Is It Too Late To Consider Oracle (ORCL) After Its Strong Multi Year Share Price Run?

Oracle Corporation ORCL | 0.00 |

- Wondering if Oracle's current share price still makes sense after its strong run, or if the story has already played out? This article breaks down what the numbers are really saying about value.

- At a recent close of US$190.96, the stock has delivered returns of 1.5% over the past week and 10.4% over the past month, with 1 year and 5 year returns of 17.7% and 154.5% respectively, while being down 2.4% year to date.

- Recent headlines have focused on Oracle's positioning in software and cloud services and how that fits into broader market themes. This helps explain why the stock price has remained in focus for many investors, and provides useful context when you compare the share price to what various valuation methods suggest the company might be worth.

- Oracle currently scores 4 out of 6 on Simply Wall St's valuation checks, as shown by its valuation score. The rest of this article walks through key valuation approaches and then outlines a framework that can help you interpret these models more effectively.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and discounting them back to today using a required rate of return. It is essentially asking what those future dollars are worth in current terms.

For Oracle, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of about US$2.2b, and analyst based projections for the next several years remain mixed, with some years showing further free cash flow losses in the tens of billions of US dollars. Beyond the explicit analyst horizon, Simply Wall St extrapolates cash flows, with projected free cash flow of about US$31.2b in 2030.

