Is Klarna Group (KLAR) Starting To Look Attractive After A 46.9% Year-To-Date Decline?

Klarna Group Plc KLAR | 0.00 |

- Wondering whether Klarna Group at US$15.17 is starting to look like value, or if the recent moves are just noise.

- The stock is up 4.6% over the last 7 days and 0.7% over the last month, but is still down 46.9% year to date, which may change how you think about its risk and return profile.

- Recent news flow around Klarna Group has focused on its position in diversified financials and ongoing interest in its business model. This gives investors plenty to weigh against the share price moves. Headlines have highlighted how sentiment toward the stock can shift quickly as the market reassesses its prospects.

- Klarna Group currently has a valuation score of 3/6. The next step is to look at how different valuation methods line up on the stock today, and then consider a more complete way to think about value at the end of the article.

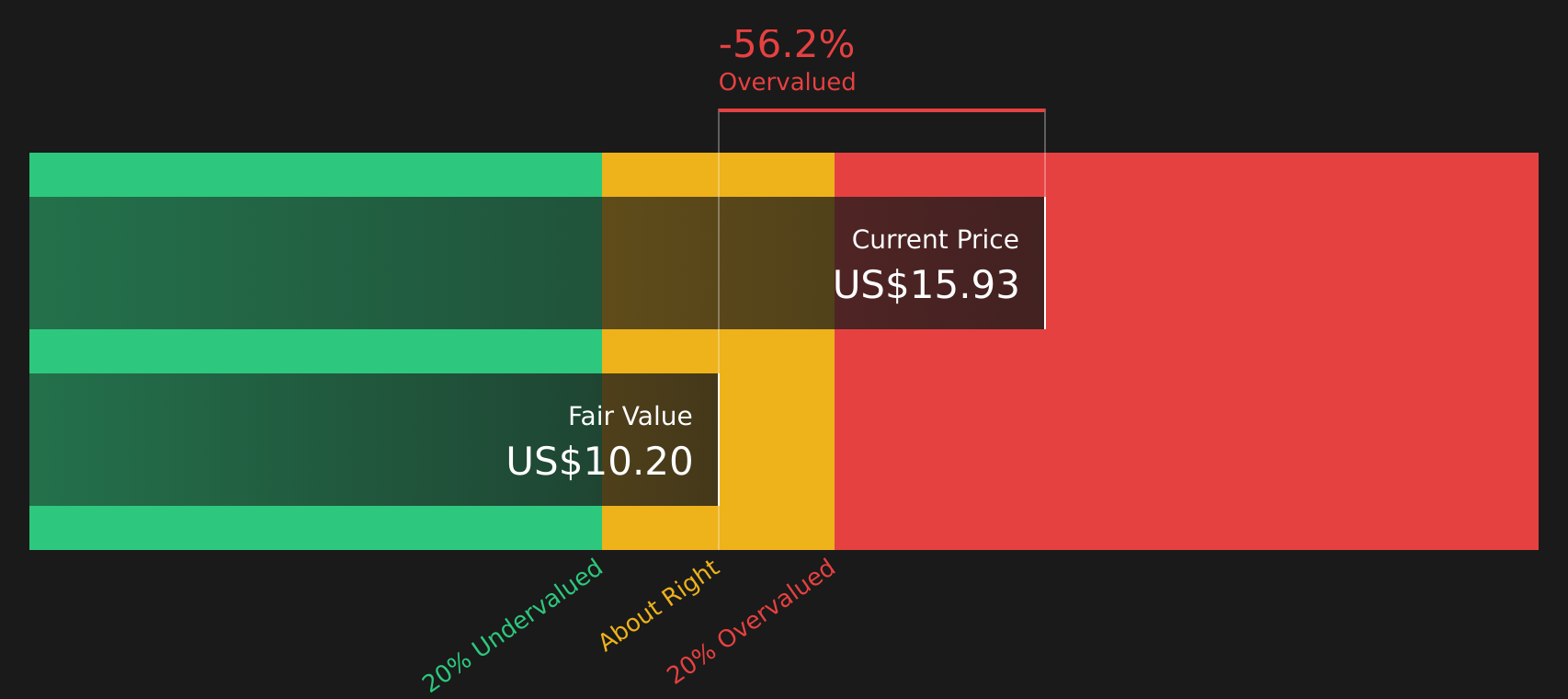

Approach 1: Klarna Group Excess Returns Analysis

The Excess Returns model looks at how much profit a company can generate above the return that shareholders require, based on its equity and earnings power. Instead of focusing on cash flows, it starts with book value per share and estimates how efficiently that equity is used over time.

For Klarna Group, book value is $6.64 per share, rising to an estimated stable book value of $8.32 per share, based on forecasts from 5 analysts. The model uses a stable EPS of $0.82 per share, sourced from weighted future Return on Equity estimates from 4 analysts, against a cost of equity of $0.68 per share. That gap, an excess return of $0.14 per share, reflects the value created above shareholders’ required return. The average Return on Equity input in the model is 9.88%.

Running these assumptions through the Excess Returns framework gives an intrinsic value of about $11.43 per share. Compared with the current share price of $15.17, the model implies Klarna Group is about 32.7% overvalued on this basis.

Result: OVERVALUED

Our Excess Returns analysis suggests Klarna Group may be overvalued by 32.7%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

