Is Oracle (ORCL) Offering Value After Recent AI Cloud Momentum And Mixed Share Performance?

Oracle Corporation ORCL | 0.00 |

- If you are wondering whether Oracle at US$185.35 is offering fair value or stretching expectations, the recent share performance gives you a useful starting signal.

- The stock has returned 11.7% over the past week, 26.6% over the last 30 days, 26.7% over 1 year and 155.3% over 5 years, with year to date performance at a 5.3% decline.

- Recent headlines have focused on Oracle's role in software and cloud infrastructure, along with its positioning within large scale enterprise IT projects. This backdrop helps frame why the stock's strong multi year returns sit alongside a weaker year to date showing, with sentiment shifting between long term growth expectations and short term caution.

- On Simply Wall St's valuation checks, Oracle scores 4 out of 6 for being undervalued. This sets up a closer look at P/E, DCF and peer comparisons next, and a different, more narrative driven way to think about valuation at the end of this article.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company's future cash flows and then discounts them back to today to arrive at an intrinsic value per share in today's dollars.

For Oracle, the Simply Wall St model uses a 2 stage Free Cash Flow to Equity approach. On a last twelve month basis, free cash flow stands at a loss of about $2.2b, and the analyst and extrapolated projections in the model move from negative free cash flow in the earlier forecast years to a projected positive free cash flow of about $31.2b by 2030.

