Is Mastercard (MA) Offering A Chance After Recent Share Price Weakness?

Mastercard MA | 0.00 |

- If you are wondering whether Mastercard is priced fairly or if the recent weakness has opened a window of opportunity, this breakdown will help you see what the current share price actually implies.

- After a strong multi year run, with a 48.5% return over 3 years and 38.5% over 5 years, the stock is currently below its recent levels, with a 1.8% decline over 7 days, 6.2% over 30 days and 8.6% year to date, leaving it 1.5% lower over the past year.

- Recent attention on Mastercard has focused on ongoing developments in digital payments and competition with other global card networks, which continues to keep the stock in the spotlight. At the same time, investors have been weighing broader payment trends and regulatory discussions that can influence sentiment toward large payment networks.

- Right now, Mastercard scores 2 out of 6 on our valuation checks, as shown in our valuation score. The key question is what each method is actually telling you about the current price, and whether a more complete way of thinking about value, which we will come to at the end, gives you a clearer picture.

Mastercard scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Mastercard Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to earn above the return that shareholders require, then capitalizes those extra profits into a per share value.

For Mastercard, the starting point is a Book Value of $8.65 per share and a Stable Book Value estimate of $14.48 per share, based on future book value estimates from 6 analysts. On this equity base, Mastercard is expected to generate Stable EPS of $25.10 per share, sourced from weighted future return on equity estimates from 12 analysts.

The required return to equity holders, or Cost of Equity, is $1.05 per share. That implies an Excess Return of $24.05 per share, which reflects earnings above what investors are assumed to require. The average return on equity implied by these inputs is very large at about 1.7x book value.

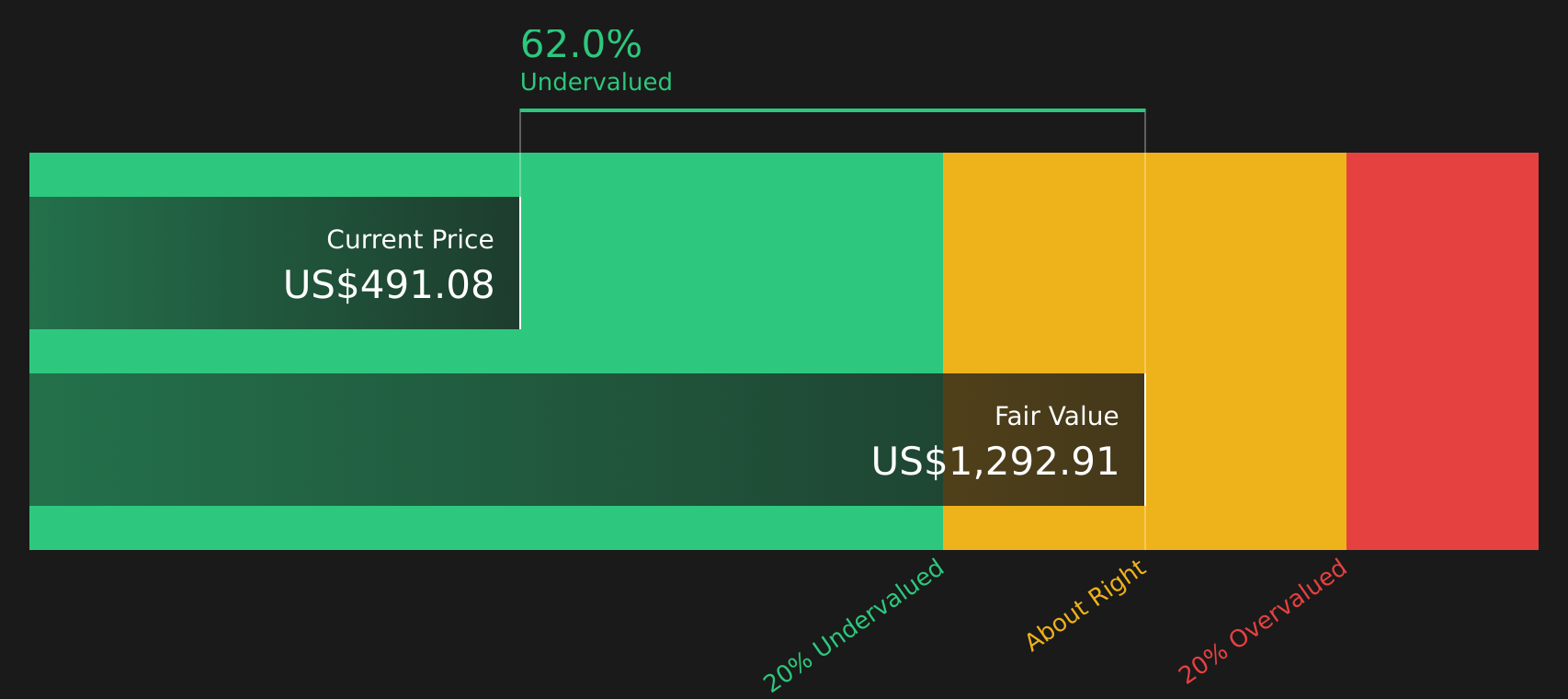

When these excess returns are projected and discounted, the model arrives at an intrinsic value of about $638.35 per share. Compared with the current share price, this implies the stock is 19.4% undervalued based on this framework.

