Is It Too Late To Reassess Super Micro Computer (SMCI) After Recent AI Server Surge?

Super Micro Computer, Inc. SMCI | 0.00 |

- Wondering whether Super Micro Computer stock still offers value or if the easy gains are behind it? This article breaks down what the current price actually implies.

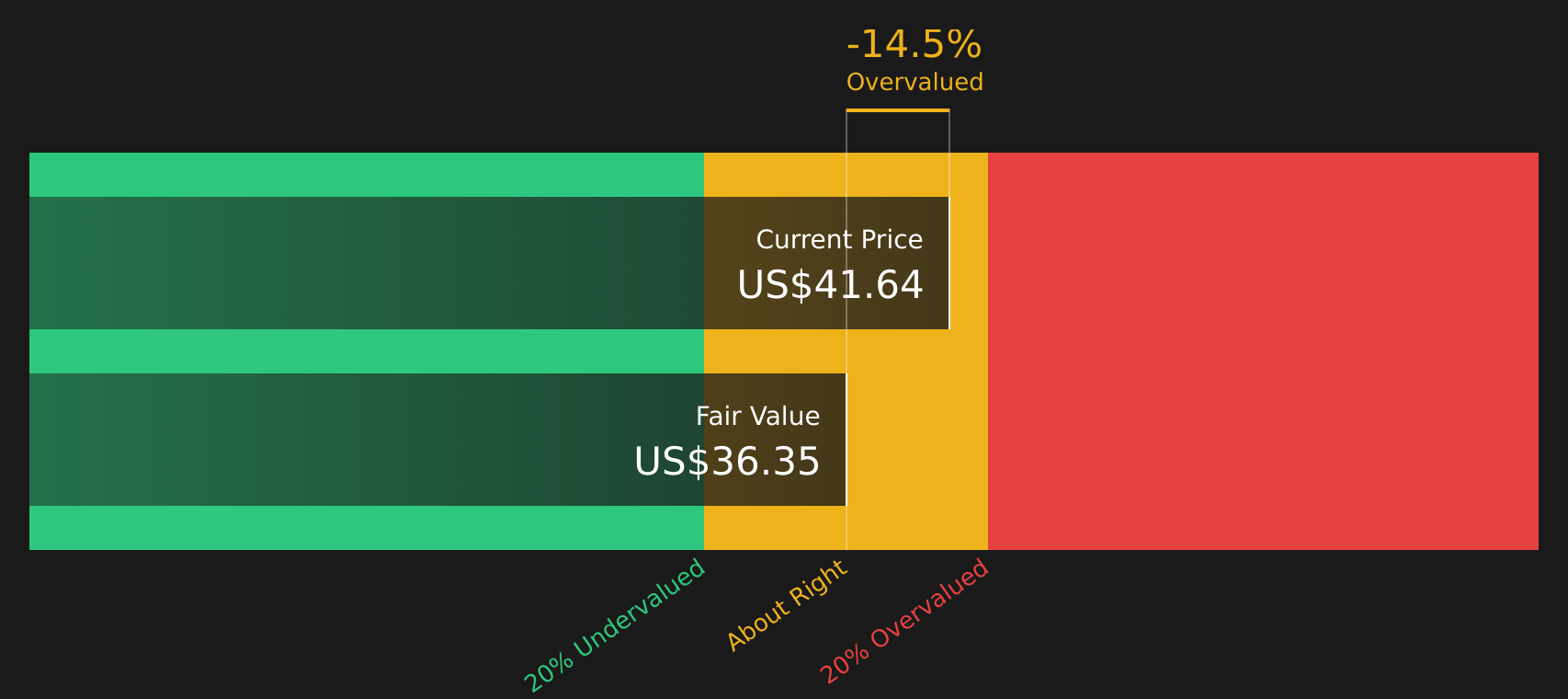

- The stock recently closed at US$41.64, with returns of 34.5% year to date, about 20.1% over the last month and a decline of 9.7% in the past week, while the 1 year return sits at 0.2%.

- Recent coverage has focused on Super Micro Computer as part of broader discussions around AI infrastructure and high performance computing hardware. This helps explain why the stock has attracted renewed attention after a mixed short term performance. Investors are watching how these themes feed into demand expectations, capital spending plans and competitive positioning for the company.

