Is It Too Late To Consider Apellis Pharmaceuticals (APLS) After Its 130% One Year Surge?

Apellis Pharmaceuticals, Inc. APLS | 0.00 |

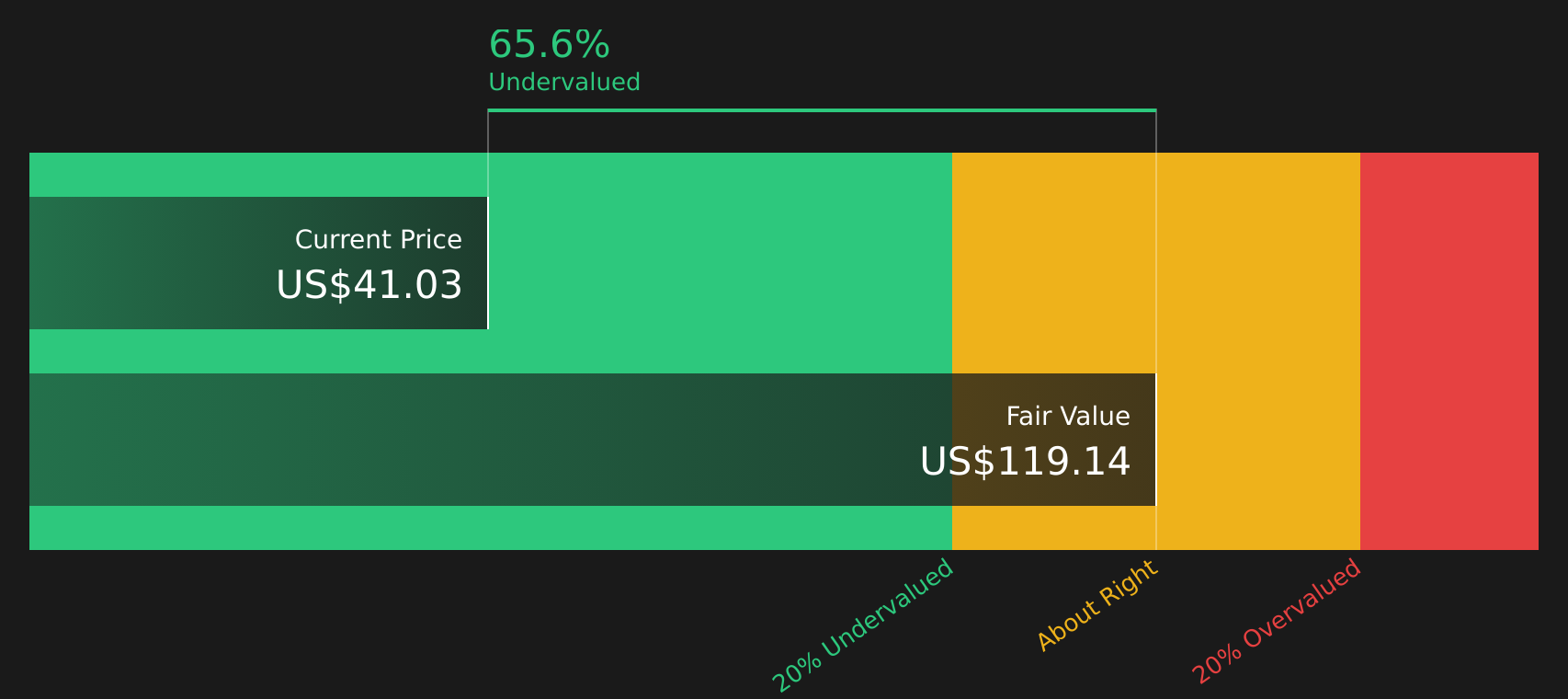

- If you are trying to figure out whether Apellis Pharmaceuticals is attractively priced today, it helps to start with how the current market value lines up against different ways of estimating fair value.

- The stock last closed at US$41.01, with returns of 0.1% over 7 days, 0.8% over 30 days, 58.6% year to date and 130.3% over the past year, alongside 3 year and 5 year returns of 53.7% decline and 10.1% decline respectively. This gives a mixed picture for anyone thinking about entry or exit points.

- Recent headlines around Apellis have focused on its product pipeline and regulatory progress, which help frame why the market might be reassessing the stock. These news items give important context for both the strong 1 year return and the weaker multi year record.

- On Simply Wall St’s 6 point valuation checklist, Apellis scores a 2 out of 6 valuation score. The next sections will walk through how different valuation methods interpret that score and then finish with a way to tie all those valuation signals into a clearer long term view of the stock.

