Is It Time To Reassess Ultra Clean Holdings (UCTT) After Its Sharp One Year Surge

Ultra Clean Holdings, Inc. UCTT | 0.00 |

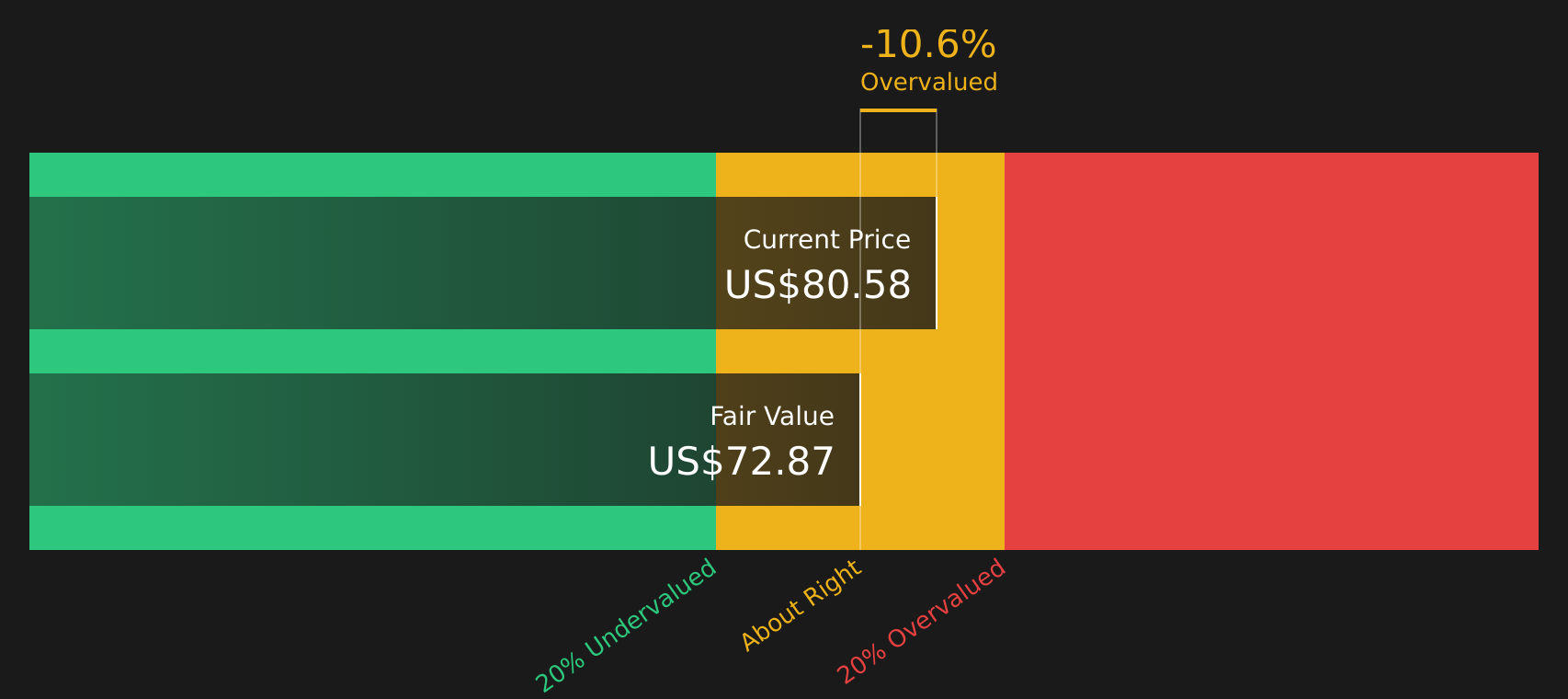

- If you are wondering whether Ultra Clean Holdings at around US$74.61 still offers value or is running ahead of itself, it helps to start with what the recent price action and fundamentals are telling you.

- The stock has moved sharply in recent periods, with a 10.1% decline over the last 7 days, a 18.1% return over 30 days, and longer term returns of 173.1% year to date and 269.9% over 1 year.