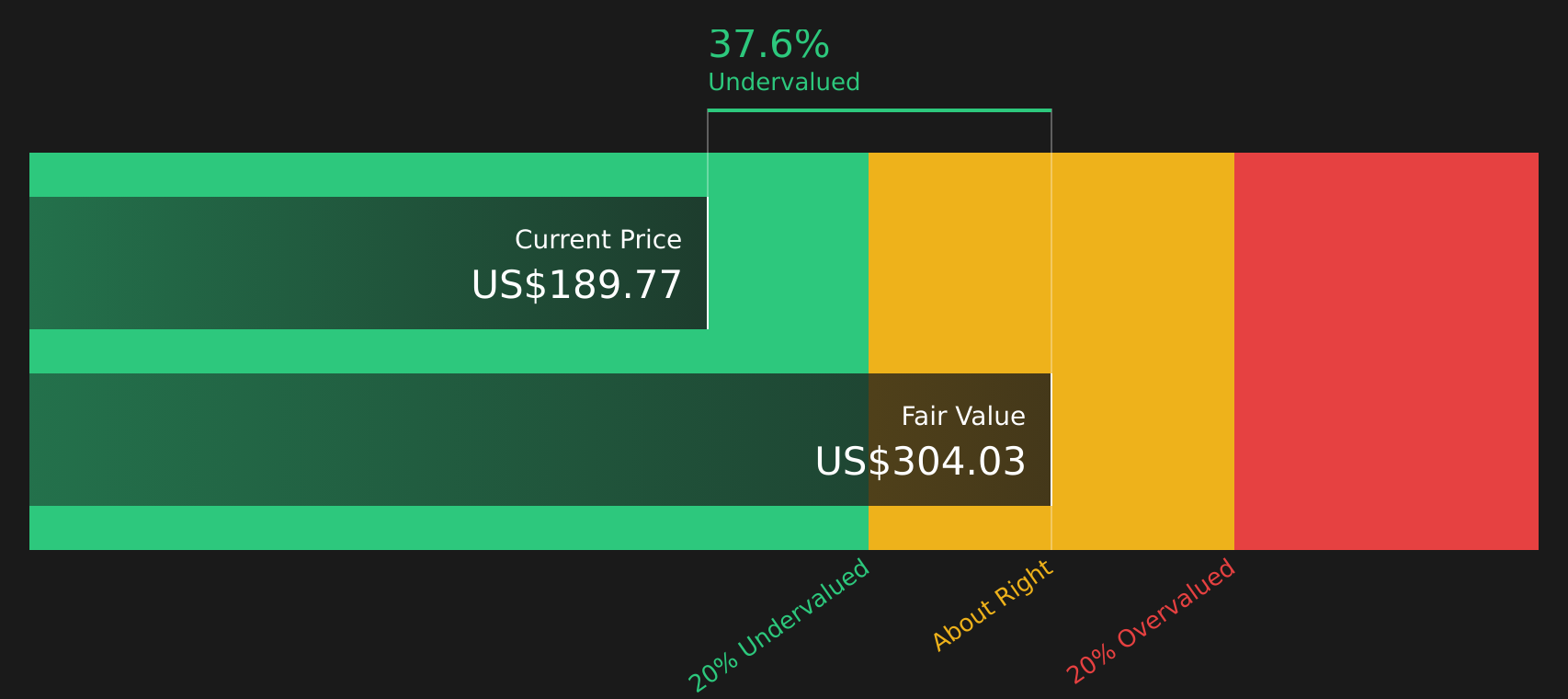

The discounted values of these projected cash flows, combined with an estimate for cash flows beyond the 10 year window, result in an intrinsic value estimate of about $300.06 per share. Compared with the recent share price of around $185.35, the model implies a 38.2% discount, which points to the stock trading below this DCF based estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle is undervalued by 38.2%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Oracle Price vs Earnings

For profitable companies, the P/E ratio is a useful way to connect what you pay for each share with the earnings that each share generates. It quickly tells you how many dollars investors are willing to pay today for one dollar of current earnings.

What counts as a normal or fair P/E depends on how investors view a company's growth outlook and risk profile. Higher expected earnings growth or lower perceived risk can justify a higher P/E, while slower expected growth or higher risk typically lines up with a lower P/E.

