Is Nvidia (NVDA) Still Worth Considering After A 70% One Year Share Price Gain

NVIDIA Corporation NVDA | 0.00 |

- If you are wondering whether NVIDIA's current share price still offers value, or if most of the story is already priced in, this article focuses squarely on what you are getting for the price you pay.

- The stock recently closed at US$188.63, with returns of 6.3% over 7 days, 4.6% over 30 days, a small year to date move of a 0.1% decline, and a 70.1% return over the last year, which can change how investors think about both upside and risk.

- Recent headlines have kept NVIDIA in the spotlight around artificial intelligence infrastructure, graphics processing technology, and its role in powering data center and consumer applications. This context helps explain why sentiment around the stock continues to be active and why valuation has become such a debated topic.

- On Simply Wall St's framework, NVIDIA currently has a valuation score of 4 out of 6. The sections that follow will unpack how different methods arrive at that result and point you toward an additional way to think about what the stock might be worth by the end of the article.

Approach 1: NVIDIA Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows and discounts them back to today to estimate what the business might be worth right now. For NVIDIA, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model built on cash flow projections.

The latest twelve month free cash flow is reported at about $97.2b. Analyst inputs and subsequent extrapolations feed into ten year projections, with free cash flow for 2031 estimated at $410.2b and discounted to $225.6b in today’s terms. Each year in between is also discounted, then summed to arrive at an equity value per share.

