Is It Time To Reassess ResMed (RMD) After This Year’s 25% Share Price Slide

ResMed RMD | 0.00 |

- Wondering whether ResMed at around US$182.82 is starting to look like value, or if recent weakness is signalling something else about the stock.

- The share price has retreated recently, with returns down 12.1% over the past week, 10.8% over the past month and 25.3% year to date, which may have changed how investors view its risk and potential.

- Recent coverage has focused on ResMed as a major player in medical equipment, with investors weighing the long term demand for its products against current sentiment toward the sector. This mix of company specific headlines and wider market focus on healthcare provides additional context for the share price moves you are seeing now.

- ResMed currently has a valuation score of 5 out of 6. The next step is a breakdown of how different valuation methods line up on the stock, followed by a look at a more complete way to think about its value by the end of this article.

Approach 1: ResMed Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today’s value using a required rate of return.

For ResMed, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about $1.75b, and analysts and estimates project Free Cash Flow of $1.98b by 2030. Simply Wall St provides detailed projections for each year out to 2035, starting from $1.58b in 2026, with near term figures based on analyst estimates and the later years extrapolated from those trends.

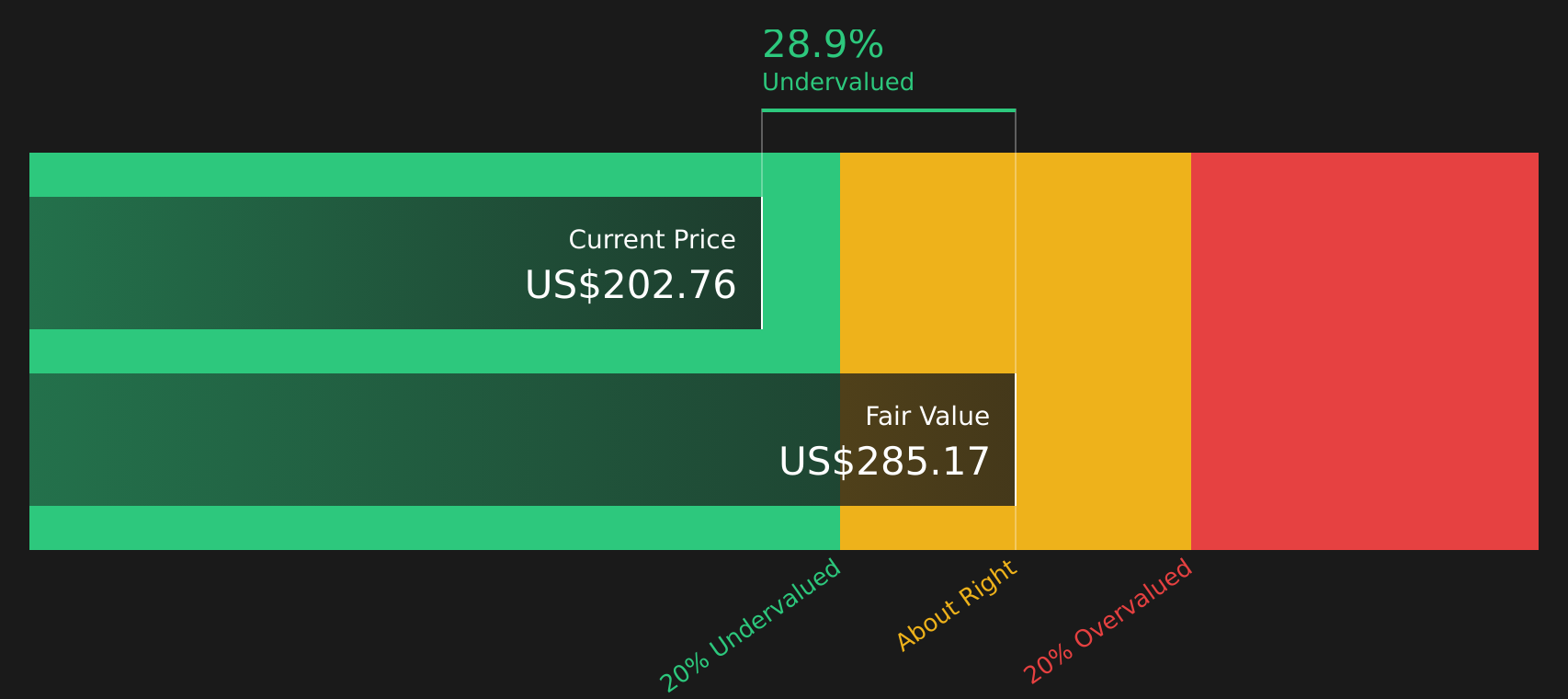

When these projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $299.04 per share. Against a current share price around $182.82, this implies ResMed is trading at roughly a 38.9% discount. On this DCF view, the stock appears to be undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ResMed is undervalued by 38.9%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: ResMed Price vs Earnings

For a profitable company like ResMed, the P/E ratio is a useful shorthand for what investors are currently willing to pay for each dollar of earnings. It ties the share price directly to actual profits, which many investors find more intuitive than cash flow models.

What counts as a “normal” P/E depends a lot on how quickly earnings are expected to grow and how risky those earnings are perceived to be. Higher growth or lower risk can justify a higher multiple, while slower growth or higher risk usually points to a lower one.

ResMed currently trades on a P/E of 17.45x, compared with a Medical Equipment industry average of about 24.23x and a peer group average of 23.89x. Simply Wall St also calculates a “Fair Ratio” of 23.34x, which is the P/E it would expect for ResMed given factors such as earnings growth, margins, industry, market cap and risk profile.

This Fair Ratio is more tailored than a simple industry or peer comparison because it adjusts for company specific characteristics instead of assuming all stocks deserve the same multiple. With the current P/E of 17.45x sitting below the Fair Ratio of 23.34x, this preferred multiple view points to the stock trading at a discount.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your ResMed Narrative

