Is It Time To Reconsider Procter & Gamble (PG) After The Slide From US$175 To US$140?

Procter & Gamble Company PG | 0.00 |

- If you are wondering whether Procter & Gamble stock at around US$146 is offering fair value or a margin of safety right now, this article breaks down what the current price may be implying.

- The stock closed at US$146.06, with a 0.7% decline over the last 7 days, a 3.4% gain over 30 days, a 3.0% gain year to date, a 5.3% decline over 1 year, a 2.3% gain over 3 years, and a 20.4% gain over 5 years. Together, these figures give you a mixed picture of recent returns.

- Recent coverage has focused on Procter & Gamble's position as a major household products company, as investors watch how demand for everyday consumer products holds up across different market conditions. This backdrop helps explain why the stock has seen both shorter term pullbacks and longer multi year gains as sentiment around consumer staples shifts.

- Procter & Gamble currently has a valuation score of 4 out of 6. The rest of this article will walk through what that means using several common valuation approaches, then finish with a broader way to think about what “fair value” really means for this stock.

Approach 1: Procter & Gamble Discounted Cash Flow (DCF) Analysis

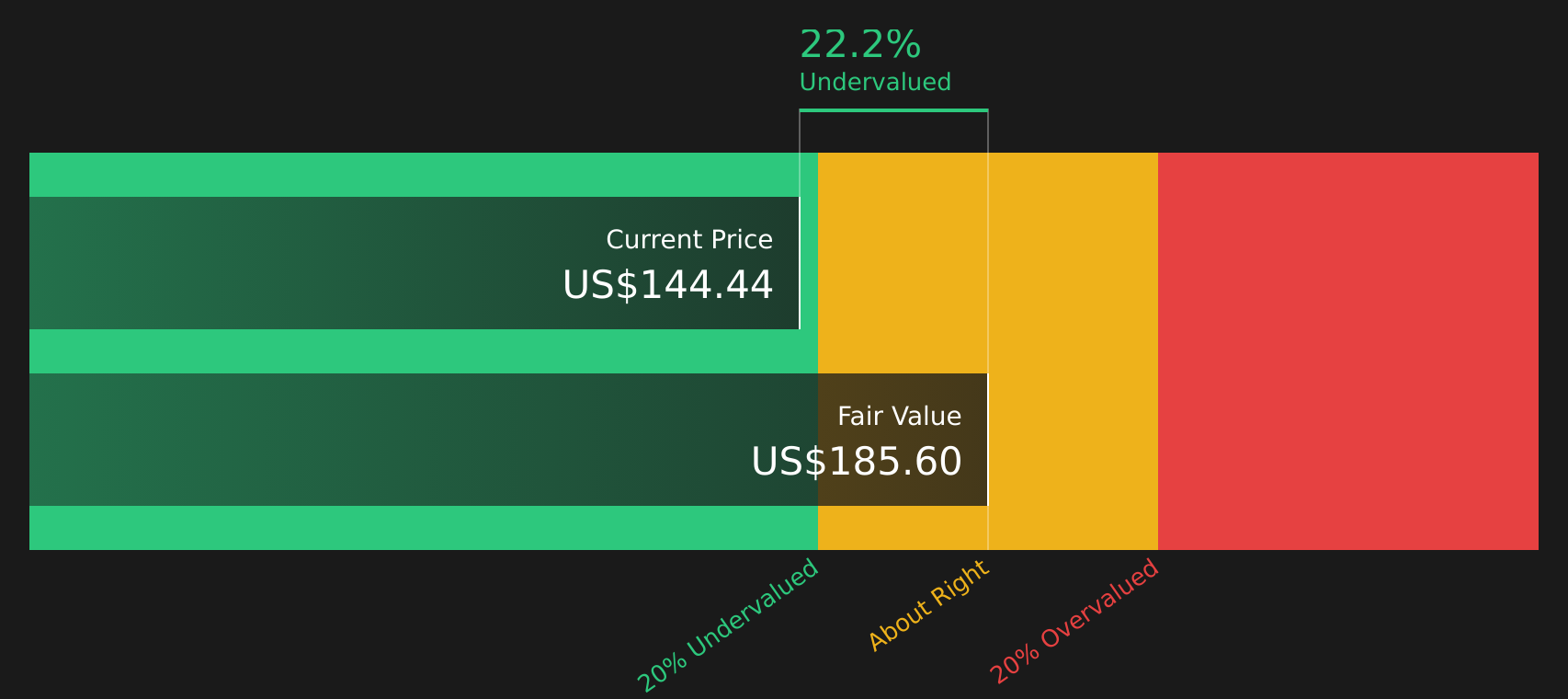

A Discounted Cash Flow, or DCF, model takes the cash that a company is expected to generate in the future and discounts those amounts back to what they might be worth in today’s dollars. It is a way of asking what the current share price implies about all those future cash flows.

