Is Oracle (ORCL) Still Attractive After Its Strong Multi Year Share Price Run?

Oracle Corporation ORCL | 0.00 |

Before you decide whether Oracle stock looks attractively priced or stretched, it helps to line up the recent share performance with what the current valuation actually reflects.

Oracle shares recently closed at US$188.16, with the price slipping 0.8% over the past week, rising 6.0% over the last 30 days, declining 3.9% year to date, and up 20.9% over the past year, alongside very large gains of 98.3% over three years and 154.0% over five years.

Recent headlines around Oracle have kept the stock in focus, including ongoing attention on its role in large scale software and cloud infrastructure, as well as recurring discussion of how established software providers fit into broader market themes. Together, these storylines help frame why expectations and risk perceptions around the stock may have shifted over time.

On Simply Wall St's valuation checks, Oracle records a score of 4 out of 6. This suggests that some metrics screen as undervalued while others do not. The next step is to unpack how different valuation methods assess the stock and then look at an even more holistic way to think about value at the end of this article.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, takes projected future cash flows and discounts them back to today, aiming to estimate what the entire business might be worth right now in cash terms.

For Oracle, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in US$. The latest twelve month free cash flow shows an outflow of about US$2.2b, and the ten year path in the model includes several years of projected outflows before shifting to inflows. By 2030, the projection used in the model reaches free cash flow of about US$31.2b, with later years extrapolated by Simply Wall St beyond the available analyst estimates.

