Is It Time To Reconsider Pfizer (PFE) After Recent Share Price Rebound?

Pfizer Inc. PFE | 0.00 |

- If you are wondering whether Pfizer at a last close of US$26.53 still offers solid value, the starting point is understanding what that price really implies about the business.

- Over the last year the stock returned 24.9%, with a 5.4% gain year to date, a 1.0% rise over the past week, and a 4.7% decline across the last 30 days, which signals that expectations and perceived risk have been shifting recently.

- Recent headlines have focused on Pfizer's efforts to reshape its portfolio and pipeline, alongside ongoing attention on its position in key therapeutic areas. These developments help explain why sentiment has not moved in a straight line, even as the stock has logged mixed returns across different time frames.

- On Simply Wall St's six point valuation check, Pfizer scores 4 out of 6, suggesting some measures flag the stock as undervalued while others are more neutral. The next sections will unpack these methods before turning to an even more rounded way to think about valuation at the end of the article.

Approach 1: Pfizer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the cash it may generate in the future and then discounting those cash flows back to today.

For Pfizer, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about US$8.94b. Analyst estimates and subsequent extrapolations suggest projected Free Cash Flow of around US$16.03b in 2030, with a full set of ten year projections stepping up toward that level and then moderating in the outer years, as shown in the discounted figures provided.

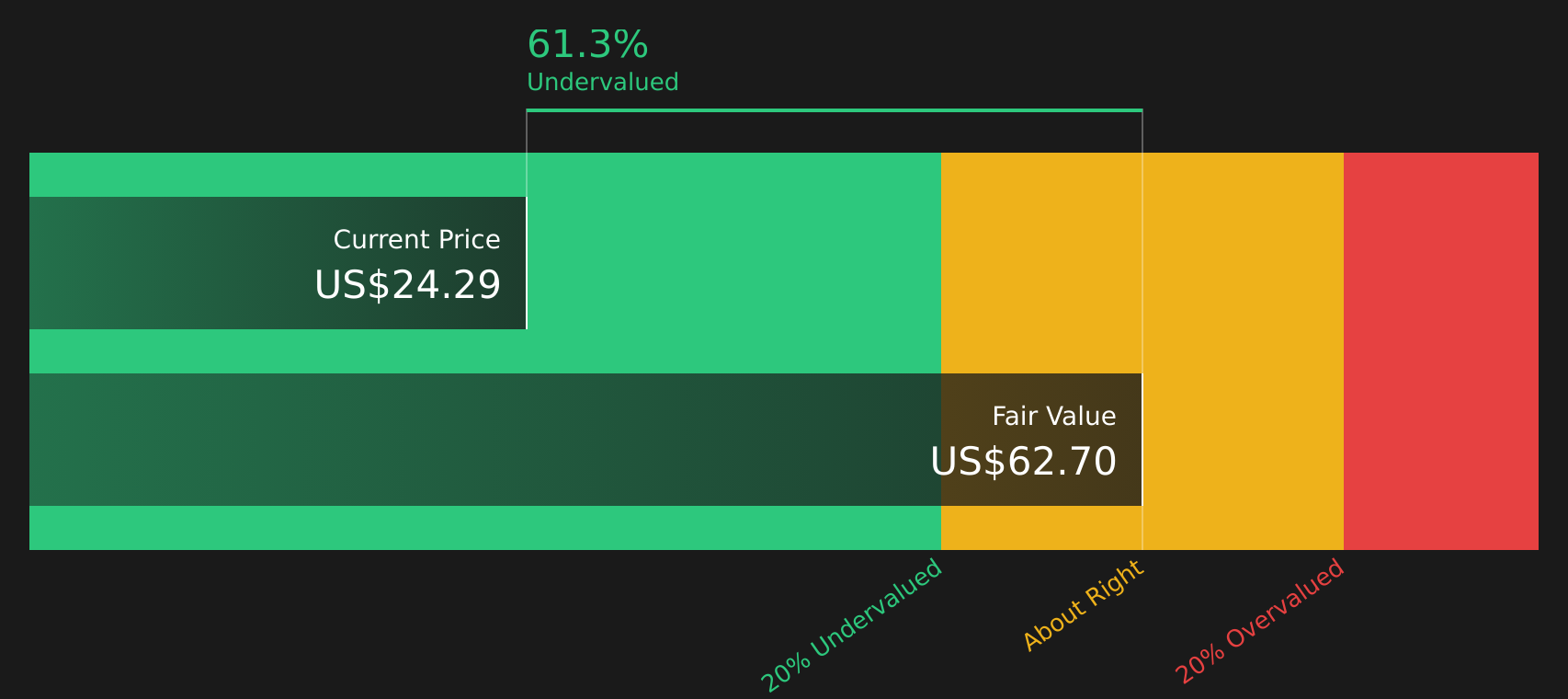

Bringing all of those future cash flows back to today, the DCF model arrives at an estimated intrinsic value of US$62.52 per share. Compared with the recent share price of US$26.53, this implies the stock is about 57.6% undervalued on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pfizer is undervalued by 57.6%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Approach 2: Pfizer Price vs Earnings

