Is It Time To Reassess Li Auto (LI) After A 39.9% One-Year Share Price Fall?

LI Auto LI | 0.00 |

- Wondering whether Li Auto shares offer real value at today's price, or if the risks outweigh the potential reward, starts with understanding what the current market is actually pricing in.

- The stock last closed at US$17.23, with recent returns showing a 6.6% decline over 7 days, a 4.2% gain over 30 days, and a slight 0.1% decline year to date. The 1 year return is a 39.9% loss.

- Recent headlines around Li Auto have focused on its position in the US-listed Chinese electric vehicle space and how sentiment toward that peer group affects trading in the stock. Broader news about regulatory conditions for US-listed Chinese companies has also shaped how investors are thinking about risk and required return.

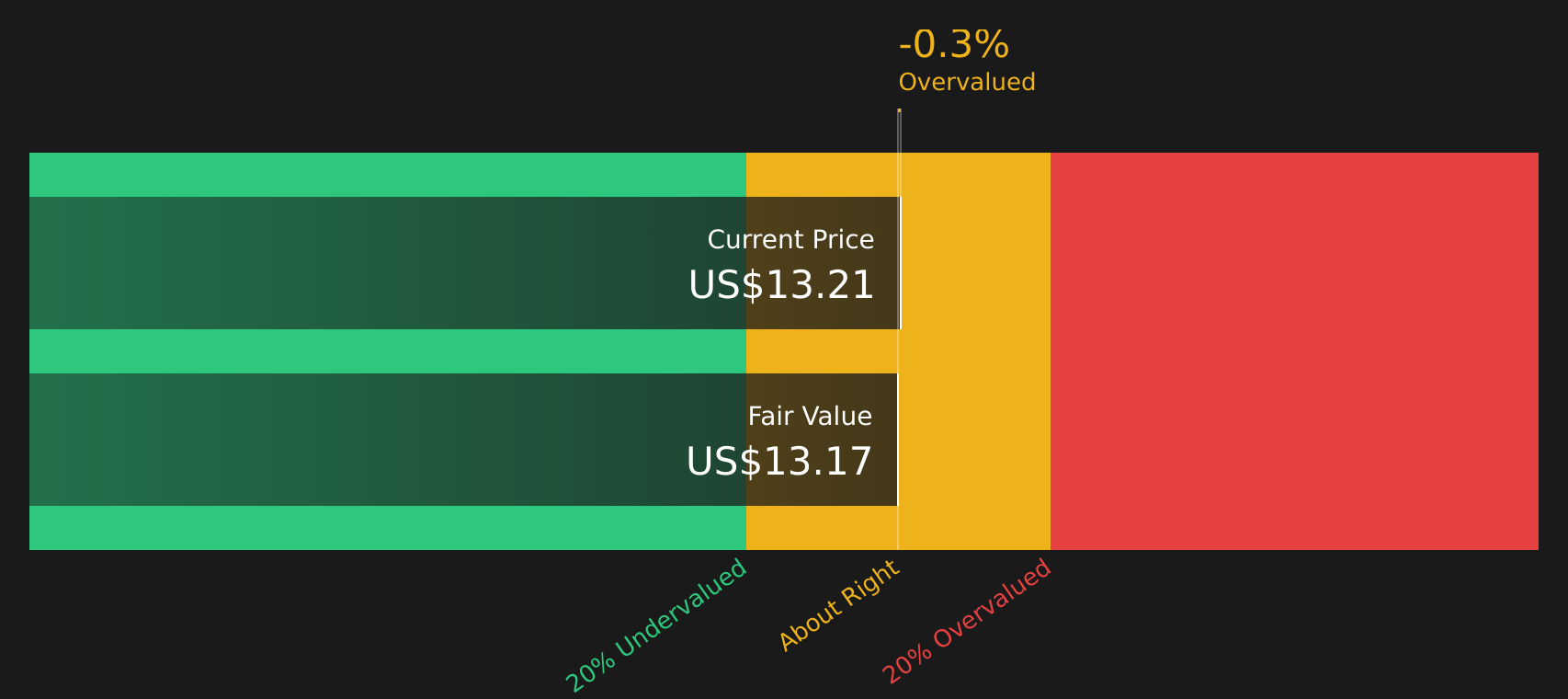

- On our checks, Li Auto scores a 3 out of 6 valuation score. This suggests some metrics point to value while others are less clear. Next we will look at the main valuation approaches investors often use before finishing with a more complete way to think about what the stock might be worth.