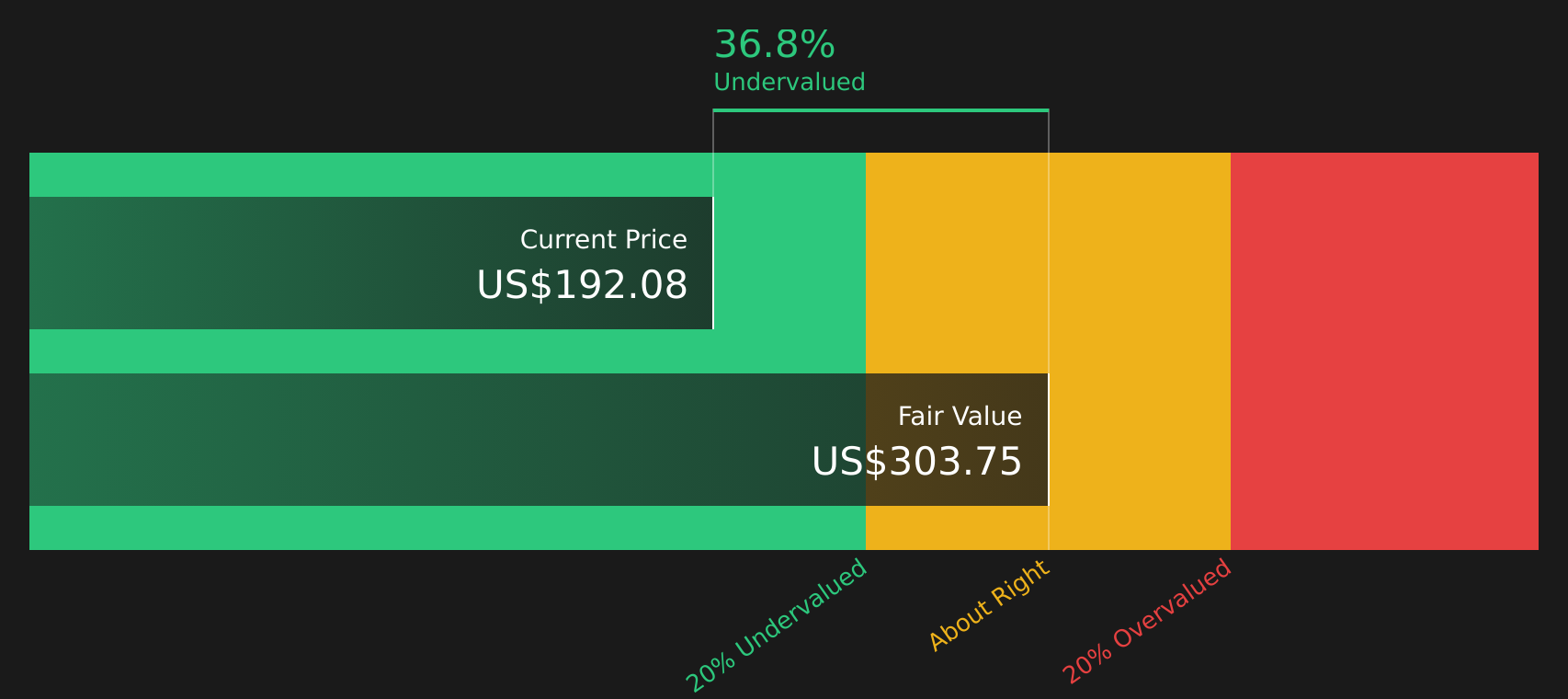

Putting those projected cash flows together and discounting them back to today gives an estimated intrinsic value of about US$302.53 per share. Compared to the recent share price of US$188.16, this implies a DCF discount of 37.8%, suggesting the stock screens as undervalued using this method alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle is undervalued by 37.8%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

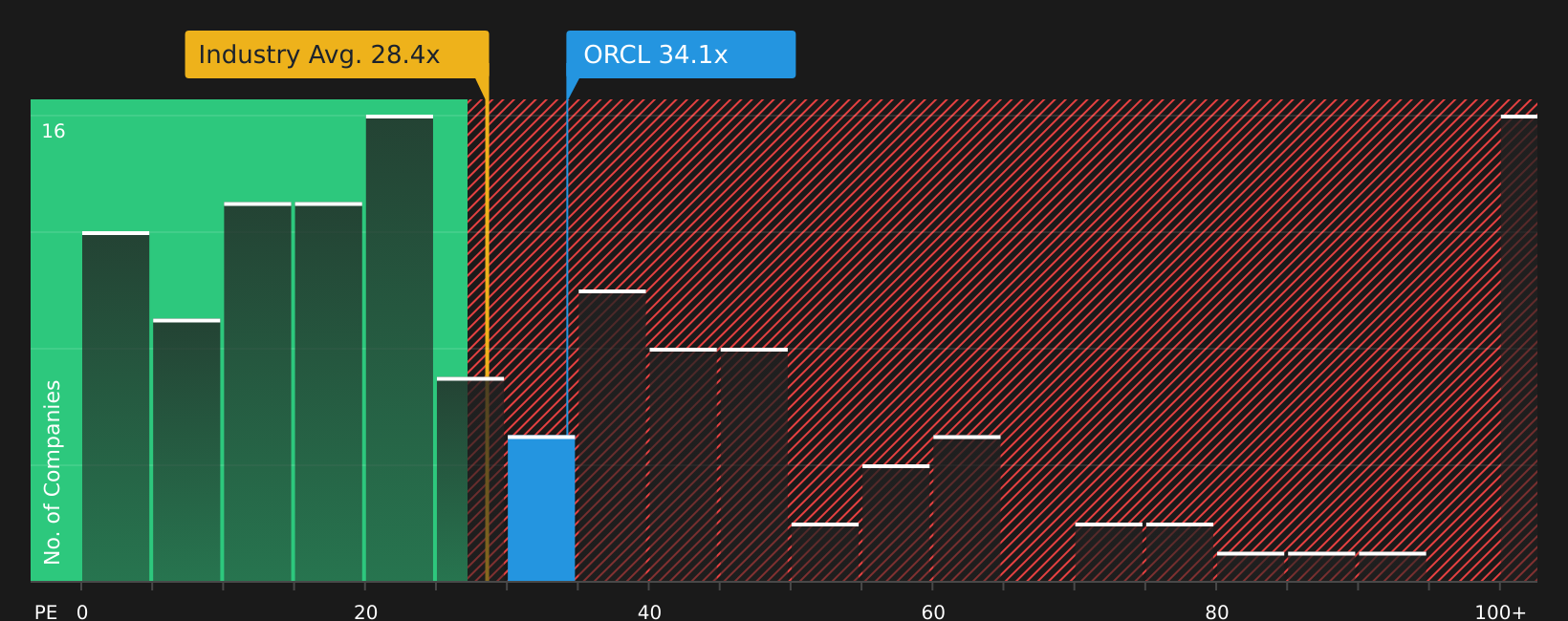

Approach 2: Oracle Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it connects what you pay for the stock to the earnings the business is currently generating. It gives you a quick sense of how many dollars investors are willing to pay for each dollar of earnings.