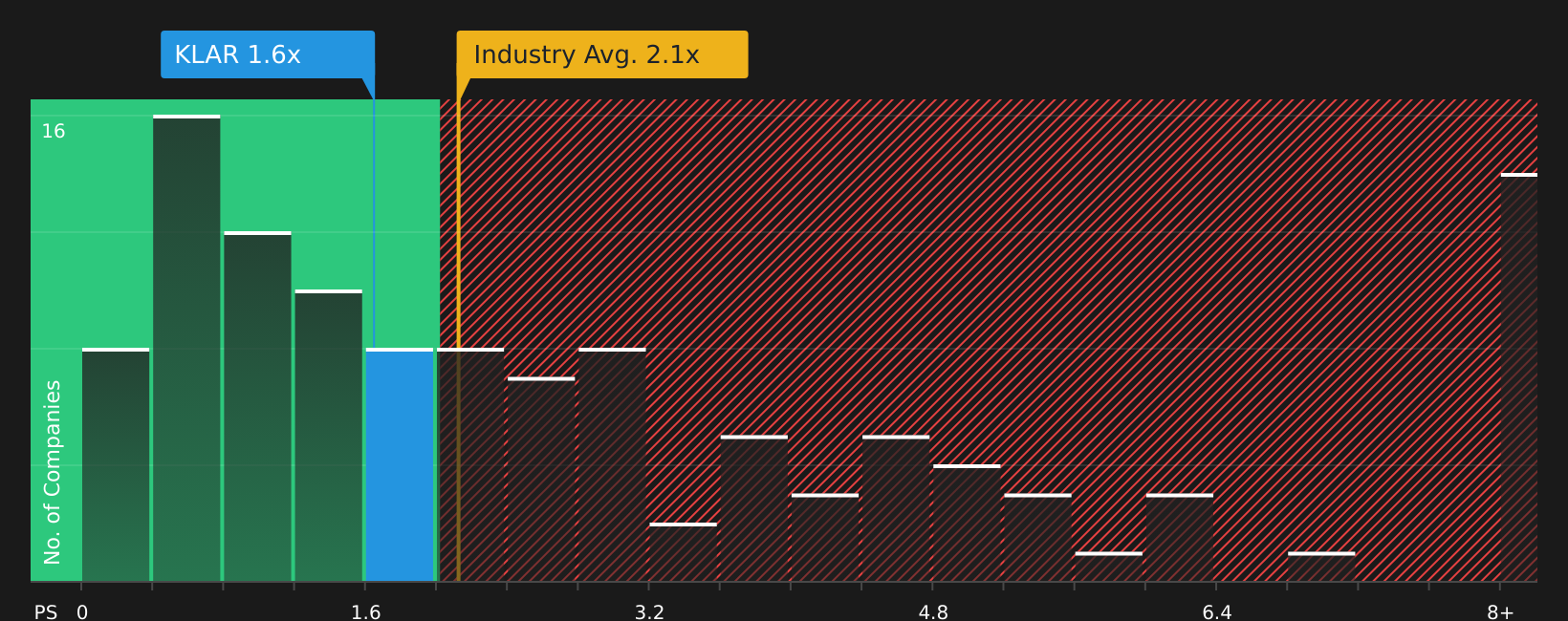

Approach 2: Klarna Group Price vs Sales

For companies where earnings are less reliable or currently limited, the P/S ratio can be a useful way to compare what investors are paying for each dollar of revenue. It side steps short term earnings noise and focuses on how the market values the top line.

Growth expectations and perceived risk usually drive what counts as a “normal” or “fair” P/S ratio. Stronger growth and lower risk often justify a higher multiple, while slower growth or higher risk tend to point to a lower one.

Klarna Group is trading on a P/S of 1.63x. This is below the Diversified Financial industry average of 2.08x and also below the peer average of 2.00x. Simply Wall St’s Fair Ratio for Klarna Group is 2.46x, which is a proprietary estimate of the P/S multiple that might be expected given factors such as earnings growth, profit margins, industry, market cap and key risks.

This Fair Ratio can be more informative than a straight comparison with peers or the sector, because it adjusts for company specific attributes instead of treating all stocks as if they were identical. Compared with the current P/S of 1.63x, the Fair Ratio of 2.46x suggests Klarna Group looks undervalued on this measure.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Klarna Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring this to life by letting you attach a clear story about Klarna Group to your own numbers, linking your view of its future revenue, earnings and margins to a forecast and then to a fair value that you can compare with today’s share price.

On Simply Wall St’s Community page, you can pick or build a Narrative in a few clicks, then see how your assumed fair value stacks up against the current price to help you decide whether Klarna Group looks more like a buy, a hold or a sell for your situation. That view automatically refreshes when new results or news are added.