For Procter & Gamble, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $15.6b. Analyst estimates and subsequent extrapolations then project free cash flow out over the next decade, reaching about $21.1b by 2035, with interim projections such as $14.8b in 2026 and $16.7b in 2028, all expressed in dollar terms.

When these projected cash flows are discounted back, the model estimates an intrinsic value of about $185.60 per share. Compared with the recent share price of around $146, this implies the DCF model suggests the stock is about 21.3% undervalued on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Procter & Gamble is undervalued by 21.3%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Procter & Gamble Price vs Earnings

For profitable companies like Procter & Gamble, the P/E ratio is a common way to see what investors are currently willing to pay for each dollar of earnings. It gives you a quick sense of how the market is pricing the stock relative to its profits.

What counts as a “normal” P/E depends on what investors expect for future growth and how much risk they see. Higher expected growth and lower perceived risk can justify a higher P/E, while lower growth or higher risk usually point to a lower P/E.

Procter & Gamble currently trades on a P/E of about 20.8x. That sits above the Household Products industry average of about 18.0x, but below the peer group average of about 24.4x. Simply Wall St’s Fair Ratio for Procter & Gamble is 24.3x. This is a proprietary estimate of what the P/E could be given factors such as earnings growth profile, profit margins, industry, market cap and risk characteristics.

Because the Fair Ratio blends these company specific factors, it can provide a more tailored benchmark than a simple comparison with peers or the broad industry. With the current P/E of 20.8x below the Fair Ratio of 24.3x, this framework suggests the stock screens as undervalued on earnings.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Procter & Gamble Narrative

Earlier it was mentioned that there is an even better way to think about valuation. Narratives are introduced here as your way of attaching a clear story about Procter & Gamble to the numbers, linking your view on its future revenue, earnings and margins to a financial forecast, a fair value, and then to a simple comparison between that fair value and today’s price on Simply Wall St’s Community page. Narratives are updated automatically when new news or earnings arrive. One investor might build a Procter & Gamble Narrative around long term wellness themes like brain health and assign a fair value near US$185 based on higher optimism. Another might focus on more cautious assumptions around growth, margins and cost of capital and land closer to US$121. Both can then use their chosen Narrative to decide whether the current share price looks high or low relative to their own story.

For Procter & Gamble however we'll make it really easy for you with previews of two leading Procter & Gamble Narratives:

Each one takes the same company data and current share price and reaches a different conclusion about fair value. Your job as an investor is to decide which story is closer to how you see the business, then judge whether today’s price around US$146.06 lines up with that view.

Fair value in this bullish narrative: US$150.00 per share

Implied discount to this fair value: about 2.6% undervalued versus the last close

Revenue growth assumption used in the narrative: 8.09%

- Views the recent slide from around US$175 to roughly US$140 as pushing the stock into potentially oversold territory, with Simply Wall St’s own fair value estimate at about US$185.05 and the narrative author’s fair value closer to US$150.

- Highlights the breadth of Procter & Gamble’s consumer staples portfolio, with brands like Pampers, Gillette, Pantene and Oral B, and points to gross margins around 50% and net margins near 18% to 19% as signs of a resilient and profitable business.

- Flags insider selling and a debt to equity ratio around 67% as factors to watch, while still viewing the stock as one to keep on a watchlist and monitor for signs such as a stabilising share price or insiders turning into net buyers.

Fair value in this cautious narrative: US$121.06 per share

Implied premium to this fair value: about 20.6% overvalued versus the last close

Revenue growth assumption used in the narrative: 3.32%

- Sees Procter & Gamble as a high quality business with an operating margin projected at 25.16%, a 5 year ROIC of 17.20% and an Aa3 Moody’s rating, but with relatively modest projected 5 year growth in revenue, EPS and dividends.

- Blends several valuation tools, including dividend discount models, DCF, historical P/E, P/CF, EV/EBITDA, P/B and P/S, along with Monte Carlo simulations, and concludes that many scenarios point to the current share price being above fair value.

- Assigns a high confidence rating to the company’s wide moat and low uncertainty, yet still lands on a fair value estimate of US$121.06 per share, which frames the stock as pricing in a premium relative to those assumptions.

Bringing these together, two of the four active Community Narratives lean undervalued and two lean overvalued, which matches the mixed signals you have already seen from the DCF and P/E work earlier in this article. Rather than hunting for a single “correct” answer, focus on which narrative assumptions about growth, margins, capital allocation and risk feel more realistic to you at today’s price.

Once you are clear on that, you can use Procter & Gamble as a live case study for building and refining your own valuation story over time, updating it as new earnings, insider activity and balance sheet data come through.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Procter & Gamble on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Procter & Gamble? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.