Result: UNDERVALUED

Our Excess Returns analysis suggests Mastercard is undervalued by 19.4%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: Mastercard Price vs Earnings

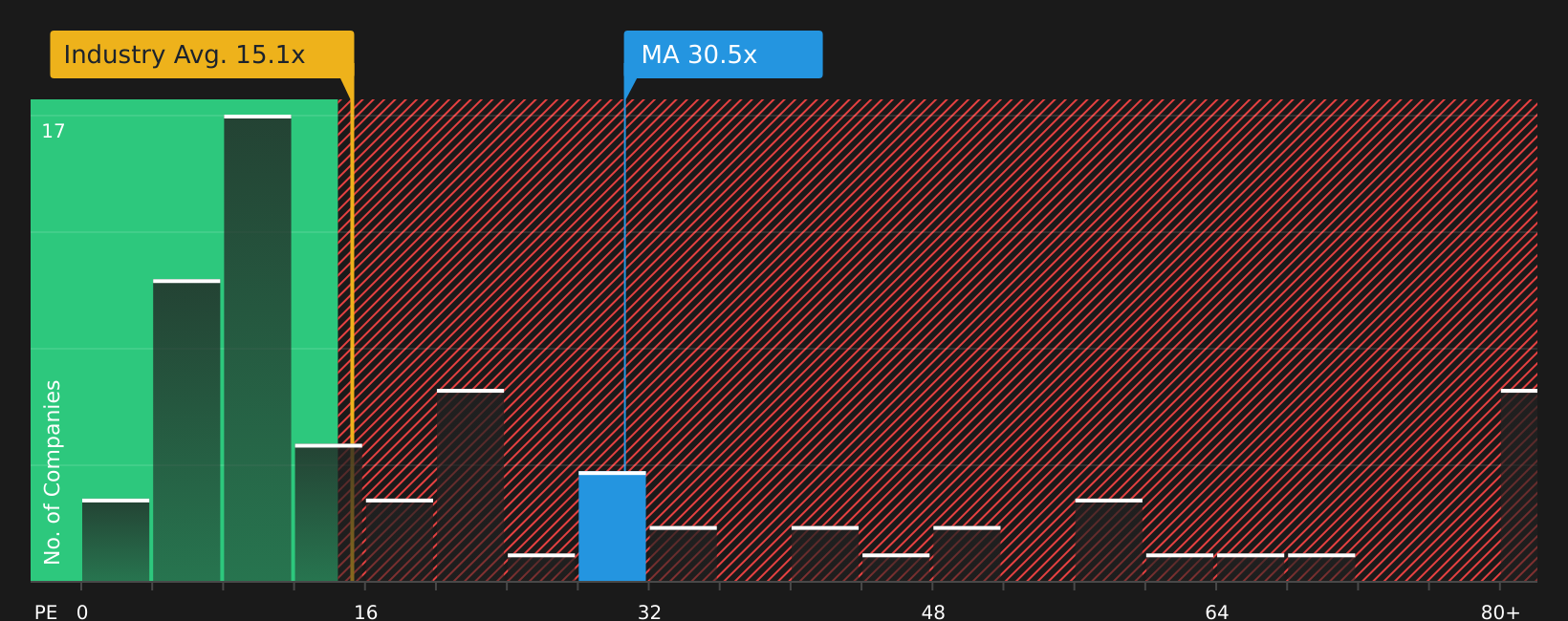

For a consistently profitable company like Mastercard, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. A higher or lower P/E often reflects what the market expects for future earnings and how risky those earnings are perceived to be, so growth expectations and business risk are key inputs into what looks like a “normal” or “fair” P/E.

Right now, Mastercard trades on a P/E of 30.67x. That sits above the Diversified Financial industry average of 17.96x and the peer average of 19.04x, so on simple comparisons the stock carries a higher earnings multiple than many of its peers.

Simply Wall St’s Fair Ratio for Mastercard, at 19.66x, is designed to be a more tailored benchmark. It incorporates factors such as earnings growth metrics, profit margins, industry classification, company size and risk indicators, rather than just comparing Mastercard with broad industry or peer group averages. Because it adjusts for these company specific drivers, the Fair Ratio can give you a more nuanced anchor for what might be a reasonable P/E range.

Comparing the Fair Ratio of 19.66x with the current P/E of 30.67x suggests Mastercard is trading above this customised earnings multiple benchmark.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Mastercard Narrative

Earlier we mentioned that there is an even better way to think about valuation. On Simply Wall St you can use Narratives, where you write the story you believe about Mastercard, link it to explicit forecasts for revenue, earnings, margins and a fair value, then see that story update automatically as new earnings or news arrive. You can compare your Fair Value to the current price to decide whether the stock fits your plan, and even see how different investors on the Community page can look at the same company in very different ways. For example, one Narrative might assume a Fair Value of about US$520.00 built on relatively modest revenue growth and a higher future P/E of 38.32x. Another Narrative might push Fair Value up to roughly US$903.41 based on stronger revenue growth and a future P/E of 39.63x. This can give you a clear sense of how your own view compares with the most cautious and most optimistic Mastercard stories in the market.

Do you think there's more to the story for Mastercard? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.