For example, one Klarna Group Narrative currently points to a fair value of US$14.00 while another points to US$50.00. Two investors can look at the same company, plug in different assumptions about growth, margins and P/E, and end up with very different but clearly explained valuation stories that they can revisit as the facts change.

For Klarna Group however we will make it really easy for you with previews of two leading Klarna Group Narratives:

Fair value in this bullish narrative: US$43.01 per share.

Implied discount to this fair value at US$15.17: about 64.7%.

Revenue growth assumption in this narrative: 19.32%.

- Klarna Group is framed as solving a timing gap between when consumers want to spend and when they get paid, using small, focused loans and flexible payment plans.

- The author highlights installment payments as a way for shoppers to manage cash flow while merchants benefit from higher conversion rates.

- The narrative treats Klarna Group as building toward a broader digital banking and shopping assistant platform, with the view that the current share price sits well below the US$43.01 fair value.

Fair value in this bearish narrative: US$14.00 per share.

Implied premium to this fair value at US$15.17: about 8.4%.

Revenue growth assumption in this narrative: 21.21%.

- The bearish author focuses on how heavier use of Fair Financing and other interest bearing products can keep reported earnings and transaction margins volatile because revenue is recognized later while provisions are booked upfront.

- There is attention on funding costs, credit quality and operating efficiency, with the view that ongoing investment in banking products and U.S. expansion could limit how much margins widen.

- The narrative anchors on a US$14.00 fair value that sits within the lower end of analyst targets, encouraging investors to test those assumptions against their own expectations for revenue, margins and credit risk.

Do you think there's more to the story for Klarna Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.