Is Fastenal (FAST) Fairly Valued On Its Dividend Increase?

Fastenal Company FAST | 0.00 |

Fastenal (FAST) is back in focus after its board approved an 8.3% increase in the quarterly dividend to $0.26 per share, payable in cash on August 25, 2026.

Fastenal's share price has been relatively steady, with a 1-day share price return of 0.30% and a 90-day share price return of 1.51%. The year-to-date share price return of 14.96% sits alongside a 5-year total shareholder return of 95.64%, which indicates stronger momentum over longer periods than in recent weeks.

If Fastenal's mix of income and long-term compounding appeals to you, it could be a good moment to see what else is out there via 34 power grid technology and infrastructure stocks

Fastenal looks like a solid industrial distributor that is comfortable raising its dividend, but a strong business is not always a cheap stock. After this latest move, how does the current price stack up against what you are actually getting?

Most Popular Narrative: Fairly Valued

Fastenal's last close at $46.49 sits right on top of the most followed narrative fair value of $46.49, so the focus shifts to what is expected to drive future returns.

The company is expanding its Fastenal Managed Inventory (FMI) technology which currently represents over 43% of revenue, aiming to enhance revenue growth by increasing efficiency in customer supply chains.

Fastenal aims to increase its digital footprint to represent 66-68% of sales, up from 61%, potentially boosting revenue by optimizing purchasing and operational efficiency.

Want to understand why a seemingly full valuation still attracts attention? This narrative leans heavily on compounding earnings, firm margins, and a richer multiple than many peers. The numbers behind that mix are what really matter.

Result: Fair Value of $46.49 (ABOUT RIGHT)

However, Fastenal's story can change quickly if trade tensions increase tariff and freight costs or if higher inventory levels start to weigh on cash flow and flexibility.

Another View on Fastenal's Valuation

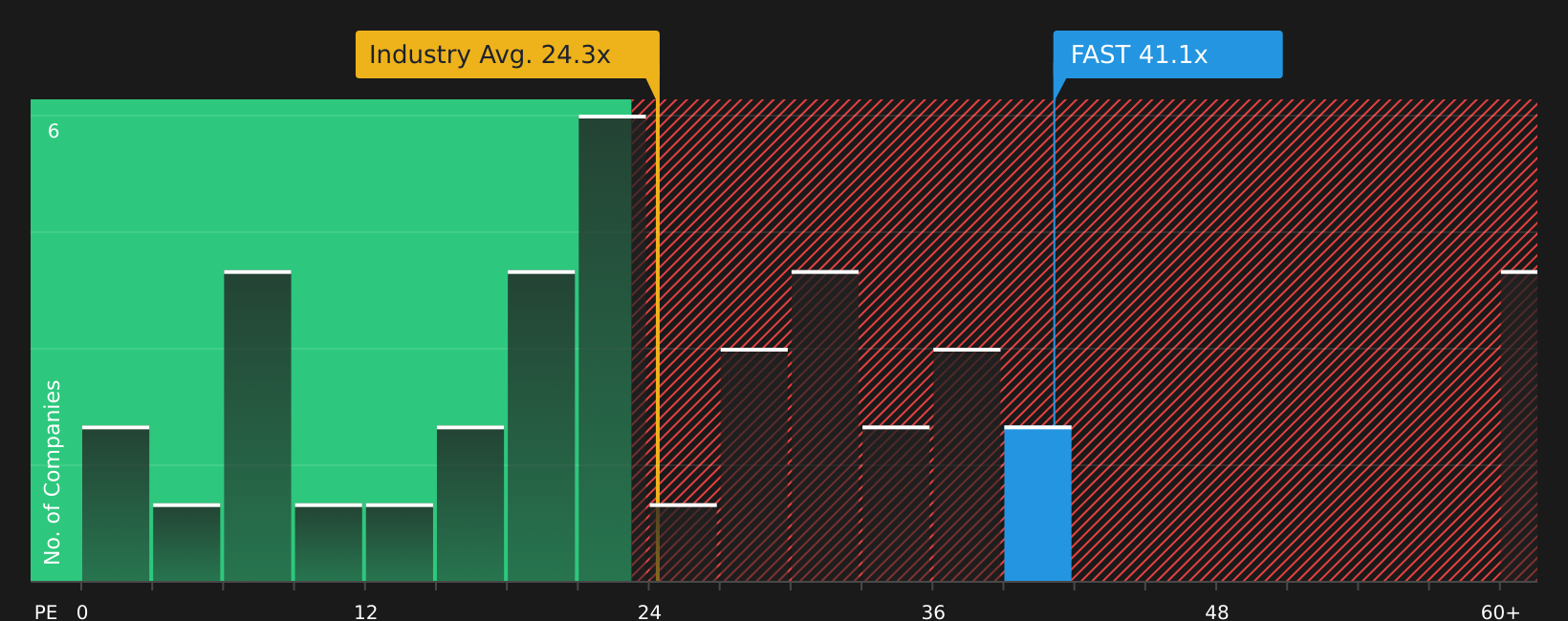

The fair value narrative around Fastenal leans heavily on future growth and margins, but the current P/E of 41.1x tells a different story. That multiple sits well above the US Trade Distributors industry at 24.3x, the peer average at 25.8x, and even the fair ratio of 29.6x.

In practice, that gap means you are paying a higher price for each dollar of Fastenal's earnings compared with both peers and where the fair ratio suggests the P/E could drift over time. This raises the bar for execution rather than lowering it. The question is whether you are comfortable paying that kind of premium for this mix of growth, quality and income.

Next Steps

Feeling unsure whether Fastenal's mix of pricing, quality, and income justifies this valuation premium? You can review the full picture with 2 key rewards and 1 important warning sign

Looking for more investment ideas beyond Fastenal?

If Fastenal has you thinking more carefully about price, quality, and income, do not stop here. Broader ideas can help you compare opportunities and sharpen your decisions.

- Target dependable growth with stronger fundamentals by scanning companies in the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for quality at a reasonable price by reviewing companies in the 45 high quality undervalued stocks.

- Prioritize stability and smoother sleep at night by focusing on companies in the 78 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.