Is It Too Late To Consider Oracle (ORCL) After Its Rapid Share Price Rally?

Oracle Corporation ORCL | 0.00 |

- If you are wondering whether Oracle's share price still makes sense after a strong run, this article walks through what the current valuation actually implies for you.

- At a last close of US$236.34, Oracle's stock has delivered returns of 16.0% over 7 days, 27.5% over 30 days, 20.8% year to date, 39.5% over 1 year, 127.8% over 3 years and 207.3% over 5 years.

- Recent coverage has focused on Oracle's role in software and cloud infrastructure, and how its positioning in these areas may be shaping investor expectations. This context helps explain why the stock's recent performance has attracted attention from both new and existing shareholders.

- On Simply Wall St's valuation checks, Oracle currently has a value score of 4 out of 6. Next up is a look at what different valuation methods say about the stock today, plus a more complete way to think about value that will be covered at the end of the article.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company's future cash flows and discounts them back to today to arrive at an estimate of what the business might be worth on a per share basis.

For Oracle, the latest twelve month free cash flow is a loss of about $2.2b. Analysts and Simply Wall St projections then extend out to at least 2035, with free cash flow estimates ranging from a loss of $24.3b in 2026 to a projected $150.2b in 2035, all expressed in $. These figures come from a 2 Stage Free Cash Flow to Equity model that uses analyst inputs for the earlier years and extrapolations thereafter.

