Is It Too Late To Consider Nvidia (NVDA) After AI Data Center Boom Fueled Gains?

NVIDIA Corporation NVDA | 0.00 |

- For investors wondering whether NVIDIA stock still offers value or whether most of the story is already reflected in the price, this article walks through what the current valuation signals indicate.

- After some short term volatility, with the share price down 1% over the last week, NVIDIA has still returned 10.6% over the past month, 18.3% year to date and 69.6% over the last year, along with a very large 3 year gain and an even larger 5 year gain.

- Recent headlines have kept NVIDIA at the center of discussions about AI hardware, data center build outs and the chips that power these trends. This backdrop helps explain why the stock price has been so sensitive to any updates on demand for its products and the competitive response from other chip companies.

- NVIDIA currently holds a valuation score of 3 out of 6. The next section explains how different methods such as discounted cash flow analysis, multiples and comparables line up with that score, followed by a more complete way to think about valuation at the end of the article.

Approach 1: NVIDIA Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of the cash a company could generate in the future and discounts those cash flows back into today’s dollars to arrive at an intrinsic value per share.

For NVIDIA, the model used here is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $97.2b. Analyst estimates and further extrapolations by Simply Wall St project free cash flow reaching about $530.9b by 2035, with specific waypoints such as $96.0b in 2026 and $417.5b in 2031, all expressed in dollars.