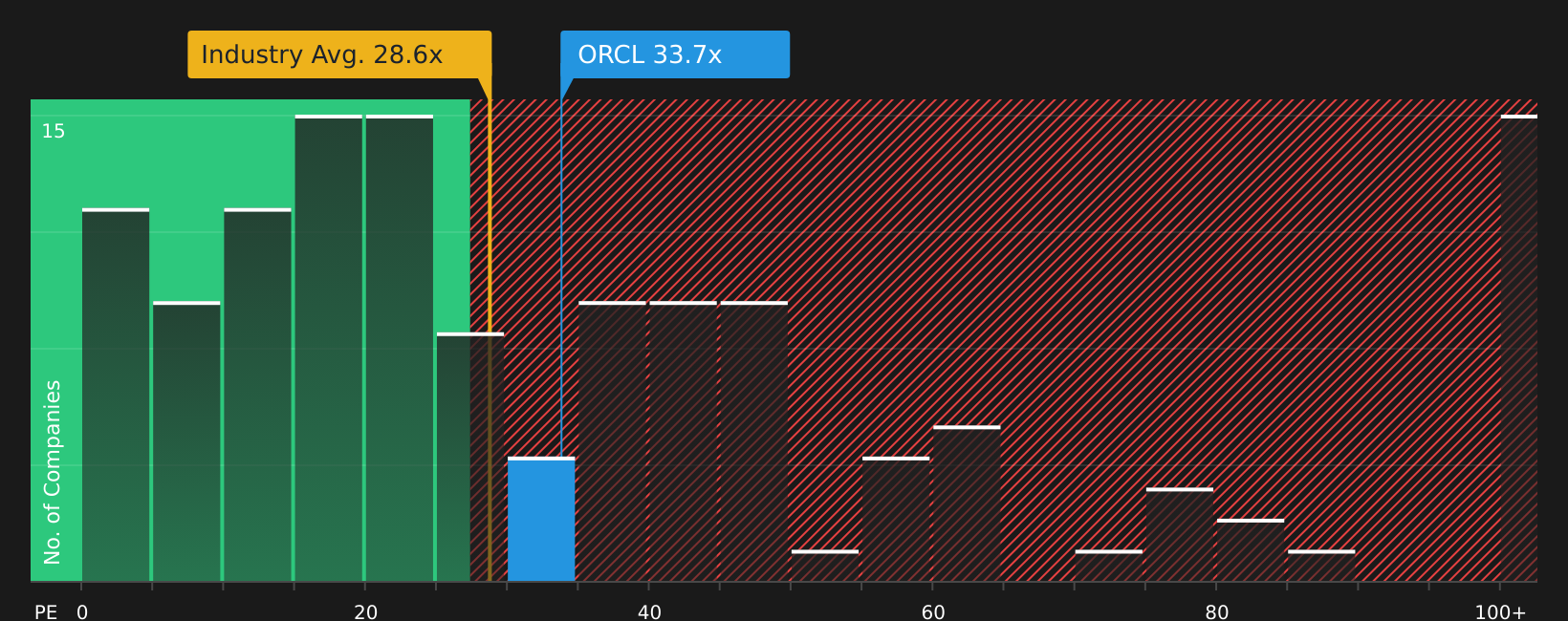

Oracle currently trades on a P/E of 32.93x, compared with the Software industry average of 30.41x and a peer average of 57.58x. Simply Wall St's Fair Ratio metric, which estimates an appropriate P/E based on factors such as earnings growth, industry, profit margin, market cap and risks, sits higher at 60.64x.

This Fair Ratio is more tailored than a simple industry or peer comparison because it adjusts for Oracle's specific characteristics rather than assuming all software stocks deserve similar multiples.

Since the Fair Ratio of 60.64x is well above the current P/E of 32.93x, the multiple based view suggests the stock is trading below this Fair Ratio estimate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story to your numbers by tying your view of Oracle’s business, revenue, earnings and margins into a forecast that rolls up into a Fair Value and compares it with the current share price to help you think about buy or sell decisions. The narrative then updates automatically as new news or earnings arrive. As Oracle’s Community page shows, narratives can range from a more cautious view that centers on a Fair Value near US$120 and slower revenue growth, to an optimistic view that uses revenue growth above 30%, different margin and P/E assumptions and a Fair Value near US$360, all in a simple, accessible format used by millions of investors.

For Oracle, however, we will make it really easy for you with previews of two leading Oracle Narratives:

Think of these as two bookends for what the stock could be worth under very different assumptions, rather than hard predictions of where it will go.

On Simply Wall St, these narratives are built from explicit forecasts for revenue, profit margins, valuation multiples and discount rates, then rolled into a Fair Value that you can compare with the current share price. Your job is to decide which story feels closer to what you believe and whether you sit somewhere in between.

Fair Value: US$389.81 per share

Gap to current price: about 52.5% below this Fair Value using the community narrative model

Revenue growth assumption: 28%

- Sees Oracle as a key infrastructure partner for heavy AI workloads, with OpenAI and very large supercluster projects as proof points that its cloud and data center build out is gaining traction.

- Highlights a very large contracted backlog and strong interest in AI inference workloads, with Oracle's "whole stack" of infrastructure, database and applications viewed as a way to deepen customer spend.

- Flags execution and supply constraints, market skepticism and high AI project failure rates as real risks, but still frames the overall story as one where Oracle's AI positioning could justify a much higher valuation over time.

Fair Value: US$155.00 per share

Gap to current price: about 19.6% above this Fair Value using the analyst bear case

Revenue growth assumption: 24.4%

- Focuses on pressure from more open and interoperable cloud platforms, tighter regulation and legacy software headwinds, which could weigh on pricing power and margins even if revenue grows.

- Builds in shrinking profit margins, higher compliance and capital spending needs and potential cloud commoditization, with concern that AI and cloud contracts may not fully offset legacy declines over time.

- Uses a Fair Value of US$155 based on lower margin and risk adjusted assumptions from the bearish end of analyst forecasts, while acknowledging that strong remaining performance obligations, AI database offerings and bundled cloud plus software deals could challenge this cautious view.

These two narratives frame a wide but clearly defined range for what Oracle might be worth using different inputs, so you can sense check where your own expectations on growth, margins and risk really sit.

If you want to see the full, live versions of these narratives, including every assumption that flows into the Fair Value, you can read them in detail and compare them side by side using the community narrative tools on Simply Wall St, starting with See what the community is saying about Oracle.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.