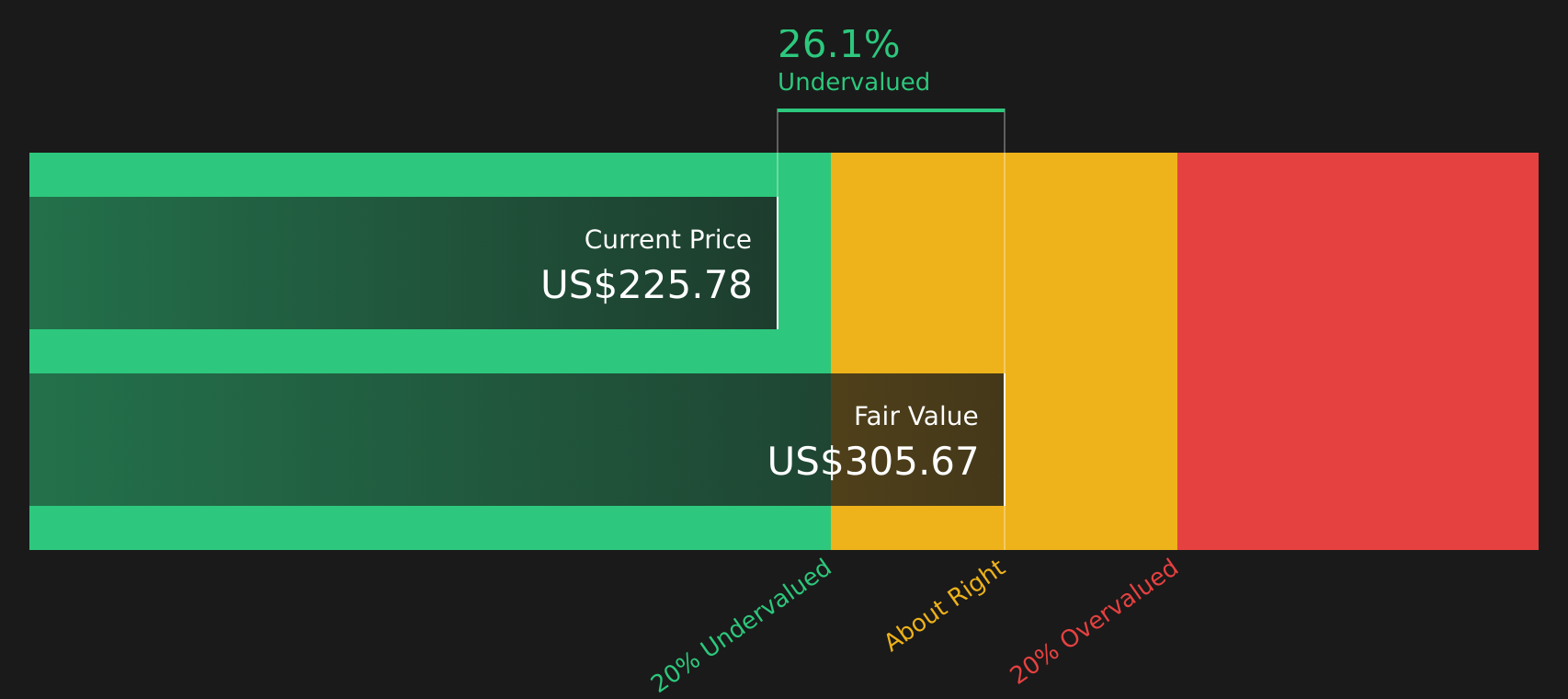

After discounting this stream of projected cash flows back to today, the DCF model arrives at an estimated intrinsic value of about US$304.07 per share. Compared with the recent share price of US$190.96, this implies the stock screens as around 37.2% undervalued on this specific cash flow based view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle is undervalued by 37.2%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Oracle Price vs Earnings

For profitable companies, the P/E ratio is a straightforward way to see how much you are paying for each dollar of current earnings. It is a useful cross check against more complex cash flow models.

What counts as a “normal” P/E will depend on how fast earnings are expected to grow and how risky those earnings appear. Higher growth or lower perceived risk can support a higher P/E, while slower growth or higher risk usually lines up with a lower one.