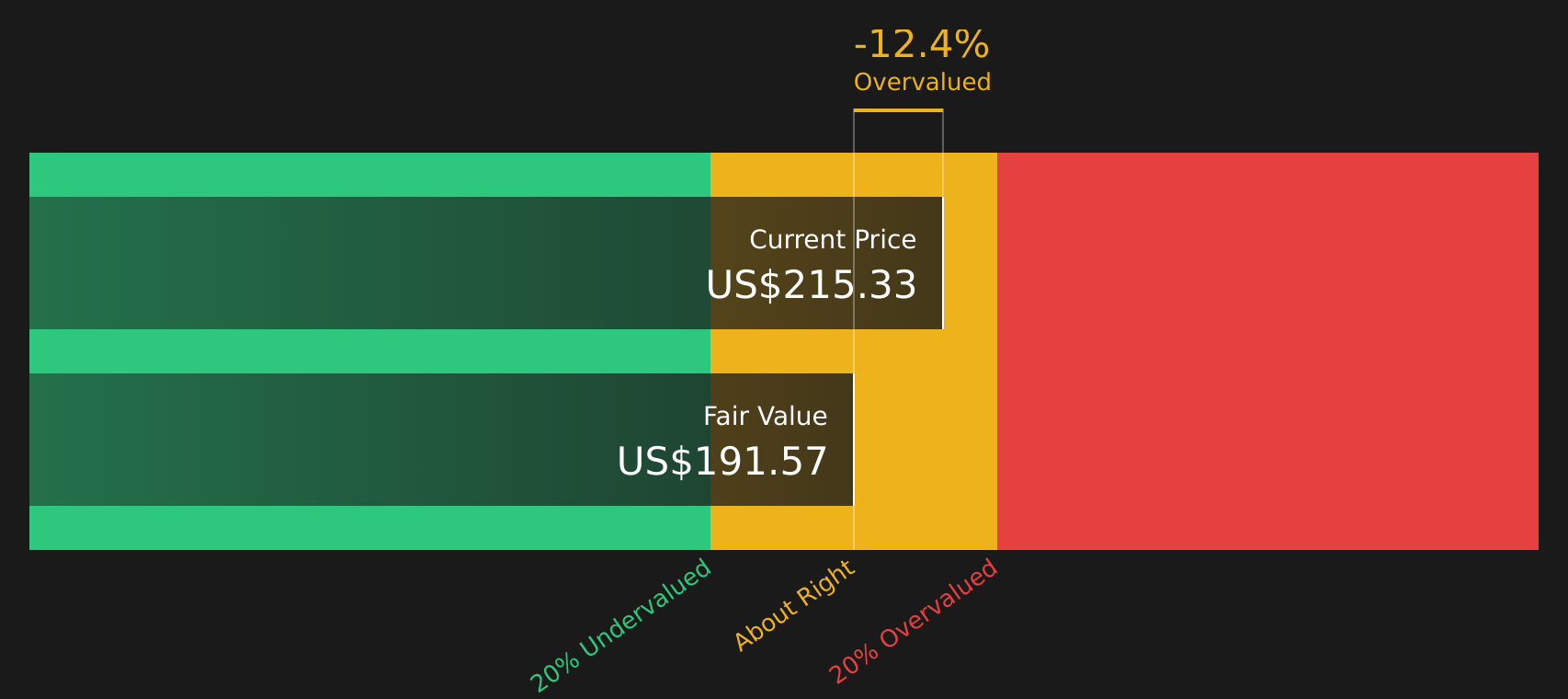

After discounting these projected cash flows back to today, the model produces an estimated intrinsic value of $185.60 per share. Compared with the current share price, the DCF output indicates that the stock is trading about 20.4% above this estimate, which means it screens as overvalued under this particular model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NVIDIA may be overvalued by 20.4%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NVIDIA Price vs Earnings

For profitable companies, the P/E ratio is a useful way to see how much investors are paying for each dollar of earnings, which makes it a common starting point when you are comparing stocks in the same sector.

A “normal” or “fair” P/E usually reflects what the market is willing to pay for a company’s earnings given its growth outlook and perceived risk. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to justify a lower one.

