Is It Too Late To Consider Oracle (ORCL) After Its Recent Multi Year Share Price Run?

Oracle ORCL | 0.00 |

- Investors may be wondering whether Oracle at around US$186.83 a share still offers value, or if most of the upside has already been priced in.

- The stock’s recent performance is mixed, with a 0.8% gain over the last week, a 35.3% rise over the past month, a decline of 4.5% year to date, and returns of 16.3% over 1 year, 97.0% over 3 years, and 154.0% over 5 years.

- Recent coverage has focused on Oracle’s position as a large software player, its role in supporting enterprise customers, and how investors view the stock after a strong multi year run. This context helps explain why shorter term moves can look quite different to the longer term performance profile.

- On Simply Wall St’s 6 point valuation checklist, Oracle scores a 4 out of 6. This suggests parts of the stock may still look attractive. The next sections will unpack how different valuation methods assess that, before finishing with a broader way to think about what the current price really implies.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return, to arrive at an intrinsic value per share.

For Oracle, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections in $. The latest twelve month free cash flow figure is a loss of about $2.2b, and analyst based projections out to 2030, followed by extrapolated estimates, show free cash flow moving from losses in the next few years to a projected $98.6b in 2035, with $31.2b indicated for 2030. Simply Wall St extends analyst inputs beyond the usual 5 year horizon to create this ten year path.