- These swings have kept attention on the stock, with investors reacting to broader semiconductor sector developments and company specific updates that shape expectations around demand, margins, and capital spending. Headlines around supply chain trends, customer ordering patterns, and technology investment cycles have all helped frame how traders and longer term holders think about risk and opportunity here.

- Ultra Clean Holdings currently holds a valuation score of 5/6. This reflects how it screens across several pricing checks. The rest of this article will walk through those methods before finishing with a broader way to think about what that score really means for you.

Approach 1: Ultra Clean Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return. The goal is to translate those future dollars into a single present value per share.

For Ultra Clean Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month free cash flow is a loss of $55.42 million, so the starting point is negative. From there, analysts and model estimates project a move to positive free cash flow, with projected free cash flow of $306.70 million by 2030. Beyond the first few years, Simply Wall St extrapolates the projections rather than relying on explicit analyst forecasts.

Combining these projected cash flows and discounting them back results in an estimated intrinsic value of about $77.66 per share. Compared with the recent share price around $74.61, the DCF output suggests the stock is roughly 3.9% undervalued, which is a modest gap rather than a dramatic one.

Result: ABOUT RIGHT

Ultra Clean Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

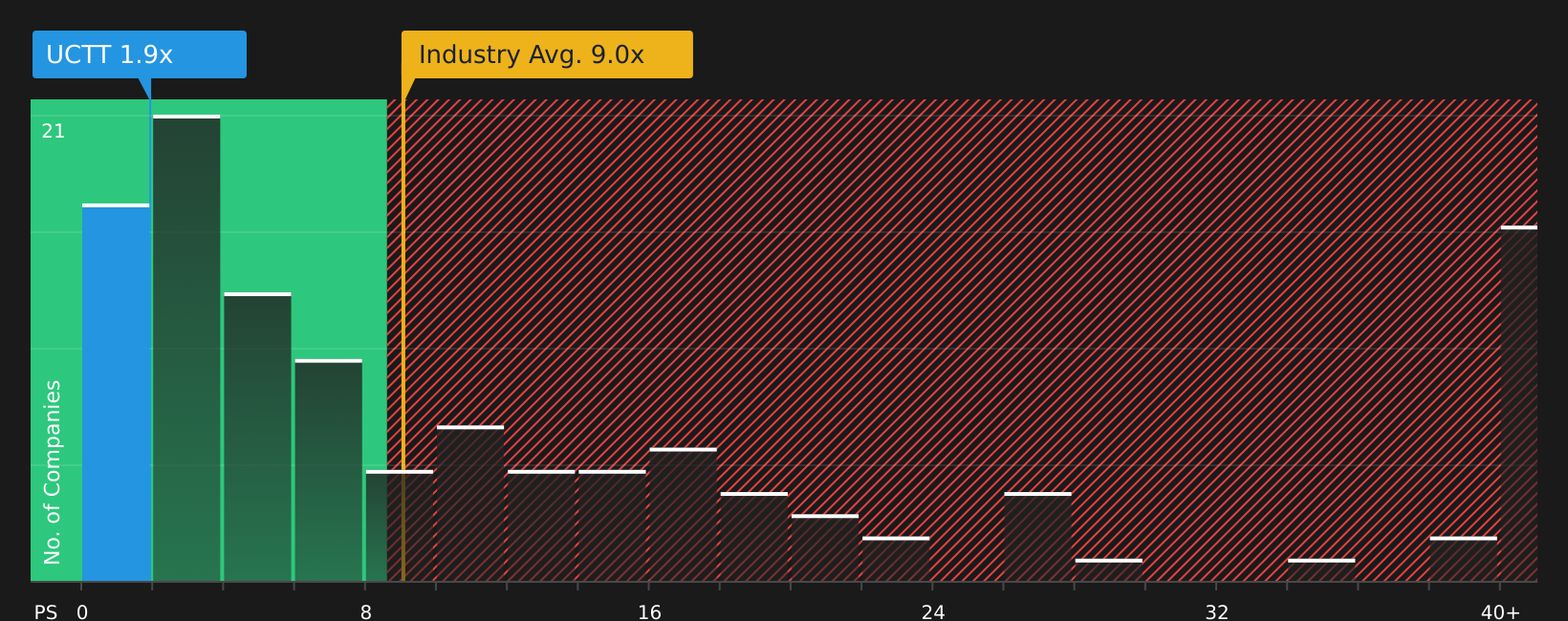

Approach 2: Ultra Clean Holdings Price vs Sales

For companies where earnings can be uneven, the P/S ratio is often a useful way to think about valuation because it focuses on revenue rather than profit, which can swing with margins and one off items. A higher or lower P/S ratio is usually linked to what investors expect for future growth and how much risk they see in the business, so there is no single “right” number that fits every stock.

Ultra Clean Holdings currently trades on a P/S ratio of 1.62x. This sits well below the Semiconductor industry average P/S of 8.11x and a peer average of 19.45x. Simply Wall St’s Fair Ratio model, which estimates what a company’s P/S “should” look like based on factors such as earnings growth, profit margins, industry, market cap and specific risks, suggests a Fair Ratio of 2.64x.

Comparing Ultra Clean Holdings only with peers or the broader industry can be misleading because those companies can have very different growth outlooks, risk profiles and margin structures. The Fair Ratio aims to adjust for those differences and offers a more tailored yardstick. With the current P/S of 1.62x versus a Fair Ratio of 2.64x, the shares screen as undervalued on this metric.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 17 top founder-led companies.