Approach 1: Li Auto Discounted Cash Flow (DCF) Analysis

A DCF model projects a company’s future cash flows and then discounts those projections back to today’s value, aiming to estimate what the whole business might be worth right now.

For Li Auto, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flows in CN¥. The latest twelve month free cash flow is a loss of CN¥9,532.48m, so the starting point is negative. Analysts provide cash flow estimates out to 2030, with CN¥14,363m of free cash flow projected for that year, and Simply Wall St extends the projections further using its own assumptions.

When all of these projected cash flows are discounted back and summed, the model arrives at an estimated intrinsic value of US$21.43 per share. Compared with the recent share price of US$17.23, this implies the stock trades at roughly a 19.6% discount to that estimate. On this DCF view, Li Auto appears to be trading below that estimated intrinsic value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Li Auto is undervalued by 19.6%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Li Auto Price vs Earnings

For a company that is generating earnings, the P/E ratio is often the quickest way to see what you are being asked to pay for each dollar of profit. It ties the share price directly to current earnings, which is what ultimately supports long term returns.

What counts as a normal or fair P/E ratio depends on what investors expect for future growth and how much risk they see in the business. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually calls for a lower one.

Li Auto currently trades on a P/E of 26.14x. That is above the Auto industry average P/E of 18.78x, but below the peer group average of 40.78x. Simply Wall St’s Fair Ratio for Li Auto is 31.42x, which is its own estimate of an appropriate P/E given the company’s earnings growth profile, industry, profit margins, market cap and risk factors. This Fair Ratio is more tailored than a simple comparison with peers or the broad industry, because it adjusts for Li Auto’s specific characteristics rather than assuming one size fits all.

On this basis, Li Auto’s current P/E of 26.14x versus a Fair Ratio of 31.42x suggests the shares trade below that tailored estimate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Li Auto Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce Narratives, a simple tool on Simply Wall St’s Community page that lets you set out your story for Li Auto, link that story to a clear set of revenue, earnings and margin assumptions, translate those into a Fair Value you can compare with today’s price, and then have that view automatically refresh as new news or earnings arrive. You can then see, for example, how one Li Auto Narrative might lean cautious with a Fair Value of about US$14.04 while another is far more optimistic at around US$35.43, and decide which version of the story fits how you see the company.

For Li Auto however we will make it really easy for you with previews of two leading Li Auto Narratives:

These are not predictions, they are structured "what if" views based on different analyst assumptions, so you can see what would need to be true for each story to make sense at today’s price.

Fair value in this bullish narrative: US$24.43 per share

Implied discount to this fair value at US$17.23: about 29.4% undervalued

Revenue growth assumption: 18.23% a year

- Assumes Li Auto successfully shifts from EREV models to pure BEVs, backed by models like Li MEGA, Li i8 and Li i6, which supports higher market share and a larger long term revenue base.

- Builds in meaningful upside from intelligent driving software, AI chips and a fast growing ultra fast charging network that together are expected to support margins and recurring revenue.

- Counts on continued expansion into lower tier Chinese cities and early overseas markets, with analysts using these forecasts to support a consensus price target above the recent share price, subject to your own checks.

Fair value in this cautious narrative: US$14.04 per share

Implied premium to this fair value at US$17.23: about 22.7% overvalued

Revenue growth assumption: 12.18% a year

- Focuses on risks from heavy reliance on China, possible trade barriers and tariffs, and stricter regulation that could pressure growth and margins even if deliveries remain solid.

- Builds in tougher assumptions on competition, pricing and the timing and execution of the shift from EREV to full BEV, which together limit how much value is placed on future earnings.

- Anchors closer to the more bearish analyst price targets, where the view is that the current market price asks investors to pay up for growth that may be harder to achieve than consensus implies.

Put side by side, these narratives show how different views on growth, margins, competition and overseas expansion can lead to very different estimates of fair value, even when they draw on similar data. The useful next step is to decide which set of assumptions feels closer to your own view of Li Auto, then use that as a reference point rather than relying on a single headline number.

Do you think there's more to the story for Li Auto? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.