What counts as a "normal" P/E depends on how the market views a company’s growth prospects and risk. Higher expected earnings growth or lower perceived risk can support a higher P/E, while slower growth or higher risk usually point to a lower, more conservative multiple.

Oracle currently trades on a P/E of 33.43x. That sits above the Software industry average P/E of 27.72x, but below the peer group average of 72.60x. Simply Wall St’s Fair Ratio for Oracle is 60.92x. This is a proprietary estimate of what P/E might be appropriate after accounting for factors such as earnings growth, profit margins, industry, market cap and key risks.

This Fair Ratio can be more informative than a simple comparison with peers or the broad industry because it aims to match the multiple to Oracle’s own profile rather than to generic averages.

With the current P/E of 33.43x sitting below the Fair Ratio of 60.92x, the stock screens as undervalued using this approach.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in, giving you a clear story that links your view of Oracle’s business to a financial forecast and then to a Fair Value you can compare with today’s share price.

A Narrative on Simply Wall St is your own Oracle story written in numbers and words, where you set assumptions for future revenue, earnings and margins, explain the reasoning behind them, and see the Fair Value that flows from that view all in one place on the Community page used by millions of investors.

Because Narratives tie the story directly to a live forecast, you can quickly see whether your Fair Value suggests the stock looks cheap or expensive versus the current price, and that comparison can then guide your decision about when to buy, hold or sell without needing to build a spreadsheet.

Narratives also update automatically when new information such as news or earnings is added to the platform, so your Fair Value is refreshed without you needing to recalculate everything by hand.

For Oracle specifically, one investor might build a cautious Narrative around a Fair Value near US$119.97, while another might use more optimistic assumptions that point to a Fair Value closer to US$389.81. Seeing those side by side may help you decide which story feels closer to your own view.

For Oracle, however, we will make it really easy for you with previews of two leading Oracle Narratives:

These are live examples of how investors are connecting their assumptions about the business to a Fair Value that can be set against the current share price.

Start by asking which version of the Oracle story feels closer to your own view, and then use that as a jumping off point to refine your numbers.

Fair Value: US$389.81

Implied discount to Fair Value vs. last close of US$188.16: about 52% undervalued

Revenue growth used in this Narrative: 28%

- Frames Oracle as an AI infrastructure partner with large scale superclusters, a deep OpenAI relationship, and very large capacity build outs aimed at intensive AI workloads.

- Highlights a contract backlog that has grown rapidly, with Remaining Performance Obligations and large IaaS deals used as evidence of durable demand for Oracle Cloud Infrastructure and AI services.

- Emphasizes the "One Oracle" stack across infrastructure, database, and applications. Customers using multiple pillars are described as spending far more. The narrative also flags execution, supply, and AI project risks.

Fair Value: US$155.00

Implied premium to Fair Value vs. last close of US$188.16: about 21% overvalued

Revenue growth used in this Narrative: 24.40%

- Focuses on pressure from more open and interoperable cloud options, regulatory complexity, and cloud commoditization as potential headwinds for Oracle’s pricing power and margins over time.

- Builds a cautious earnings path that assumes shrinking profit margins, higher capital intensity, and the possibility that fast growing cloud contracts may not fully offset weakness in older on premise revenue.

- Uses a Fair Value of US$155 that sits toward the lower end of analyst targets. It encourages you to test whether the implied revenue, earnings, and P/E assumptions match your own expectations for Oracle.

If neither of these stories quite matches your view, you can adjust the growth, margin, and risk assumptions to create your own Fair Value and see how it lines up with the current share price.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.