Is It Time To Reconsider Block (SQ) After A 40% One Year Share Price Gain?

Block, Inc. Class A XYZ | 0.00 |

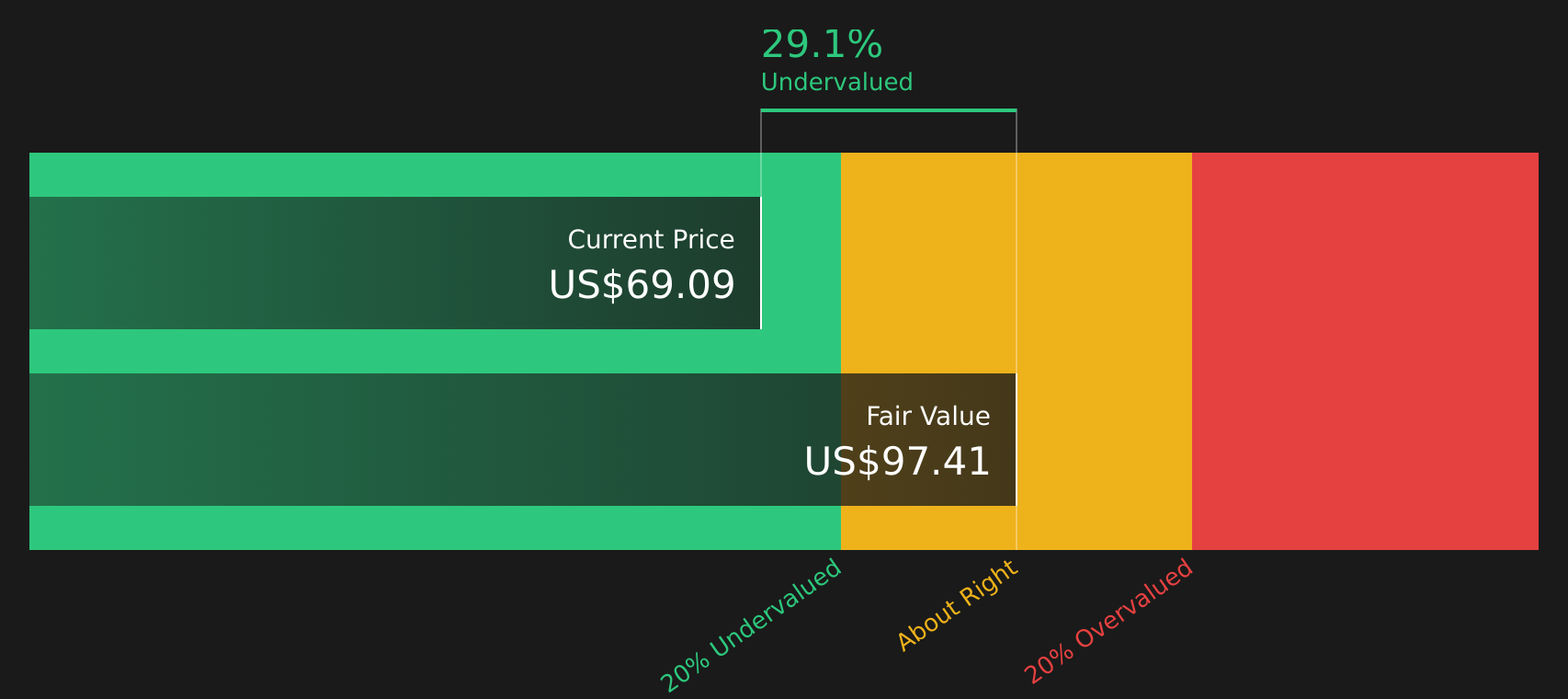

- If you are trying to figure out whether Block at around US$70 a share offers reasonable value, the key question is what you are actually paying for in terms of fundamentals and future expectations.

- The stock is roughly flat over the last 7 days with a 0.5% decline, but it has returned 17.0% over the last 30 days, 7.7% year to date and 40.0% over the last year, all against a longer 5 year return of 64.4% decline and a 3 year return of 22.4%.

- Recent headlines around Block have focused on its role in diversified financial services and ongoing attention to its core platforms. This continues to keep the stock in the spotlight for both growth focused and risk conscious investors. This news flow helps explain why sentiment can shift quickly, feeding into short term price swings even as longer term questions about business quality and sustainability remain central.

