Is It Time To Reconsider Super Micro Computer (SMCI) After Sharp Recent Price Swings?

Super Micro Computer, Inc. SMCI | 0.00 |

- Wondering whether Super Micro Computer's current share price reflects its true worth, especially after a strong multi year run? This article focuses squarely on what the valuation signals are telling you today.

- The stock has seen sharp moves recently, with returns of 23.4% over the past week, 51.6% over the past month and 33.4% year to date, while the 1 year return sits at 0.4% and the 3 year return is 78.8%.

- Recent coverage around Super Micro Computer has focused on its role in high performance computing and AI focused server hardware, along with the scale of interest from large customers and partners. That context helps explain why the share price has been so sensitive to headlines about demand for computing capacity and broader sentiment toward AI related spending.

- Simply Wall St currently shows Super Micro Computer with a valuation score of 3 out of 6. The next sections will compare what different valuation methods suggest, and finish with a way to look beyond the models to understand what might really matter for the stock's value.

Approach 1: Super Micro Computer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projected future cash flows and discounts them back to today, aiming to estimate what those future dollars are worth right now.

For Super Micro Computer, the latest twelve month free cash flow is a loss of $6,890.86m. Analysts provide detailed free cash flow estimates for the next few years, and Simply Wall St extends those out using its 2 Stage Free Cash Flow to Equity model. By 2029, free cash flow is projected at $980.08m, with later years extrapolated through 2035 using progressively lower growth rates.