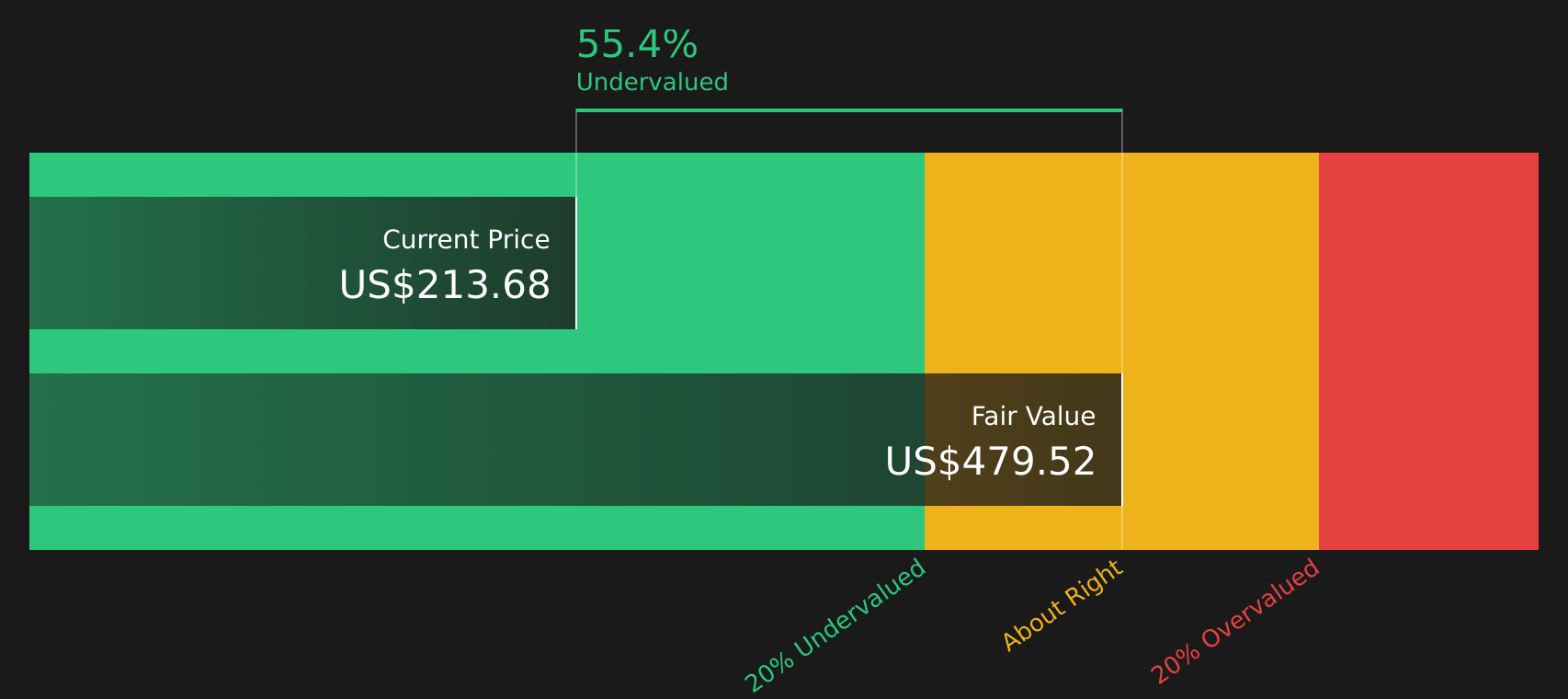

Based on these cash flow projections, the model arrives at an estimated intrinsic value of about $461.80 per share. Against a recent share price of $236.34, this implies the stock trades at a 48.8% discount to the DCF estimate. On this specific model, Oracle stock appears to be undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle is undervalued by 48.8%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Oracle Price vs Earnings