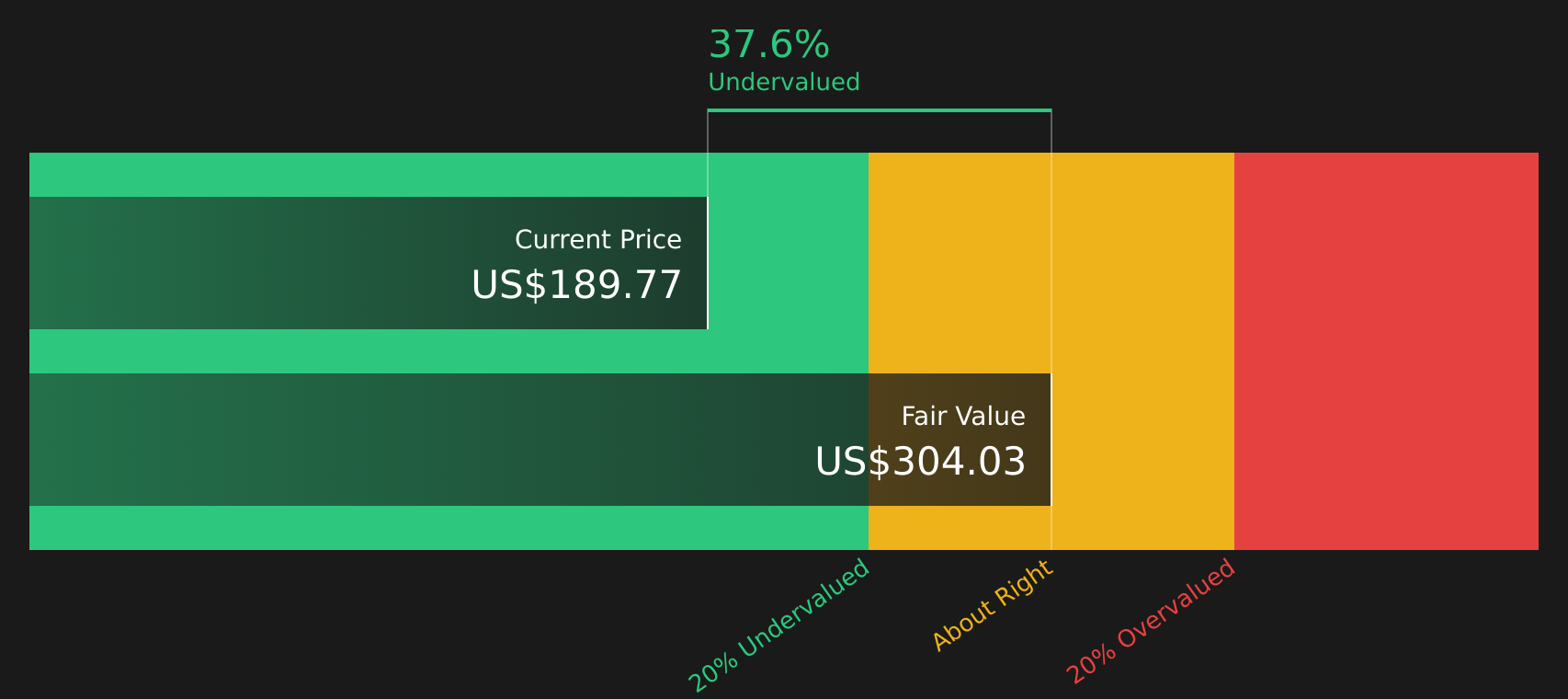

Discounting these projected cash flows results in an estimated intrinsic value of about $302.81 per share, compared with a recent share price around $186.83. On this model, the stock screens as about 38.3% undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle is undervalued by 38.3%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: Oracle Price vs Earnings

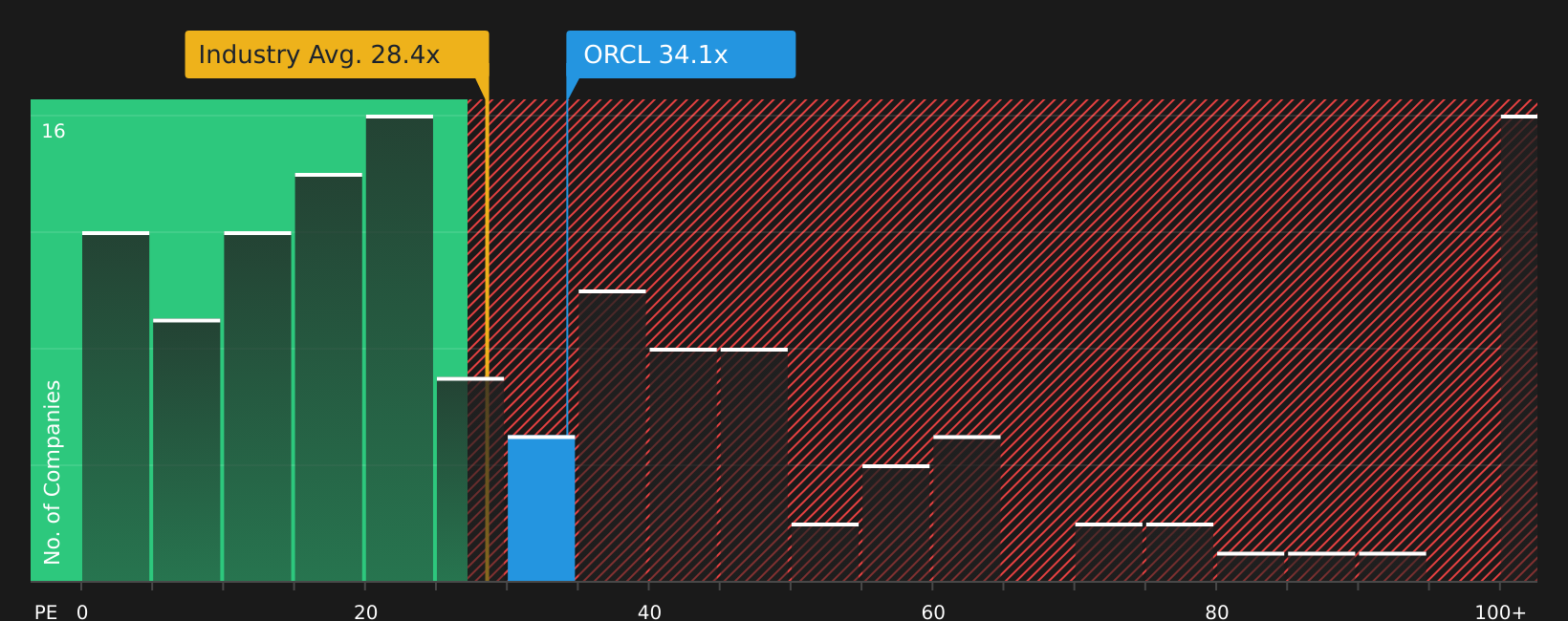

P/E is a useful way to think about value for profitable companies because it links what you pay for each share directly to the earnings that support that share. In simple terms, higher growth potential and lower perceived risk can justify a higher P/E, while slower growth and higher risk usually line up with a lower, more conservative range.

