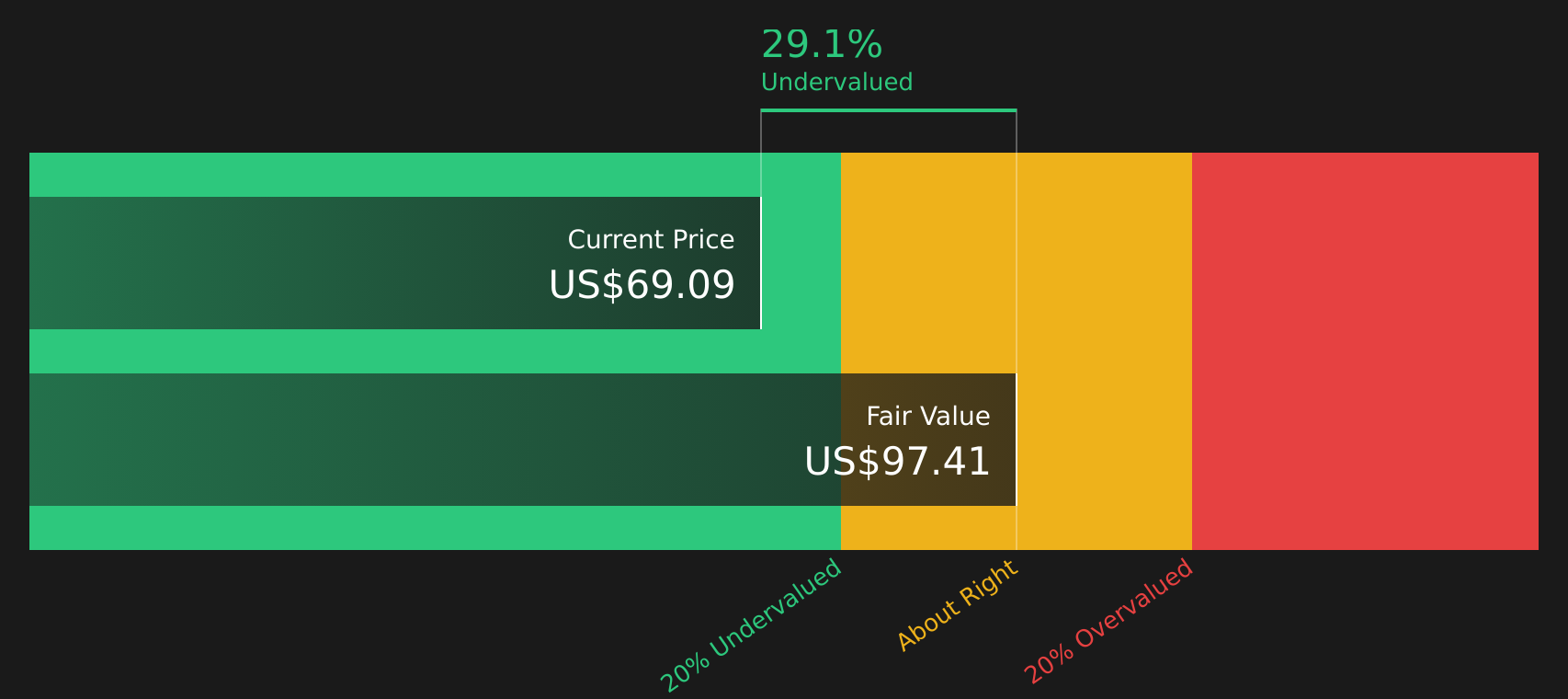

The Stable Book Value used in the model is $45.25 per share, sourced from weighted future Book Value estimates from 7 analysts. Combining these inputs, Simply Wall St’s Excess Returns framework arrives at an intrinsic value of about $97.38 per share.

Compared with the recent share price of US$66.63, this Excess Returns estimate suggests Block is 31.6% undervalued based on these assumptions.

Result: UNDERVALUED

Our Excess Returns analysis suggests Block is undervalued by 31.6%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: Block Price vs Earnings

For a profitable company like Block, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. A higher or lower P/E often reflects how the market is balancing growth expectations against the risks investors see in the business.

Block currently trades on a P/E of 49.59x. That compares with an average P/E of 16.57x for the Diversified Financial industry and a peer group average of 10.74x. On these simple comparisons, the stock is priced well above both its industry and peer reference points.

Simply Wall St’s “Fair Ratio” for Block is 27.27x. This is a proprietary P/E level that reflects factors such as the company’s earnings profile, its industry, profit margins, market capitalization and risk characteristics. Because it ties the valuation multiple to company specific drivers rather than broad group averages, it can give a more tailored reference point than a straight peer or sector comparison. Set against this Fair Ratio, Block’s current P/E of 49.59x is higher, which indicates that the shares appear overvalued on this metric alone.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Block Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in as a simple way for you to connect the story you believe about Block with concrete numbers like future revenue, earnings, margins and a fair value.

A Narrative on Simply Wall St is your own story about the company, captured through assumptions such as how Block’s Cash App and Square businesses might develop, what profit margins could be, and what P/E you think is reasonable. The platform then turns that story into a forward forecast and a Fair Value that you can compare with today’s share price.

These Narratives sit inside the Community page on Simply Wall St, are easy to set up and adjust, and they update automatically when fresh data such as earnings, regulatory news or new product information is added. This means your view on Block does not stay frozen in time.

For Block specifically, one investor might align with the more cautious Narrative that points to a Fair Value around US$60.88, while another might follow a more optimistic Narrative closer to US$112.45. Comparing either of those to the current share price may help you decide whether the stock appears closer to fully priced, expensive or cheap based on the story you believe.

For Block however we will make it really easy for you with previews of two leading Block Narratives:

Here is how a more optimistic Narrative compares with a more cautious one, using the same current share price but very different assumptions about the future.

Fair value: US$90.52 per share

Current price vs this fair value: about 26% below this Narrative fair value

Revenue growth assumption: 11.13% per year

- Focuses on faster product rollouts across Cash App and Square, embedded banking, and cryptocurrency tools that widen Block's user base and deepen engagement.

- Uses analyst assumptions that earnings, margins and share count trends support higher future earnings, which are then discounted back using a 7.54% rate.

- Leans on a higher 2029 P/E multiple and a consensus price target that sits above the current share price, while still flagging competition, credit risk and crypto exposure as key risks to watch.

Fair value: US$60.88 per share

Current price vs this fair value: about 9% above this Narrative fair value

Revenue growth assumption: 8.24% per year

- Emphasizes heavier regulatory and compliance burdens, cyber risk, competition and pressure from government backed payment systems that could keep a lid on margins.

- Builds in lower revenue growth and profit margin assumptions, a higher discount rate of 7.62%, and a future P/E of 16.25x that is below the consensus Narrative.

- Arrives at a fair value close to the lower end of analyst targets, with the view that current market expectations already bake in a lot of improvement in earnings and profitability.

Together, these Narratives frame a realistic range of outcomes for Block based on different views of growth, risk and what multiple the market might be willing to pay for future earnings. If you want to see how this range compares with other investor views and update it as new data arrives, take a look at the full community range for Block, including the consensus view, bull and bear cases See what the community is saying about Block.

Do you think there's more to the story for Block? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.