- Block currently has a valuation score of 2/6, which means it screens as undervalued on 2 of 6 key checks. The next sections will compare different valuation methods and then finish with a broader way to think about value that goes beyond any single model.

Block scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Block Excess Returns Analysis

The Excess Returns model looks at how much value Block creates on top of the return that shareholders are assumed to require. Instead of focusing on near term earnings headlines, it asks whether the company’s return on equity justifies its current share price.

For Block, the key inputs are:

- Book Value: $36.88 per share

- Stable EPS: $5.20 per share (source, weighted future Return on Equity estimates from 9 analysts)

- Cost of Equity: $3.51 per share

- Excess Return: $1.69 per share

- Average Return on Equity: 11.28%

- Stable Book Value: $46.09 per share (source, weighted future Book Value estimates from 7 analysts)

The model compares the earnings power implied by that 11.28% Return on Equity with the required $3.51 per share cost of equity. It then capitalizes the excess $1.69 per share to estimate what the stock could be worth today.

On this basis, the Excess Returns valuation points to an intrinsic value of about $87.67 a share, which indicates that Block trades at roughly a 20.0% discount to this estimate.

Result: UNDERVALUED

Our Excess Returns analysis suggests Block is undervalued by 20.0%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Block Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it ties the share price directly to the earnings that support it. When you pay a certain P/E, you are effectively deciding how many years of current earnings you are willing to pay for upfront.

What counts as a “normal” P/E depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth or more predictable earnings can justify a higher P/E. In contrast, slower growth or higher uncertainty usually points to a lower multiple.

Block currently trades on a P/E of 31.97x. This sits above the Diversified Financial industry average of 18.50x and above the peer average of 25.09x. On a simple comparison, this makes the stock look more expensive than many alternatives.

Simply Wall St’s Fair Ratio framework goes a step further. It estimates what a reasonable P/E might be based on factors such as earnings growth, profit margins, industry, market cap and key risks, rather than relying purely on peer or industry comparisons. For Block, the Fair Ratio is 23.30x, which is below the current 31.97x. On this metric, the stock screens as overvalued.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Block Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St bring this to life by letting you attach a clear story about Block to your own assumptions on future revenue, earnings, margins and fair value. You can then constantly refresh that view as new news or earnings arrive, compare your fair value to the current price and decide whether the stock looks attractive or stretched. For example, one Block Narrative on the Community page currently anchors on a fair value of about US$60.88 with more modest revenue growth and an 8.4% profit margin outlook. Another assumes stronger growth with margins above 11% and a fair value near US$111.26. By choosing the story that best matches your expectations, you turn scattered data into a simple, reusable decision tool.

For Block, we will make it really easy for you with previews of two leading Block Narratives:

Fair value in this bullish narrative: US$85.52 per share.

Implied undervaluation vs the recent US$70.14 share price, using that fair value, is about 18.0%.

Revenue growth assumption in this narrative: 10.77% a year.

- Focuses on AI driven efficiency plans and workforce reductions that analysts link to higher long term profitability and slightly higher fair value estimates.

- Emphasizes growing product velocity across Cash App and Square, with international and upmarket expansion broadening Block's addressable market.

- Highlights a modestly higher long run profit margin and revenue growth outlook, while also assuming a lower future P/E multiple as sentiment around payment stocks adjusts.

Fair value in this bearish narrative: US$60.88 per share.

Implied overvaluation vs the recent US$70.14 share price, using that fair value, is about 13.2%.

Revenue growth assumption in this narrative: 8.24% a year.

- Argues that rising regulatory burdens, cyber risk, and dependence on cryptocurrency activity could keep costs elevated and earnings more volatile.

- Flags pressure from competition and government backed payment systems, with the potential for lower transaction fees and squeezed margins over time.

- Frames AI driven workforce cuts and sector wide multiple compression as sources of execution risk and as reasons why a lower future P/E could be warranted.

Together, these two narratives bracket a fair value range from about US$60.88 to US$85.52 around the current price. This provides a clear starting point to consider which assumptions feel closer to how you see Block's future.

Do you think there's more to the story for Block? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.