Is It Too Late To Consider Costco Wholesale (COST) After Its Strong Multi Year Share Price Run?

Costco Wholesale Corporation COST | 0.00 |

- If you are wondering whether Costco Wholesale at US$1,016.42 is priced for perfection or still holds value for new money, the key is to look past the headline share price and into how it stacks up on core valuation checks.

- The stock has returned 2.3% over the last 7 days, 0.1% over the past month, 18.9% year to date and 1.2% over the last year, with longer term returns of 111.3% over 3 years and 183.7% over 5 years. These figures provide useful context for where sentiment sits today.

- Recent coverage has focused on Costco Wholesale's role as a major US consumer retailer, with attention on how its membership model and warehouse format position it in the broader sector. This backdrop helps frame why investors may be reassessing the stock's balance between quality, growth profile and current price.

- Despite that, Costco Wholesale currently has a valuation score of 0 out of 6. The next step is to compare what different valuation methods say about the stock and then look at an even better way to make sense of those numbers by the end of this article.

Costco Wholesale scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

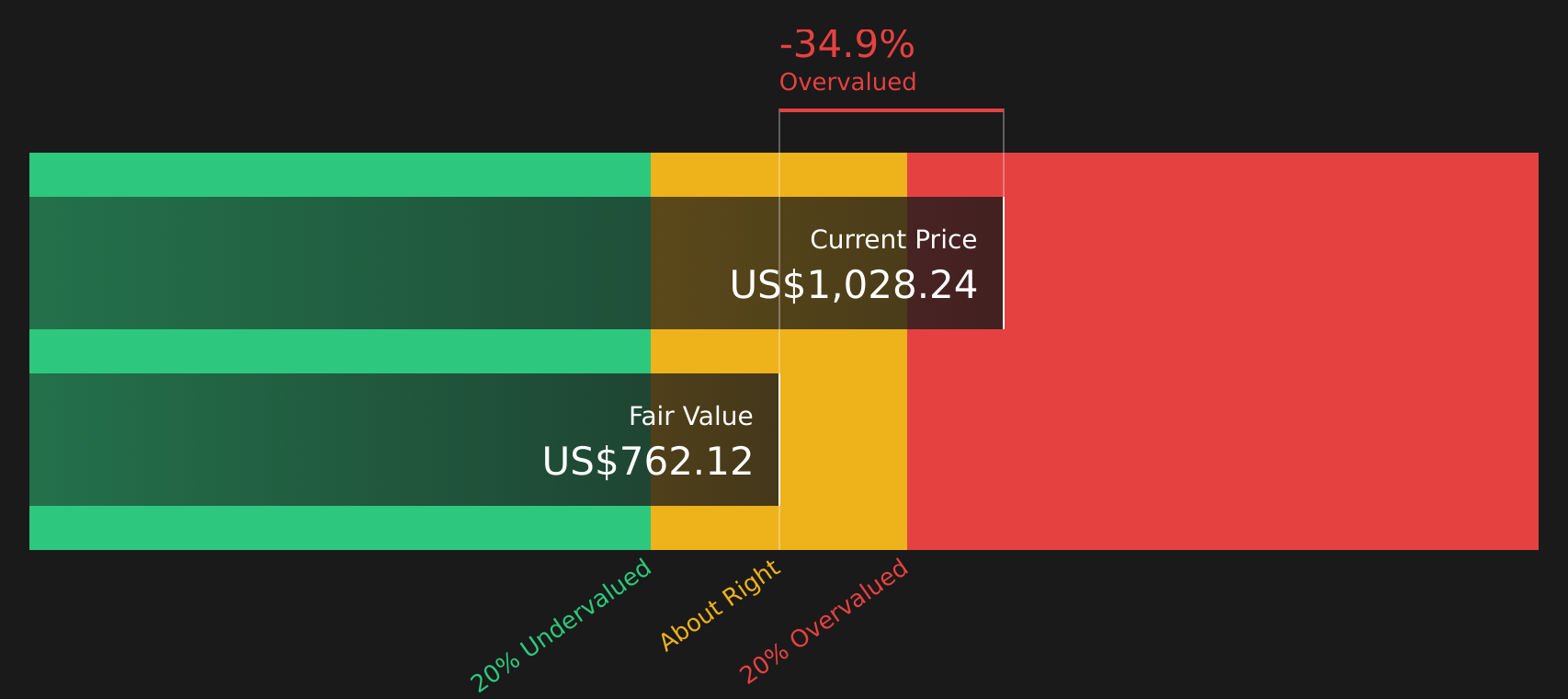

Approach 1: Costco Wholesale Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows, then discounts them back to today to estimate what the business might be worth right now. It is essentially asking what those future dollars are worth in today’s money.