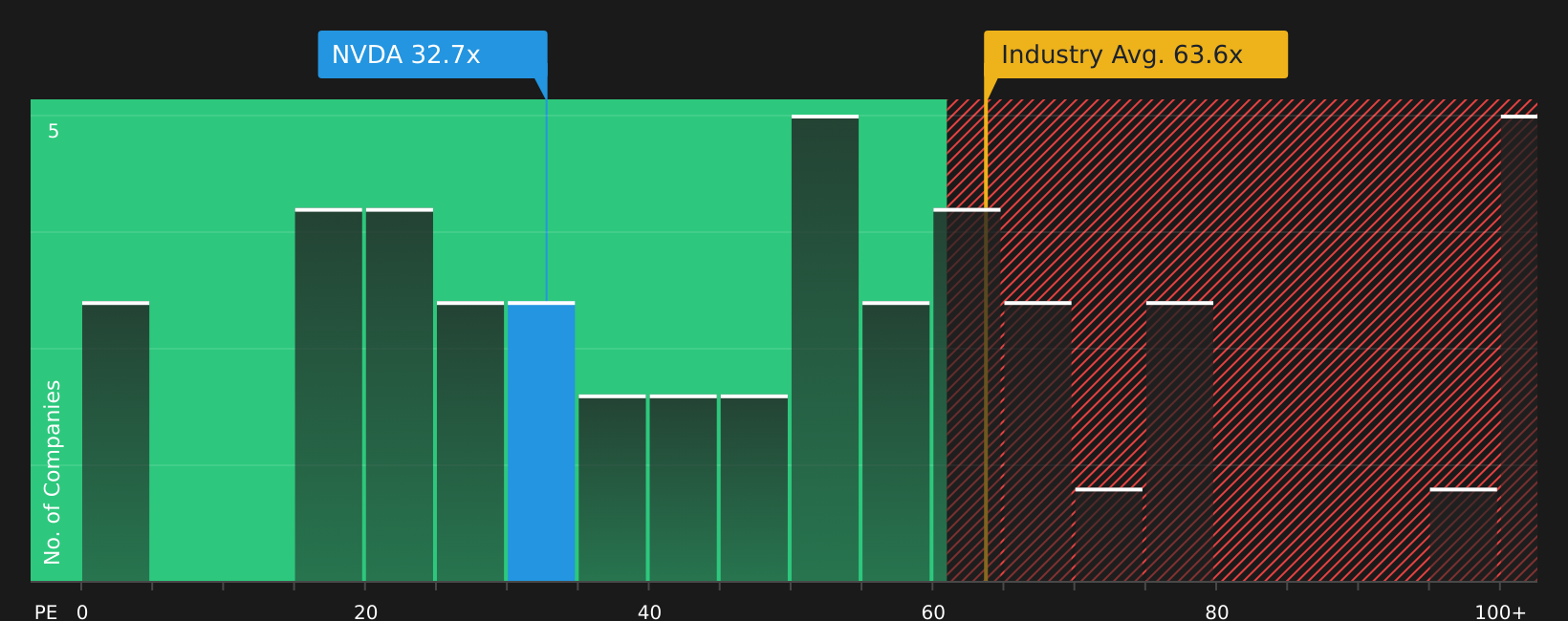

NVIDIA currently trades on a P/E of 45.1x. This sits below the peer group average of 78.4x and the broader Semiconductor industry average of 63.0x. Simply Wall St’s “Fair Ratio” framework estimates a fair P/E of 52.1x for NVIDIA, based on factors such as its earnings growth profile, profit margins, industry, market cap and risk characteristics.

This Fair Ratio is designed to be more tailored than a simple peer or industry comparison, because it adjusts for company specific factors instead of assuming all semiconductor stocks deserve similar multiples. Comparing the 45.1x market P/E with the 52.1x Fair Ratio suggests the stock appears undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your NVIDIA Narrative

Earlier we mentioned that there is an even better way to think about valuation. This is where Narratives come in, a simple way for you to attach a clear story about NVIDIA to the numbers you already care about, like fair value, future revenue, earnings and margins.

A Narrative is your own worked through view of the company, where you link NVIDIA’s story, such as AI factories or competition from custom chips, to a financial forecast and then to a fair value, instead of just looking at a single metric in isolation.

On Simply Wall St’s Community page, Narratives are available as an easy tool used by millions of investors. You can see and build valuations without spreadsheets, then compare your fair value with the current price to decide whether the stock looks expensive or cheap against your assumptions.

Narratives update automatically when new information like earnings, export controls or large AI infrastructure deals are added to the platform. This means your framework moves with the news instead of going stale between quarters.

For example, one NVIDIA Narrative on the Community pegs fair value around US$90, assuming revenue growth slows and margins compress. Another uses stronger AI demand, higher margins and a richer future P/E to arrive near US$335. A third Narrative that leans into very strong data center growth and margin resilience reaches about US$571, giving you a clear spread of stories and numbers to compare against your own view.

For NVIDIA however we will make it really easy for you with previews of two leading NVIDIA Narratives:

Fair value: US$339.90 per share

Current price vs this fair value: around 34.2% below this Narrative’s estimate

Revenue growth in the model: 30.0%

- Expects NVIDIA to reach US$400b in annual revenue in five years, with around 90% tied to data center customers and large scale AI infrastructure.

- Sees GPU and software dominance as central, but flags risks from competing chip designers, potential CUDA alternatives and the need for each new architecture to justify data center upgrade cycles.

- Highlights external constraints such as power availability, regulation around AI and energy, and the higher cost of nuclear and other generation options as possible brakes on the most optimistic outcomes.

Fair value: US$141.74 per share

Current price vs this fair value: around 57.7% above this Narrative’s estimate

Revenue growth in the model: 17.2%

- Focuses on NVIDIA’s strong positions in data centers, gaming, automotive and Omniverse, but assumes more modest long run growth and profits than recent years.

- Builds in pressure from rising competition, potential margin compression, regulatory pushback and supply chain issues which could limit how much of the AI and data center opportunity the company converts into earnings.

- Uses a 40.0% net margin and a 60x future P/E in its forecast, which still implies high expectations, and treats some newer opportunities as optional rather than fully reflected in the valuation.

If you want to see how those narratives are built, and how your own assumptions compare, it is worth reading the full community versions and then saving NVIDIA to your watchlist so you can see how the valuation story changes over time.To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for NVIDIA on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for NVIDIA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.