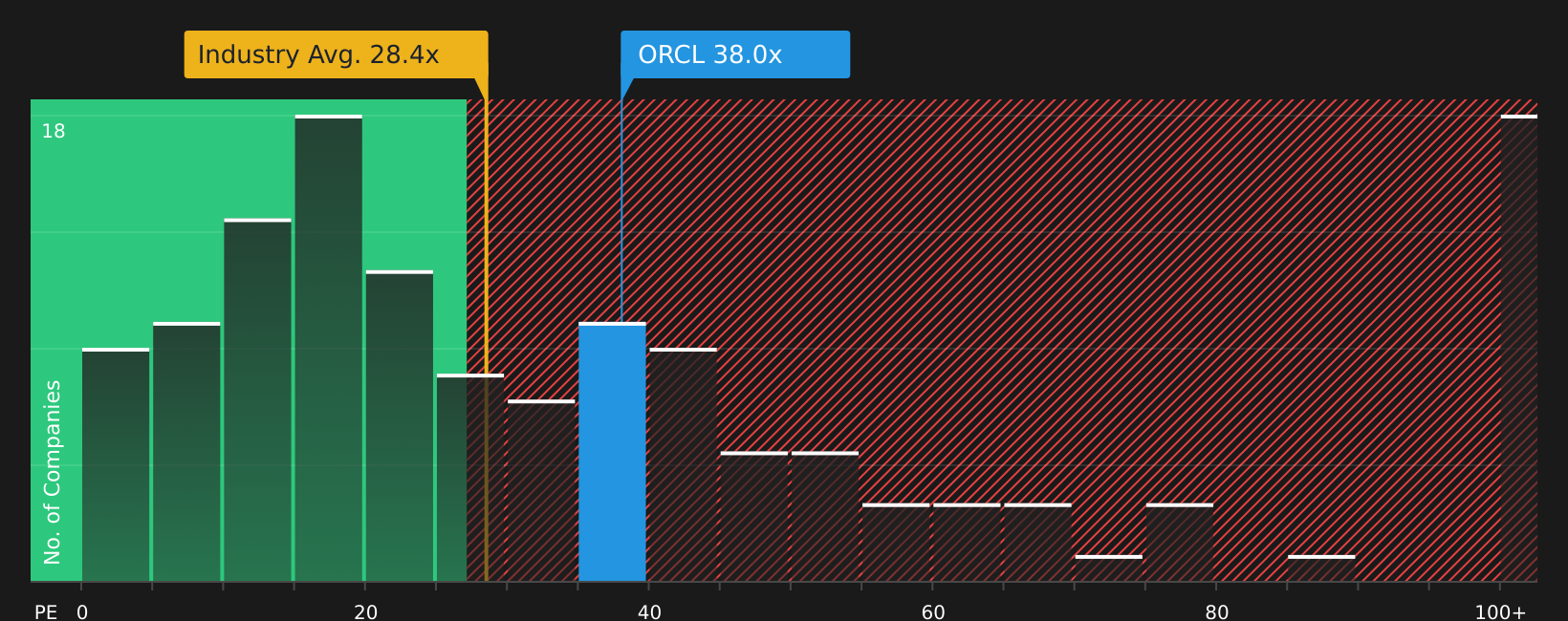

For profitable companies, the P/E ratio is a straightforward way to link what you pay for the stock to the earnings the business is currently generating. It helps you see how many dollars investors are paying today for each dollar of earnings.

What counts as a “normal” or “fair” P/E depends on factors like expected earnings growth and risk. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually point to a lower one.

Oracle currently trades on a P/E of 41.99x, compared with the Software industry average of 29.24x and a peer group average of 105.39x. Simply Wall St’s Fair Ratio for Oracle is 60.05x. The Fair Ratio is a proprietary estimate of what the P/E might be, given the company’s earnings growth profile, industry, profit margins, market cap and risk characteristics.

Because it blends these company specific factors, the Fair Ratio can be more informative than a simple comparison with peers or the broad industry, which may have very different growth or risk profiles. On this measure, Oracle’s current P/E of 41.99x sits below the Fair Ratio of 60.05x, which points to the stock appearing undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are a way for you to put a clear story behind your numbers by linking your view of Oracle’s future revenue, earnings and margins to a concrete fair value that you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are short, accessible forecasts created by investors that connect a company’s story to a financial model, then translate that into a Fair Value so you can quickly see whether your view suggests the stock is priced above or below what you think it is worth and decide if that lines up with your own buy or sell timing.

Narratives are refreshed when new information arrives, such as Oracle’s AI data center plans or updated revenue targets, so the numbers and the story stay in sync rather than becoming a static snapshot.

For Oracle right now, one Narrative on Simply Wall St assigns a Fair Value of about US$119.97 while another assigns about US$389.81 and a third sits near US$359.59. This shows how different investors can look at the same company, build different forecasts for revenue growth, profit margins and P/E, and end up with very different ideas of what the stock is worth today.

For Oracle however we will make it really easy for you with previews of two leading Oracle Narratives:

Both are built on the same company data but reach very different conclusions about what the stock is worth today. This contrast is exactly what helps you pressure test your own view before you act.

Fair Value: US$389.81

Implied discount to this Fair Value at US$236.34: about 39.4% undervalued

Revenue growth assumption: 28%

- Frames Oracle as an AI infrastructure partner for large workloads, with the OpenAI relationship and supercluster buildout at the center of the story.

- Highlights a very large Remaining Performance Obligations balance and heavy AI inference demand as key supports for contracted revenue.

- Emphasizes the "One Oracle" stack of infrastructure, database and applications, while also flagging execution, supply constraints and AI project risks that could disrupt this path.

Fair Value: US$155.00

Implied premium to this Fair Value at US$236.34: about 52.5% overvalued

Revenue growth assumption: 26.46%

- Argues that demand for open, interoperable and vendor neutral cloud options, plus cloud commoditization, could pressure Oracle’s pricing power and margins over time.

- Points to regulatory and compliance costs, legacy on premise softness and lower switching costs as potential drags on long term profitability and contract stickiness.

- Bases the Fair Value on a lower P/E multiple by 2029, even with higher modeled revenue and earnings, on the view that current market expectations may be too optimistic.

Taken together, these Narratives show how the same company data can justify very different fair values, depending on how you weigh AI data center spending, backlog visibility, margin risk and the price you are willing to pay for that growth.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.