Is It Time To Reassess IBM (IBM) After Its Recent Share Price Weakness?

IBM Corp IBM | 0.00 |

- If you are wondering whether International Business Machines stock is pricing in too much optimism or leaving value on the table, the starting point is understanding how its current share price compares with underlying fundamentals.

- The stock recently closed at US$231.31, with returns of 0.1% over 7 days, a 5.6% decline over 30 days, a 20.6% decline year to date, and gains of 6.0% over 1 year, 110.8% over 3 years and 104.3% over 5 years. These figures set the backdrop for any valuation check.

- Recent headlines around International Business Machines have focused on its position in enterprise technology and its role in areas such as cloud, software and services. These factors can shape how investors think about its long term earnings potential and risk profile, and are often front of mind when markets reassess what they are willing to pay for the stock.

- On Simply Wall St's valuation model, International Business Machines scores a 5 out of 6 for being undervalued across different checks. This sets up a closer look at the usual valuation tools like P/E multiples and cash flow models, followed by a final section that walks through a more complete way to think about value beyond just a single metric.

Approach 1: International Business Machines Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes forecasts of a company’s future cash flows and discounts them back to today’s dollars to estimate what the whole business might be worth right now.

For International Business Machines, the model uses a 2 Stage Free Cash Flow to Equity approach, starting from last twelve months free cash flow of about $12.2b. Analysts provide explicit free cash flow estimates out to 2030, such as $15.7b in 2026 and $18.4b in 2028, with Simply Wall St extending the projections further using its own assumptions for later years.