Apellis Pharmaceuticals scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Apellis Pharmaceuticals Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and then discounting them back to today using a required rate of return.

For Apellis Pharmaceuticals, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s last twelve months Free Cash Flow is about $37.21 million. Analyst estimates and subsequent extrapolations point to projected Free Cash Flow of $345.03 million in 2030, with interim years ranging from about $38.07 million in 2026 to $863.89 million in 2035, all in dollar terms.

After discounting those projected cash flows, the model arrives at an estimated intrinsic value of $111.61 per share. Compared with the recent share price of $41.01, the DCF output implies the stock is 63.3% undervalued on this set of assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Apellis Pharmaceuticals is undervalued by 63.3%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Apellis Pharmaceuticals Price vs Earnings

For a profitable company, the P/E ratio is a useful shortcut because it links what you pay for each share to the earnings that support that share. Investors usually accept a higher P/E when they expect stronger earnings growth or see lower risk, and a lower P/E when they expect slower growth or higher risk. So, what counts as a “normal” P/E is closely tied to those expectations.

Apellis currently trades on a P/E of 39.39x, compared with the Biotechs industry average of 17.75x and a peer group average P/E of 10.91x. Simply Wall St’s Fair Ratio for Apellis is 35.95x, which is its proprietary estimate of what the P/E could be given Apellis’ earnings growth profile, industry, profit margins, market cap and risk characteristics.

This Fair Ratio is more tailored than a simple peer or industry comparison because it adjusts for company specific factors instead of assuming all biotechs deserve the same multiple. Setting Apellis’ current P/E of 39.39x against the Fair Ratio of 35.95x indicates the stock is trading at a premium on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Apellis Pharmaceuticals Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are worth introducing as a simple way for you to link your view of Apellis Pharmaceuticals to numbers like future revenue, earnings, margins and fair value.

A Narrative is your story about the company, written in plain language, that then connects directly into a financial forecast and a fair value estimate instead of sitting separate from the models.

On Simply Wall St’s Community page, Narratives are set up so you can see how a particular story about Apellis translates into assumptions such as revenue growth, profit margins, P/E multiples and a fair value, then compare that fair value to the current share price to think about whether the stock looks cheap or expensive on that story.

Because Narratives on the platform update when new information like earnings, FDA decisions or deal terms arrive, they stay aligned with the latest data rather than being a one off snapshot.

For Apellis, one investor might align with the view that points to a Fair Value of about US$55.00 or even a US$60.00 price target based on stronger growth and margins, while another might lean toward a more cautious view that anchors on a Fair Value near US$19.00. Comparing those stories side by side can help you decide which Narrative feels more realistic for your own decision making.

For Apellis Pharmaceuticals however we will make it really easy for you with previews of two leading Apellis Pharmaceuticals Narratives:

Start by asking which version of the future feels closer to your own view, then use that to anchor how you think about the current US$41.01 share price and the earlier DCF and P/E signals.

Fair value in this bullish Narrative: US$55.00 per share.

Implied pricing gap vs last close: about 25.5% below this fair value level.

Revenue growth assumption: 14.05% a year.

- Sees EMPAVELI and SYFOVRE as potential long term leaders in their categories. This would support higher revenues if broad adoption and durable use play out as expected.

- Builds in rising profit margins. Analysts in this camp expect earnings to scale as operating discipline, pipeline progress and manufacturing scale take hold.

- Requires comfort with a higher future P/E multiple and meaningful earnings growth by 2028. It also assumes confidence that competitive and pricing risks do not materially derail the story.

Fair value in this more cautious Narrative: about US$40.93 per share.

Implied pricing gap vs last close: current price is about 0.2% above this fair value level.

Revenue growth assumption: 7.87% a year.

- Frames Apellis as broadly in line with analyst expectations, with growth from rare kidney and eye indications but more modest revenue and margin expansion than the bullish view assumes.

- Highlights dependence on SYFOVRE and EMPAVELI, ongoing R&D spend and potential pricing pressure as factors that could keep the stock closer to fair value if execution or policy developments fall short of best case hopes.

- Assumes a relatively high future P/E multiple to justify fair value, alongside a wide range of possible earnings outcomes that reflects disagreement among analysts.

Both Narratives use the same raw building blocks, yet arrive at different views of what the stock is worth and how much growth and profitability are realistic. The key step for you is deciding which set of assumptions feels more reasonable and then checking whether the current share price still makes sense once those assumptions are in place.

If you want to see how these stories play out in full forecasts, including detailed risks and valuation links back to the latest market price, To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Apellis Pharmaceuticals on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Apellis Pharmaceuticals? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.