For Costco Wholesale, the model uses current Free Cash Flow of about $9.5b and a 2 Stage Free Cash Flow to Equity approach. Analyst forecasts cover several years ahead, with projected Free Cash Flow of $11.996b in 2029, and Simply Wall St extrapolates further to reach around $17.6b in 2035. Each of these cash flows is discounted using the model’s assumptions to arrive at a present value stream.

On this basis, the estimated intrinsic value is $779.69 per share, compared with a current share price of $1,016.42. The intrinsic discount figure indicates the stock screens as roughly 30.4% overvalued against this DCF output.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Costco Wholesale may be overvalued by 30.4%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Costco Wholesale Price vs Earnings

For profitable companies, the P/E ratio is a straightforward way to connect what you pay for the stock with the earnings it generates. It helps you see how many dollars of price the market is placing on each dollar of earnings.

A “normal” or “fair” P/E typically reflects what investors are willing to pay for a company’s growth outlook and risk profile. Higher expected earnings growth or lower perceived risk can support a higher P/E, while slower growth or higher risk tends to justify a lower P/E.

Costco Wholesale currently trades on a P/E of 52.75x. This is well above the Consumer Retailing industry average of 18.37x and also above the peer group average of 23.83x. Simply Wall St’s Fair Ratio for Costco Wholesale is 40.91x, which is its proprietary view of what the P/E might be given factors such as earnings growth, profit margins, industry, market cap and risk profile.

Because the Fair Ratio incorporates those fundamentals rather than just comparing headline multiples to peers or the broad industry, it can give you a more tailored sense of whether the stock’s earnings multiple looks stretched or conservative. With Costco Wholesale trading at 52.75x against a Fair Ratio of 40.91x, the stock screens as valued above this Fair Ratio.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Costco Wholesale Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St give you a clear story behind your numbers by allowing you to link your view of Costco Wholesale’s future revenue, earnings and margins to a financial forecast and a Fair Value. You can then compare that Fair Value with today’s price to decide if the stock looks attractive or expensive for you. Each Narrative lives on the Community page, updates automatically when new earnings or news arrive, and can capture very different perspectives. For example, one Costco Narrative assumes a Fair Value near US$489 per share, another around US$726, and a more optimistic view near US$1,529, all using the same company but different assumptions about growth, margins and future P/E.

For Costco Wholesale, however, we will make it really easy for you with previews of two leading Costco Wholesale Narratives:

Start with a bullish view if you think the current price still lines up with long term growth and margin potential, or a more cautious view if you are worried about valuation pressure outweighing the quality of the business.

Here is how two detailed Community Narratives currently frame that trade off for you.

Fair value: US$1,047.90

Implied pricing gap versus last close: 3.0% discount to this narrative fair value

Revenue growth assumption: 7.52%

- Focuses on membership growth, new warehouses and extended gas station hours as key drivers of higher traffic and sales, alongside growing e commerce and international operations.

- Builds its earnings path on analyst assumptions for mid single digit revenue growth, a small uplift in profit margins and modest share count growth, all discounted at about 7.0%.

- Frames the stock as close to fairly priced against the analyst consensus target, and encourages you to check whether those revenue, margin and P/E assumptions fit your own view of Costco Wholesale.

Fair value: US$726.29

Implied pricing gap versus last close: 40.0% premium to this narrative fair value

Revenue growth assumption: 7.0%

- Highlights Costco Wholesale as a high quality business with a wide moat and strong membership model, but argues the stock is priced for perfection at around a 50x P/E.

- Sets out base, bear and bull return scenarios that all depend heavily on how much the earnings multiple compresses or holds, even when revenue growth and margins are assumed to be solid.

- Flags valuation, tariff exposure and renewed competition from other warehouse retailers as key risks that could limit returns if growth or market expectations fall short.

If you want to see how other investors are weighing these same trade offs and where your own view sits on that spectrum, you can compare these with the rest of the Community Narratives on Costco Wholesale.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Costco Wholesale on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Costco Wholesale? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.