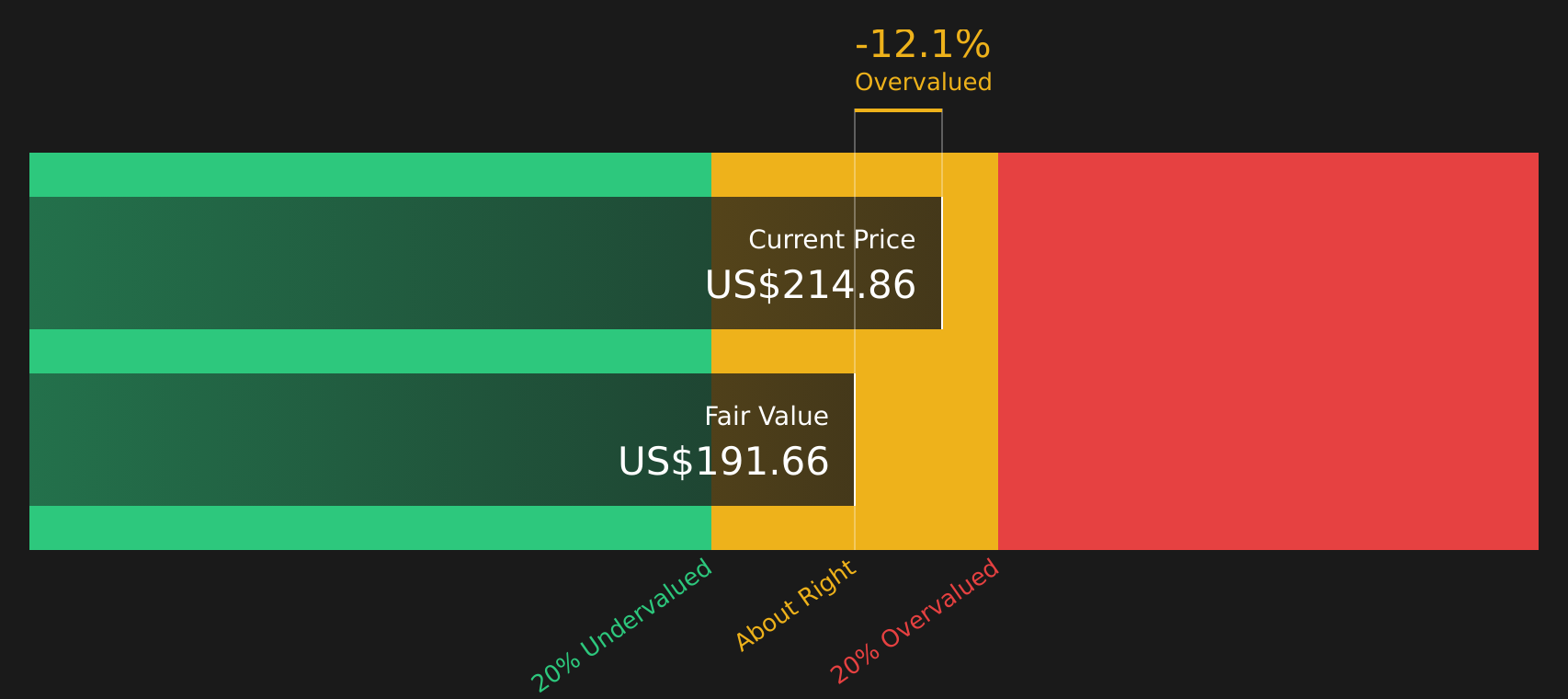

Under this framework, the estimated intrinsic value for NVIDIA is US$189.06 per share. Versus the recent share price of US$188.63, this implies the stock is about 0.2% below the DCF estimate, which is effectively a very small gap.

Result: ABOUT RIGHT

NVIDIA is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: NVIDIA Price vs Earnings

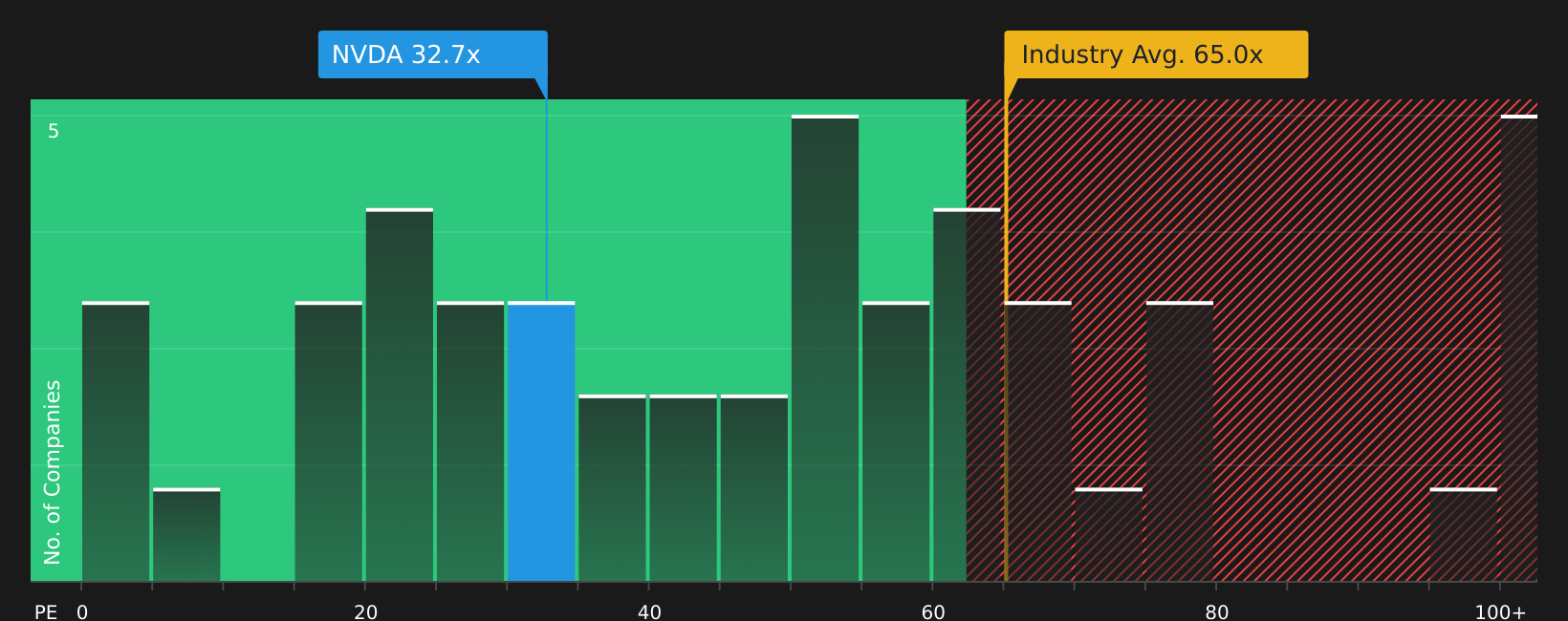

For a profitable company like NVIDIA, the P/E ratio is a useful yardstick because it links what you pay directly to the earnings the business is currently generating. The higher the expected growth and the lower the perceived risk, the more investors are often willing to pay in terms of a higher P/E multiple.

