Is It Too Late To Consider Seadrill (SDRL) After A 137% One Year Surge?

Seadrill Limited SDRL | 0.00 |

- If you are wondering whether Seadrill shares at around US$49.79 are offering value or asking you to pay up for recent excitement, this article breaks down the numbers in a clear, practical way.

- The stock has delivered returns of 5.9% over the last week, 9.6% over the last month, 42.5% year to date, and 137.1% over the past year, which naturally raises questions about what is already priced in.

- Recent coverage has focused on Seadrill as an offshore drilling name in the Energy Services space, with attention on how investors are weighing sector specific risks against company specific prospects. Headlines around contract activity, balance sheet positioning, and industry conditions help frame why the share price has been drawing interest.

- Seadrill currently has a valuation score of 2/6. The next step is to compare what different methods such as multiples and cash flow based models say about that price, before looking at a broader way to think about valuation later in the article.

Seadrill scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Seadrill Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth by projecting future cash flows and then discounting them back to today’s value using a required return.

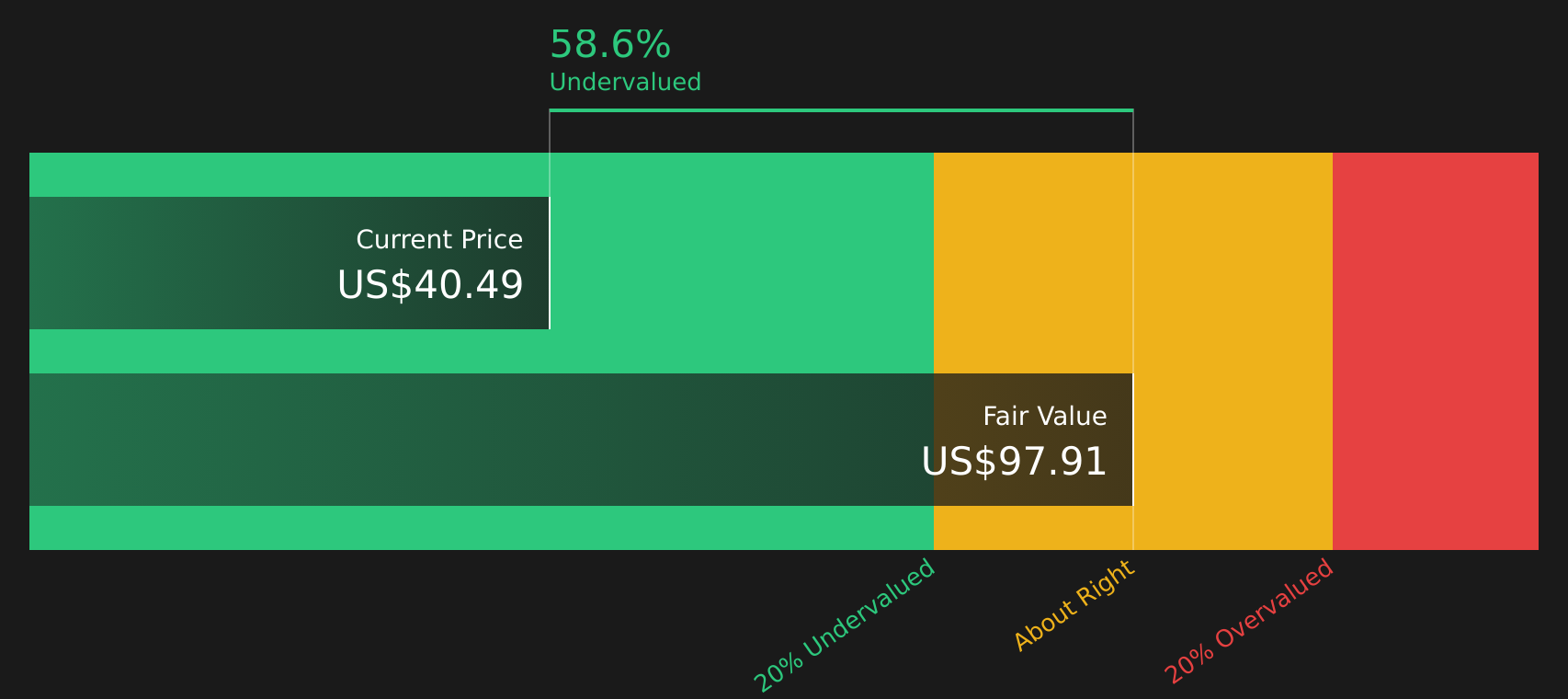

For Seadrill, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is a loss of $150.6 million. Analysts provide explicit estimates out to 2027, with free cash flow for that year projected at $262 million. Beyond that, Simply Wall St extrapolates estimates, with projected free cash flow in 2035 of about $1.6 billion, all kept in dollar terms and discounted back to today using the model’s assumptions.

Adding these discounted cash flows together results in an estimated intrinsic value of about $417.34 per share, compared with the recent price around $49.79. On this framework, the stock screens as about 88.1% undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Seadrill is undervalued by 88.1%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Seadrill Price vs Sales

For companies where earnings can be volatile or negative, P/S is often a useful way to compare what the market is paying for each dollar of revenue. It sidesteps short term swings in profit, while still reflecting how investors balance growth expectations and risk when deciding what feels like a normal trading range.

Higher growth and lower perceived risk usually support a higher P/S, while slower growth or higher risk tend to justify a lower multiple. Seadrill currently trades on a P/S of 2.25x. This sits above the Energy Services industry average of 1.47x and the peer average of 1.05x, so on simple comparisons the shares look more expensive than many peers.