Oracle currently trades on a P/E of 33.19x. That sits above the broader Software industry average of 27.99x, but below a peer average of 63.88x. Simply Wall St also estimates a “Fair Ratio” of 61.15x for Oracle, which is the P/E that would be expected given factors such as its earnings profile, industry, profit margin, market cap and risk characteristics.

This Fair Ratio is more tailored than a simple comparison with peers or the industry, because it adjusts for company specific traits rather than assuming one size fits all. Comparing the Fair Ratio of 61.15x with the current P/E of 33.19x suggests the stock is trading below what this framework would indicate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple way for you to write the story behind your numbers by linking your view of Oracle’s future revenue, earnings and margins to a forecast and a Fair Value that you can compare with today’s share price.

A Narrative on Simply Wall St starts with your story. For example, you might think Oracle is a legacy database provider that could face pricing pressure, or a cloud and AI infrastructure leader that could support long term demand. The Narrative then ties that story directly to explicit assumptions about growth, profitability, discount rates and expected P/E.

On the Community page, where millions of investors share their work, Narratives make those stories and numbers transparent. You can see, for instance, one Oracle Narrative that sets Fair Value near US$119.97 and another far higher at about US$389.81, then decide for yourself which set of assumptions feels closer to your own view.

Because Narratives update as new information comes in, such as Oracle’s reported contract backlog, AI data center spending or analyst earnings estimates, your Fair Value stays in sync with the latest data and gives you a consistent, numbers based way to judge whether the stock looks expensive or attractive relative to your chosen Narrative at any point in time.

For Oracle, however, we will make it really easy for you with previews of two leading Oracle Narratives:

On one side you have a bullish AI infrastructure story that leans heavily on contract backlog, supercluster build outs and the whole stack model. On the other you have a more cautious view that stresses cloud commoditisation risk, regulation and questions around how much of today’s AI enthusiasm is already reflected in the share price.

Seen together, these Narratives bracket a reasonable range of outcomes for Oracle and give you a clear way to test which set of assumptions feels closer to your own expectations.

Fair Value: US$389.81 per share

Implied discount to Fair Value at US$186.83: about 52.1% undervalued

Revenue growth assumption: 28%

- Frames Oracle as an AI infrastructure leader, with the OpenAI partnership, large scale superclusters and very large Remaining Performance Obligations reinforcing demand for its Gen2 AI cloud.

- Highlights the whole stack approach across infrastructure, database and applications, where customers using multiple pillars tend to spend far more than those on a single product line.

- Flags execution, supply and AI project risk, but still anchors on a view that Oracle’s AI data center build out and backlog support a materially higher long term Fair Value than today’s price.

Fair Value: US$155.00 per share

Implied premium to Fair Value at US$186.83: about 20.5% overvalued

Revenue growth assumption: 24.4%

- Assumes that pressure from open, interoperable cloud platforms, regulatory costs and legacy software declines weigh on margins and limit how much incremental earnings Oracle can generate from AI and cloud.

- Bases Fair Value on a lower profit margin profile and a future P/E of 30.5x, close to sector levels, which keeps the overall analyst bearish target only slightly above a past share price reference.

- Accepts that there are powerful offsetting positives, including very large contracted backlogs and AI database capabilities, but treats these as risks to the bearish case rather than the central outcome.

If you want to see how other investors are framing the story and where your own expectations sit between these two poles, there is a broader range of community Narratives that link detailed assumptions on growth, margins and valuation directly to Oracle’s current share price. To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Oracle on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.