Earlier the article mentioned that there is an even better way to understand valuation, so this is where Narratives come in, giving you a simple story that links your view of ResMed to a financial forecast and then to a Fair Value that you can compare with today’s price.

A Narrative on Simply Wall St’s Community page is your chance to spell out why you think ResMed’s future revenue, earnings and margins could look a certain way, then connect those assumptions to a Fair Value estimate instead of relying only on headline multiples.

Because Narratives are updated when fresh news or earnings arrive, your story and the numbers move together and make it easier to reassess whether the stock looks attractively priced or stretched based on your own framework, not just the latest share price move.

For example, one ResMed Narrative currently anchors to a Fair Value of about US$340.00, while another sits closer to US$182.45. This shows how two investors can look at the same company, plug in different assumptions about future revenue, earnings, margins and P/E, and end up with very different views on whether the current price looks high or low.

For ResMed, however, we will make it really easy for you with previews of two leading ResMed Narratives:

Fair value in this bullish narrative: US$288.21 per share

Recent price compared with this fair value suggests the stock is about 36.6% below that narrative fair value using the latest close of US$182.82

Revenue growth assumption used in this narrative: 7.6% a year

- Focuses on broader reach in sleep and respiratory care, helped by acquisitions, digital health tools and higher awareness of sleep disorders.

- Assumes gradual improvement in profit margins and earnings as manufacturing, logistics and scale efficiencies filter through.

- Takes analyst consensus targets as a guide and uses a higher future P/E multiple, so the fair value depends on both earnings growth and a strong valuation being sustained.

Fair value in this bearish narrative: US$182.45 per share

Recent price compared with this fair value suggests the stock is about 0.2% above that narrative fair value using the latest close of US$182.82

Revenue growth assumption used in this narrative: 6.9% a year

- Frames a case where GLP 1 therapies, alternative treatments and pricing pressure could limit demand for devices and masks.

- Builds in more cautious assumptions on revenue growth, margin expansion and the future P/E multiple compared with consensus.

- Arrives at a fair value close to the current share price, which in this scenario suggests there is limited room for error in how the business and margins develop.

These two narratives sit on the same company data but apply different assumptions on growth, margins and the multiple investors might be willing to pay. This provides a practical range to compare with your own view before making any decisions.

Do you think there's more to the story for ResMed? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.