NVIDIA is currently trading on a P/E of 38.17x. The broader semiconductor industry average P/E is about 41.26x, while the peer group used here sits higher at 95.29x. On those simple comparisons, NVIDIA is below both the peer average and slightly below the sector average.

Simply Wall St also calculates a proprietary “Fair Ratio” for NVIDIA of 45.97x. This aims to estimate what a reasonable P/E could be after factoring in company specific elements such as earnings growth profile, profit margins, risk characteristics, industry classification and market cap. Because it combines these drivers into one figure, the Fair Ratio can be more tailored than a plain sector or peer comparison.

Comparing the current P/E of 38.17x with the Fair Ratio of 45.97x suggests the share price sits below that model based estimate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your NVIDIA Narrative

Earlier we mentioned that there is an even better way to understand valuation, so this is where Narratives come in, giving you a simple way to connect your view of NVIDIA’s story directly to numbers like fair value, future revenue, earnings and margins.

A Narrative is essentially your version of the NVIDIA story written in financial terms, where you spell out what you believe about AI demand, data center adoption or competition and then translate that into explicit forecasts and a fair value per share.

On Simply Wall St’s Community page, Narratives are an accessible tool that sit alongside traditional models. You can see how different assumptions drive different fair values, then compare those fair values to today’s share price to help decide whether NVIDIA looks expensive or reasonable on your terms.

These Narratives update as new information arrives. When fresh earnings guidance, export rules or product news appear, the forecasts and fair values linked to each story adjust automatically instead of staying frozen in time.

For example, one NVIDIA Narrative on the Community pegs fair value at about US$171 per share with a future P/E of 23x, another sits closer to US$305 with a future P/E near 36x, and a third is around US$90 with a future P/E of 18x. This shows how different views on AI durability, China exposure or competition can coexist and gives you a clear framework to decide which story you find most reasonable.

For NVIDIA, however, we will make it really easy for you with previews of two leading NVIDIA Narratives:

These sit on opposite sides of the fair value debate. Together they give you a helpful range to think about rather than a single answer.

Fair value in this narrative: US$268.22 per share

Gap to that fair value at the last close of US$188.63: about 29.7% below the narrative fair value

Revenue growth assumption: 37.36% a year

- Builds on a view that AI demand, data center spending and wider digitization support sustained revenue expansion for NVIDIA across multiple end markets.

- Credits the company with strong pricing power through a full stack approach that includes hardware, networking and software platforms such as CUDA and TensorRT.

- Recognizes material risks around geopolitics, customer vertical integration, supply chain capacity, power constraints and rising costs, but still arrives at a higher fair value estimate.

Fair value in this narrative: US$141.74 per share

Gap to that fair value at the last close of US$188.63: about 33.1% above the narrative fair value

Revenue growth assumption: 17.2% a year

- Sees NVIDIA as a key player across data centers, gaming, automotive and professional visualization, but questions how long current hardware leadership and pricing power can last.

- Assumes healthy but more moderate long term growth, with net margins settling at 40% and a 60x future P/E to reflect strong earnings but also rising competition.

- Highlights risks from rival GPU vendors, consumer pricing sensitivities, regulatory scrutiny on deals and potential supply chain disruptions that could cap upside from today’s price.

Taken together, these two Narratives frame NVIDIA’s valuation debate around what you believe about long term AI demand, competitive pressure and the level of earnings multiple you are comfortable with at today’s share price.

If you want to see how other investors connect their NVIDIA stories to specific numbers, have a look at the wider range of community views and track how they evolve over time, then use that range as a cross check on your own assumptions. See what the community is saying about NVIDIA

Do you think there's more to the story for NVIDIA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.