- On Simply Wall St’s 6 point valuation checklist Super Micro Computer scores a 3, meaning the stock screens as undervalued on half of the tests. The next sections will compare different valuation methods and then finish with a framework that can help you judge whether those numbers really fit your own view of the stock.

Approach 1: Super Micro Computer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and discounting them back to today using a required rate of return. It is essentially asking what all of Super Micro Computer’s future cash generation is worth in today’s dollars.

For Super Micro Computer, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model. The latest twelve month free cash flow is a loss of $6,890.86m. Analyst and extrapolated estimates see free cash flow moving to $2,772.15m in 2035, with interim projections such as $565.63m in 2028 and $980.08m in 2029. Simply Wall St discounts each of these annual cash flows, all in $, back to today and sums them to arrive at an estimated intrinsic value per share of $37.08.

Compared with the recent share price of $41.64, this DCF output implies Super Micro Computer trades at about a 12.3% premium, so the stock screens as overvalued on this model alone.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Super Micro Computer may be overvalued by 12.3%. Discover 49 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Super Micro Computer Price vs Earnings

The P/E ratio is a common way to value profitable companies because it links what you pay for the stock to the earnings the business is already generating. In general, higher growth expectations and lower perceived risk can justify a higher P/E, while slower expected growth or higher risk tend to line up with a lower, more cautious P/E range.

Super Micro Computer currently trades on a P/E of 20.1x. That sits below the broader Tech industry average P/E of 25.5x and well below the peer group average of 52.4x. On those simple comparisons, the stock looks cheaper than many alternatives in its space.

Simply Wall St’s Fair Ratio for Super Micro Computer is 52.7x, which is an estimate of what the P/E might be if factors like the company’s earnings growth profile, profit margins, industry, market cap and specific risks were all reflected. This Fair Ratio is more tailored than a plain industry or peer comparison because it adjusts for those company specific drivers rather than treating all Tech stocks as the same. Comparing the Fair Ratio of 52.7x with the current P/E of 20.1x suggests the stock screens as undervalued on this metric.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Super Micro Computer Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Now meet Narratives, a simple tool on Simply Wall St’s Community page that lets you attach a clear story about Super Micro Computer to the numbers you think are fair for its future revenue, earnings and margins. It then instantly turns that story into a fair value you can compare with the current share price to help you decide if the stock looks interesting, stretched or somewhere in between. Those fair values update automatically as new earnings or news arrive. This is why one investor’s cautious Super Micro Computer view might translate to a fair value around US$16 per share, while another is comfortable with assumptions that support a fair value closer to US$57, all within the same platform.

For Super Micro Computer however, we will make it really easy for you with previews of two leading Super Micro Computer Narratives:

Fair value: about US$50.30 per share

Implied pricing gap vs recent close: the stock sits about 17.2% below this narrative fair value

Revenue growth assumption used: 12.5%

- Sees Super Micro Computer as a leading AI server manufacturer with operational agility and a close NVIDIA partnership that helps it bring new systems to market quickly.

- Highlights a shift in focus from lower margin standalone servers to higher margin rack scale and liquid cooled data center solutions, tied to rising AI and data center spending.

- Flags meaningful risks around margin pressure, dependence on a small set of suppliers and customers, and governance concerns, but still concludes that the current price sits below a cautiously estimated fair value.

Fair value: about US$33.20 per share

Implied pricing gap vs recent close: the stock sits about 25.4% above this narrative fair value

Revenue growth assumption used: 28.0%

- Focuses on strong AI infrastructure demand and Super Micro Computer’s modular data center solutions as key drivers for potential revenue growth and margin recovery over time.

- Emphasizes execution and competitive risks, including reliance on a handful of large customers, hardware commoditization, pricing pressure and exposure to global supply chain and regulatory issues.

- Uses analyst assumptions for earnings, margins and a future P/E of 11.7x to arrive at a consensus fair value of US$33.20, which sits below the recent share price and frames the stock as pricing in more optimism than this narrative supports.

These two narratives show how reasonable investors, using different assumptions on margins, customer risk and fair P/E levels, can reach very different views on what Super Micro Computer is worth. If you want to test where your own expectations sit between these views, you can build and track a custom narrative directly on the Community page alongside To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Super Micro Computer on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Super Micro Computer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.