Simply Wall St’s Fair Ratio for Seadrill is 1.13x, which is its view of what a reasonable P/S could be after weighing factors such as growth profile, risk, profit margins, industry and market cap. This is more tailored than a basic peer or industry comparison, which may overlook company specific traits. With the current P/S of 2.25x versus a Fair Ratio of 1.13x, the shares screen as overvalued on this metric.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Seadrill Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives step in as a simple way for you to write the story behind your numbers, linking what you believe about Seadrill’s contracts, margins and risks to a financial forecast and a Fair Value. You can then compare that Fair Value with today’s price to help you decide if you prefer to buy, hold or sell.

On Simply Wall St’s Community page, Narratives are easy to access and update automatically when new earnings, contracts or guidance land. For example, if one investor thinks Seadrill justifies a Fair Value around the higher end of analyst targets near US$76.37, while another anchors closer to the lower end around US$41.00, each can quickly see how their own revenue, earnings and P/E assumptions line up with the current share price and choose the Narrative that best matches their view of the company.

For Seadrill however we will make it really easy for you with previews of two leading Seadrill Narratives:

Start with the bullish case if you think the recent run still leaves room for more, then balance it with the caution from a lower Fair Value view so you can see which set of assumptions feels closer to your own.

Fair Value in this bullish narrative: US$76.37 per share.

At a recent price around US$49.79, that implies the shares are about 34.8% below this Fair Value on the author's assumptions.

Revenue growth assumption: 10.9% a year.

- Emphasis on a modern, high specification fleet, digital tools and managed pressure drilling to support stronger margins and pricing power in offshore drilling.

- View that longer term Brazilian contracts, contract extensions and growing backlog could support higher revenues, utilization and cash generation into the next decade.

- Acknowledges risks around energy transition, ESG pressure, rig oversupply and leverage, but concludes that higher earnings and a P/E of 25.8x on 2029 earnings could still justify a Fair Value of about US$76.

Fair Value in this more cautious narrative: US$41.00 per share.

At a recent price around US$49.79, that implies the shares are about 21.4% above this Fair Value on the author's assumptions.

Revenue growth assumption: 3.6% a year.

- Focus on the risk that growing renewables adoption, net zero policies and capital shifting away from hydrocarbons could weigh on Seadrill's long term contract pipeline and backlog duration.

- Flags ESG costs, regulatory pressure, aging stacked rigs and capex needs as potential drags on margins, free cash flow and earnings stability, even with new technology investments.

- Assumes a Fair Value of US$41 based on slower revenue growth, higher long term margin pressure and a P/E of 14.6x on 2029 earnings, suggesting less upside from current levels on this view.

Do you think there's more to the story for Seadrill? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.