Upgrade Your Decision Making: Choose your Ultra Clean Holdings Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as simple stories that you and other investors build around Ultra Clean Holdings, linking your view of its business, future revenue, earnings and margins to a Fair Value that you can compare with the current share price to decide whether you see it as attractive or expensive.

On Simply Wall St’s Community page, Narratives are available as an easy tool used by millions of investors, connecting a company’s story to a financial forecast and then to a Fair Value that refreshes automatically when new information such as news or earnings is added.

For Ultra Clean Holdings, one investor might align with a higher Fair Value such as US$100.00 and focus on AI driven demand and the UCT 3.0 plan. Another might lean toward a lower Fair Value like US$35.00 and focus on customer concentration and margin risks. Narratives allow both views to sit side by side so you can see where your own assumptions fit on that spectrum.

For Ultra Clean Holdings, however, we will make it really easy for you with previews of two leading Ultra Clean Holdings Narratives:

Think of these as quick snapshots of what bullish and bearish analysts are building into their numbers, so you can decide which set of assumptions feels closer to your own view before you do any detailed work.

Fair Value: US$81.25

Implied undervaluation vs last close: about 8.2%

Revenue growth assumption: 12.54%

- Analysts backing this view lean on AI related capital spending, advanced fab buildouts and the UCT 3.0 plan as reasons Ultra Clean Holdings could grow into a higher valuation over time.

- They factor in revenue growing by low double digits annually, a move from a loss to positive earnings and modest margin improvement, with a relatively high future P/E multiple to support the fair value of US$81.25.

- The narrative still flags risks around customer concentration, tariff related costs and the impact of cost cutting, so it is not a one sided story and assumes these issues remain manageable.

Fair Value: US$35.00

Implied overvaluation vs last close: about 53.0%

Revenue growth assumption: 11.50%

- The more cautious group of analysts focuses on qualification delays, inventory overhang at customers and execution risk around automation and a more complex manufacturing footprint.

- They still assume revenue and earnings increase over time, but pair that with a much lower fair value of US$35.00 and a future P/E that sits below the wider US Semiconductor industry multiple.

- This camp highlights that even with expected business improvement, current pricing could be rich if AI demand, wafer fab equipment spending and China growth do not line up with the more optimistic scenarios.

If you want to see how these two storylines are built line by line, and where your own expectations sit in between them, it can help to read the full narratives side by side and stress test the assumptions that matter most to you.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Ultra Clean Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Ultra Clean Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.