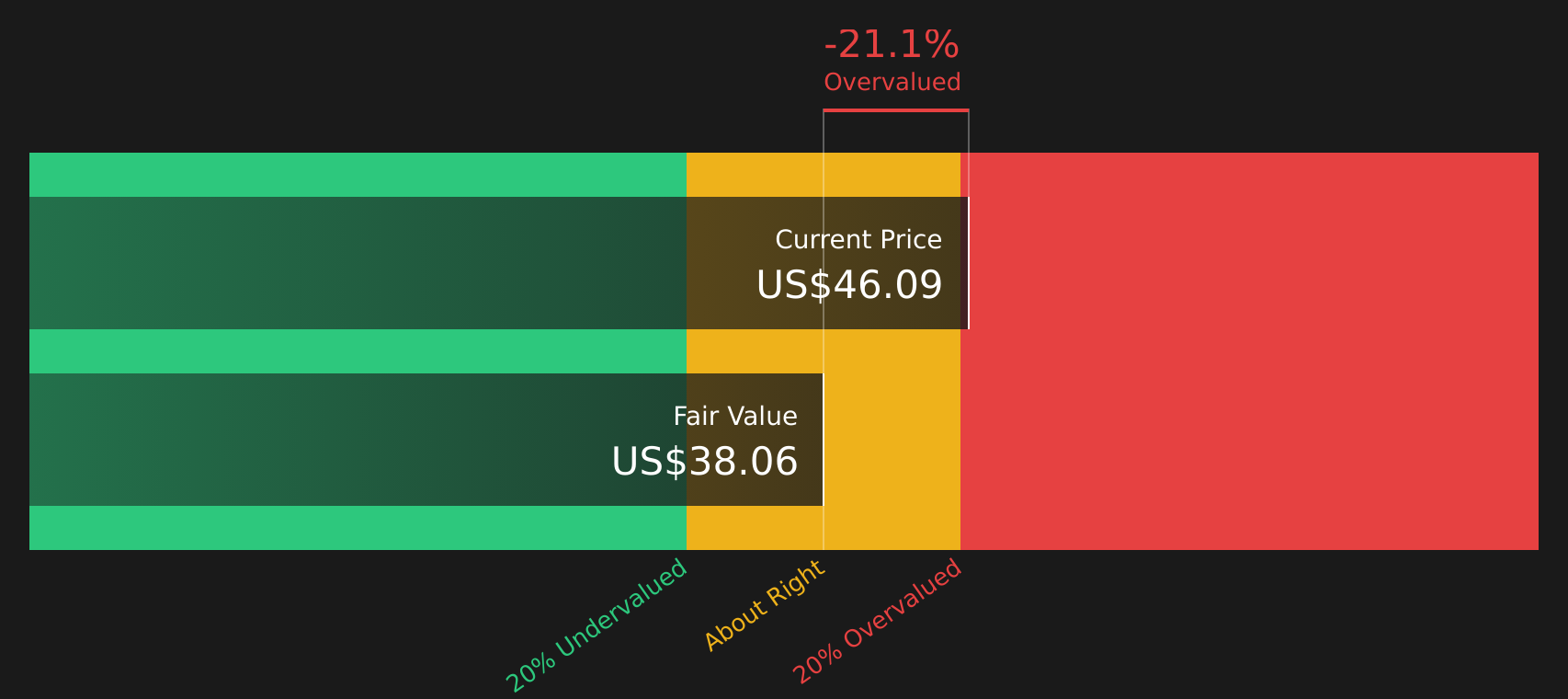

When all those projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of $36.40 per share. Compared with the current share price, this DCF output suggests the stock is about 13.5% overvalued right now.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Super Micro Computer may be overvalued by 13.5%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Super Micro Computer Price vs Earnings

For a profitable company, the P/E ratio is a useful shorthand for how much you are paying for each dollar of earnings. It ties directly to what the business earns today, which many investors find easier to relate to than multi year cash flow forecasts.

What counts as a reasonable P/E depends a lot on how fast earnings are expected to grow and how risky those earnings might be. Higher growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk often goes with a lower one.

Super Micro Computer currently trades on a P/E of 19.9x. That sits below the Tech industry average P/E of 23.9x and well below the peer average of 56.1x. Simply Wall St also provides a proprietary “Fair Ratio” for Super Micro Computer of 50.5x, which reflects factors such as earnings growth, profit margin, industry, market cap and risk profile.

This Fair Ratio aims to be more tailored than a simple peer or industry comparison because it adjusts for company specific traits rather than assuming all Tech stocks should trade on similar multiples. Set against the current P/E of 19.9x, the Fair Ratio of 50.5x indicates that, on this measure, the stock appears undervalued relative to that ratio.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Super Micro Computer Narrative

Earlier the article mentioned that there is an even better way to understand valuation, so this is where Narratives come in, giving you a way to attach a clear story about Super Micro Computer to the numbers behind your own fair value, revenue, earnings and margin assumptions.

A Narrative is simply your view on what the company is and where it is heading, written out as a short story that is then linked directly to a forecast model so that your expectations about AI server demand, customer concentration, governance risk or margin recovery flow through into a fair value per share.

On Simply Wall St, Narratives sit inside the Community page and are designed to be easy to use. You can compare your fair value to the current price and quickly see whether your story suggests the stock is above or below what you think it is worth, without needing to build Excel models.

These Narratives update automatically when new data like earnings, guidance changes, legal developments or major product news is added. This helps your story and fair value stay aligned with fresh information rather than going stale between results.

For Super Micro Computer, one Narrative might look like the lower fair value range around US$16.15, focusing on legal and credibility risks plus customer concentration. Another could sit nearer the higher fair value cluster around US$55.14 that leans into AI infrastructure demand and global DCBBS adoption. Comparing these helps you decide which story you agree with before you act.

For Super Micro Computer however we will make it really easy for you with previews of two leading Super Micro Computer Narratives:

Fair value in this narrative: US$74.53 per share

Implied discount to this fair value compared with the last close of US$41.30: about 45% below the narrative fair value

Revenue growth assumption used: 50%

- Leans on management guidance that points to US$23b to US$25b in 2025 revenue and confidence about reaching US$40b in 2026, helped by Direct Liquid Cooling being adopted across a meaningful share of new data center builds.

- Highlights the appointment of a new auditor and a special committee after short seller allegations, with the view that updated filings can help rebuild confidence after sharp share price swings.

- Frames Super Micro Computer as a key AI infrastructure provider with relationships across major chip partners, using a 50% revenue growth rate, a 6.64% net margin and a 20x forward P/E to reach fair value estimates well above the current share price.

Fair value in this narrative: US$33.20 per share

Implied premium to this fair value compared with the last close of US$41.30: about 24% above the narrative fair value

Revenue growth assumption used: 27.96%

- Builds on analyst models that tie Super Micro Computer to strong AI and analytics demand, but still land on a lower fair value as they factor in execution risk, customer concentration and hardware commoditization.

- Spells out risks around reliance on a small group of large customers, elongated order cycles around new GPU launches and potential margin pressure from price competition and global supply chain complexity.

- Arrives at a US$33.20 consensus target based on revenue of US$58.8b, earnings of US$2.2b, a P/E of 11.7x and a 9.16% discount rate, and encourages you to test those inputs against your own expectations for growth, margins and risk.

Do you think there's more to the story for Super Micro Computer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.