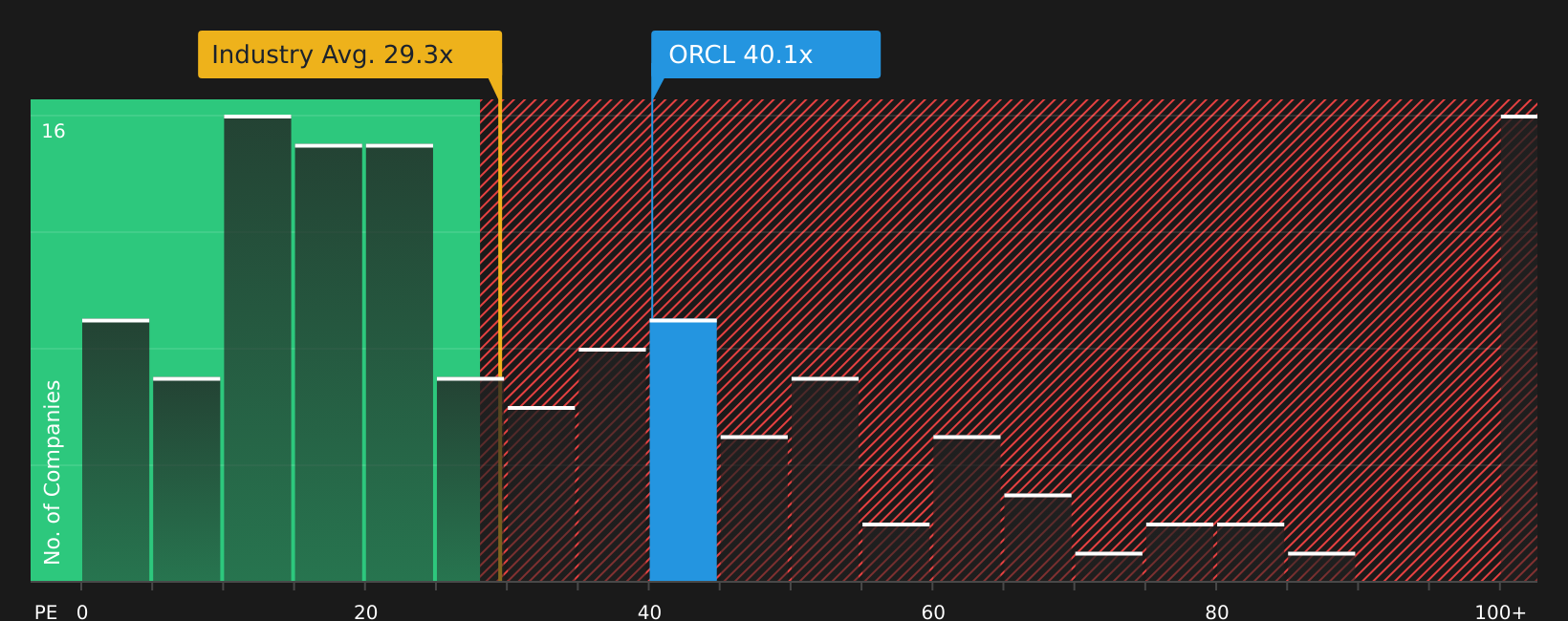

Oracle currently trades on a P/E of about 33.9x. That sits above the broader Software industry average of roughly 29.2x, but below the peer group average of about 72.4x. To add more context, Simply Wall St also calculates a proprietary “Fair Ratio” for the stock of around 61.2x.

The Fair Ratio is designed to be a more tailored benchmark than a simple peer or industry comparison, because it incorporates factors such as earnings growth, profit margins, risk profile, industry and market cap into one yardstick.

Comparing Oracle's current P/E of 33.9x with the Fair Ratio of 61.2x suggests the stock screens as undervalued on this earnings based view.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in as a simple way for you to connect your view of Oracle's story to concrete numbers like future revenue, earnings, margins and an estimated fair value.

A Narrative is your own story about the company that you translate into assumptions. For example, this can include how fast Oracle's cloud and AI businesses might grow, what profit margins could look like, and what P/E you think is reasonable. These assumptions then link directly to a fair value that you can compare with the current share price.

On Simply Wall St, Narratives are available on the Oracle Community page and across the platform. They are designed so you can easily see different story based forecasts side by side, then decide whether the stock looks expensive or cheap by comparing each Narrative fair value to the live market price.

Narratives update automatically when new information such as news or earnings is added. With Oracle you can already see a wide spread of views, from a more cautious fair value of about US$120 through to an optimistic view above US$350, reflecting how differently investors interpret the same business and price today.

For Oracle, however, we will make it really easy for you with previews of two leading Oracle Narratives:

On Simply Wall St, Narratives sit on a spectrum so you can quickly see how different assumptions on growth, margins and valuation translate into very different fair values for the same stock.

Here is how one bullish and one cautious Oracle Narrative compare, so you can decide which story feels closer to your own view and adjust from there.

Fair value: US$389.81 per share

Implied undervaluation vs current price: about 51.0%

Revenue growth assumption: 28%

- Frames Oracle as an AI infrastructure leader, highlighting very large Remaining Performance Obligations and demand for Gen2 AI infrastructure tied to OpenAI and other large customers.

- Emphasizes the "One Oracle" whole stack approach across infrastructure, database and applications, with customers that adopt multiple pillars modeled to spend far more over time.

- Flags execution, supply, AI project risk and investor skepticism as key uncertainties, but still aligns these assumptions with a much higher modeled fair value than today’s price.

Fair value: US$155.00 per share

Implied overvaluation vs current price: about 19.0%

Revenue growth assumption: 26.46%

- Focuses on pressure from open, interoperable cloud platforms and AI native alternatives that could weigh on pricing power, margins and long term revenue stability.

- Highlights regulatory, compliance and capital intensity risks, along with the drag from legacy on premise software and the possibility that cloud growth does not fully offset older revenue streams.

- Anchors on a lower analyst price target that assumes thinner profit margins, a lower future P/E multiple and heavier AI data center spending before free cash flow improves.

Taken together, these two Narratives show how the same company, price and data can justify very different conclusions once growth, margin and valuation assumptions change. The key is to decide which set of assumptions feels more realistic to you, then adjust the inputs until the fair value lines up with your own view of Oracle.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.