For a profitable company like Pfizer, the P/E ratio is a useful shorthand for how much investors are currently paying for each dollar of earnings. A higher or lower P/E often reflects what the market is factoring in around earnings growth potential and risk, so what counts as a “normal” or “fair” P/E varies across industries and companies.

Pfizer trades on a P/E of 20.22x. That sits above the Pharmaceuticals industry average of 16.85x, but below the peer group average of 22.95x. On the surface, that suggests the stock is priced higher than the wider industry, yet not as highly as some peers.

Simply Wall St’s Fair Ratio for Pfizer is 20.46x. This is a proprietary estimate of the P/E that might be expected given factors such as Pfizer’s earnings growth profile, profit margins, industry, market cap and company specific risks. Because it pulls these elements together in one number, the Fair Ratio can be more informative than a simple comparison against peers or the broad industry.

With a current P/E of 20.22x versus a Fair Ratio of 20.46x, Pfizer’s valuation on this measure looks about in line with what those fundamentals imply.

Result: ABOUT RIGHT

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Pfizer Narrative

Earlier it was mentioned that there is an even better way to understand valuation, and on Simply Wall St this shows up as Narratives, where you set out your story for Pfizer, link it to explicit assumptions about future revenue, earnings and margins, and arrive at your own Fair Value that you can compare to the current share price.

Each Narrative on the Community page is a concise story plus a forecast. You can see, for example, one investor arguing that Pfizer's transition and oncology focus support a Fair Value of about US$36, while another focuses on patent cliffs and pricing pressure and lands closer to US$24. The platform converts those views into cash flow paths, margins, P/E assumptions and a Fair Value that sits right next to the live market price.

Because these Narratives sit on Simply Wall St's platform used by millions of investors and update as new earnings, news and guidance figures are added, you can quickly see whether your preferred Pfizer story still holds up, whether the gap between Fair Value and price has widened or narrowed, and whether that story suggests it is time to wait, add, or trim based on your own plan and risk tolerance.

For Pfizer, however, we will make it really easy for you with previews of two leading Pfizer Narratives:

These sit at opposite ends of the current debate. Together they give you a clear sense of what different investors think needs to happen for the stock to look attractive or stretched at today’s price of US$26.53.

Fair value in this bullish narrative: US$29.08 per share.

Implied discount to that fair value at US$26.53: about 8.8% undervalued.

Analyst revenue outlook used in this view: 2.93% annual decline.

- Focuses on obesity, oncology and other higher margin therapies, with analysts expecting these areas plus business development to support earnings even as some products face patent expiry.

- Builds in revenue declining by 2.2% a year over the next 3 years, but margins improving from 16.8% to 21.5% and earnings moving from US$10.7b to US$12.8b by around 2028.

- Assumes the stock trades on a P/E of 15.7x those 2028 earnings, which is below the current US Pharmaceuticals industry P/E of 19.0x, and discounts everything back at about 6.8%.

Fair value in this bearish narrative: US$24.00 per share.

Implied premium to that fair value at US$26.53: about 10.5% overvalued.

Analyst revenue outlook used in this view: 7.84% annual decline.

- Centres on drug pricing pressure, patent expiries on products like Eliquis and Ibrance by 2027, and regulatory reforms that squeeze revenue and margin in key markets.

- Assumes revenue declines by 7.8% a year over the next 3 years, with earnings slipping from US$7.7b to US$6.7b by about 2029, even though margins edge up from 12.4% to 13.6%.

- Requires a higher 25.1x P/E on those 2029 earnings, above the current US Pharmaceuticals industry P/E of 17.0x, and uses a discount rate of about 7.0% to arrive at a Fair Value of US$24.00.

Taken together, these Narratives frame the current spread of expectations around Pfizer, from optimism on an obesity and oncology led reset to concern that pricing pressure and the patent cliff will weigh on revenue for longer.

If you want to see how other investors are joining that debate and what assumptions they are using around growth, margins and valuation, it is worth reading the full range of Pfizer Narratives on Simply Wall St, then testing which story lines up most closely with your own view of the stock.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Pfizer on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Pfizer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.