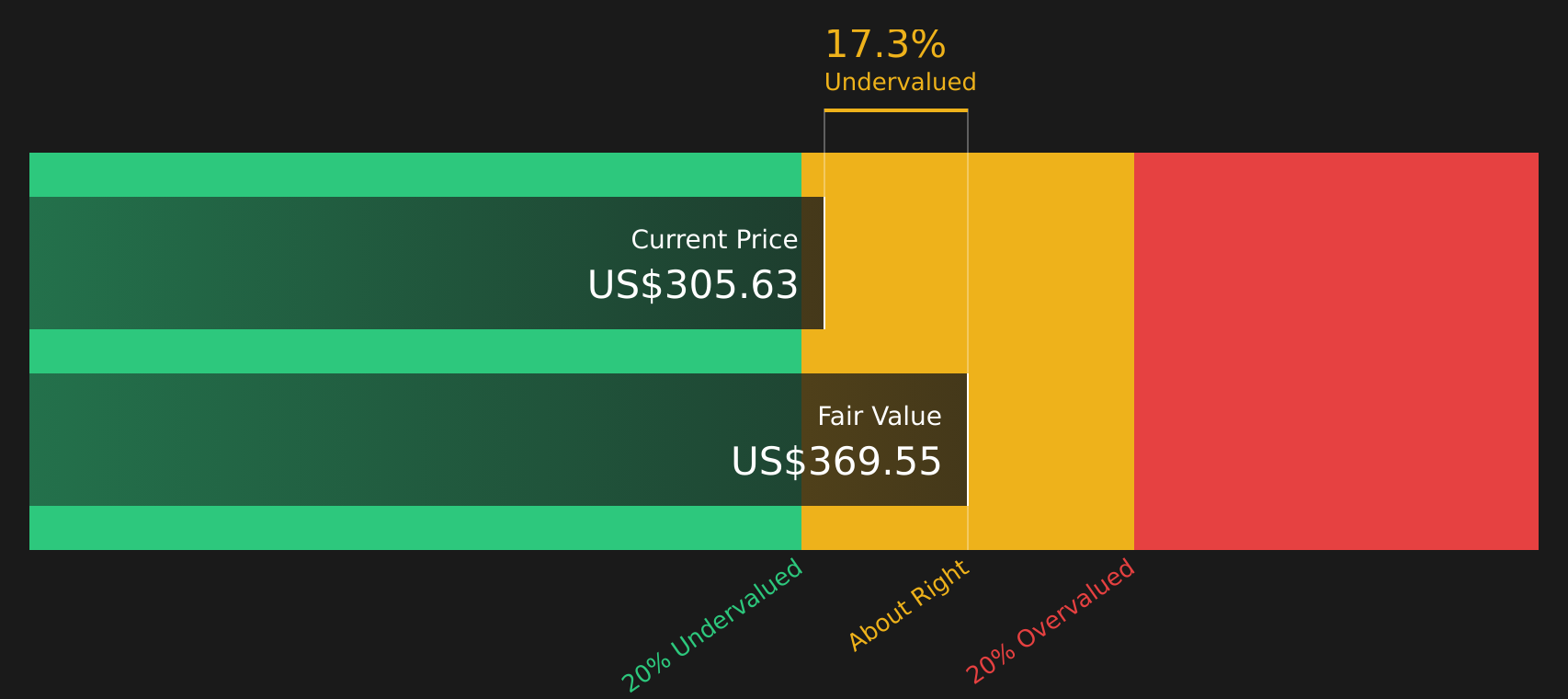

Bringing these projected cash flows back to today using a discount rate yields an estimated intrinsic value of around $339.76 per share. Compared with the recent share price of $231.31, the model suggests an intrinsic discount of about 31.9%, which points to the stock being undervalued on these cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests International Business Machines is undervalued by 31.9%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: International Business Machines Price vs Earnings

P/E is a common way to look at profitable companies because it ties what you pay directly to the earnings the business is generating today. As a rule of thumb, higher expected earnings growth and lower perceived risk can justify a higher P/E, while slower growth and higher risk tend to line up with a lower P/E being seen as normal.

International Business Machines currently trades on a P/E of 20.26x. That sits close to the broader IT industry average of 20.57x, but above the peer group average of 13.01x, so on simple comparisons the stock looks more expensive than many peers but roughly in line with the sector overall.

Simply Wall St’s Fair Ratio for International Business Machines is 30.47x. This is a proprietary estimate of what the P/E might be given factors such as the company’s earnings profile, industry, profit margins, market cap and identified risks. Because it folds these elements into a single figure, it can be more tailored than a basic peer or industry average comparison. Setting the current P/E of 20.26x against the Fair Ratio of 30.47x suggests the stock is trading below what this framework would imply.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your International Business Machines Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced. These let you attach a clear story about International Business Machines to the numbers by linking your view on its future revenue, earnings and margins to a forecast, and then to a Fair Value that can be compared with the current price on Simply Wall St's Community page. Narratives update automatically when fresh news or earnings arrive. For example, one Narrative might assume a lower Fair Value of about US$201.51 based on slower revenue growth of 3.7% a year, easing profit margins around 13.4% and earnings of US$10.3b by 2029. Another might assume a higher Fair Value of about US$390.00 built on revenue growth of 7.3% a year, margins near 17.1% and earnings of US$14.3b by 2029. This provides a clear range of stories to compare with your own expectations before deciding how the stock fits your plan.

For International Business Machines however we will make it really easy for you with previews of two leading International Business Machines Narratives:

Fair value in this narrative: about US$302.05 per share.

Implied undervaluation vs the recent US$231.31 share price: roughly 23.4%.

Revenue growth assumption: 5.18% a year.

- Analysts in this camp see hybrid cloud, AI and acquisitions such as HashiCorp supporting revenue growth, higher margins and a larger base of recurring software income.

- They factor in earnings rising to about US$10.5b by 2028, with profit margins moving higher and a future P/E of 33.7x helping to support their fair value estimate.

- Key risks they flag include macro uncertainty, pressure on consulting and software, competition in areas like virtualization, and currency moves that could affect cash flow.

Fair value in this narrative: about US$201.51 per share.

Implied overvaluation vs the recent US$231.31 share price: roughly 14.8%.

Revenue growth assumption: 3.72% a year.

- The bearish view focuses on pressure from large cloud providers, a shift toward cloud native solutions and weaker demand for traditional infrastructure weighing on revenue and margins.

- These analysts model slower growth, profit margins easing to about 13.4% and a future P/E of 25.3x, which together support their lower fair value estimate.

- They also highlight higher compliance and operating costs, pension and acquisition related debt, and the risk that legacy revenue erosion offsets progress in areas like AI and automation.

If you want to see how other investors are framing the story and where your own view sits between these poles, See what the community is saying about International Business Machines.

Do you think there's more to the story for International Business Machines? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.