Is Tesla (TSLA) Trading At Too High A Premium After Q2 Deliveries?

Tesla Motors, Inc. TSLA | 0.00 |

Tesla stock has delivered a strong 79.7% return over the past five years. However, recent valuation checks and market concerns around margins and future technology execution suggest the current price may be demanding for new buyers.

- Over the past five years, Tesla has returned 79.7%. This indicates that a substantial amount of anticipated future growth and cash flow may already be reflected in the share price.

- Record vehicle deliveries, expanding energy projects and AI related initiatives can support long term revenue expectations. At the same time, pressure on automotive profit margins and ongoing safety and regulatory investigations may limit how much investors are willing to pay for that story.

- Tesla scores 0 out of 6 on our broader valuation checks, which suggests that overall it leans expensive rather than looking like a clear bargain 0/6.

The key question for investors is whether Tesla’s recent share price still leaves enough potential reward to compensate for the valuation and execution risks surrounding the company.

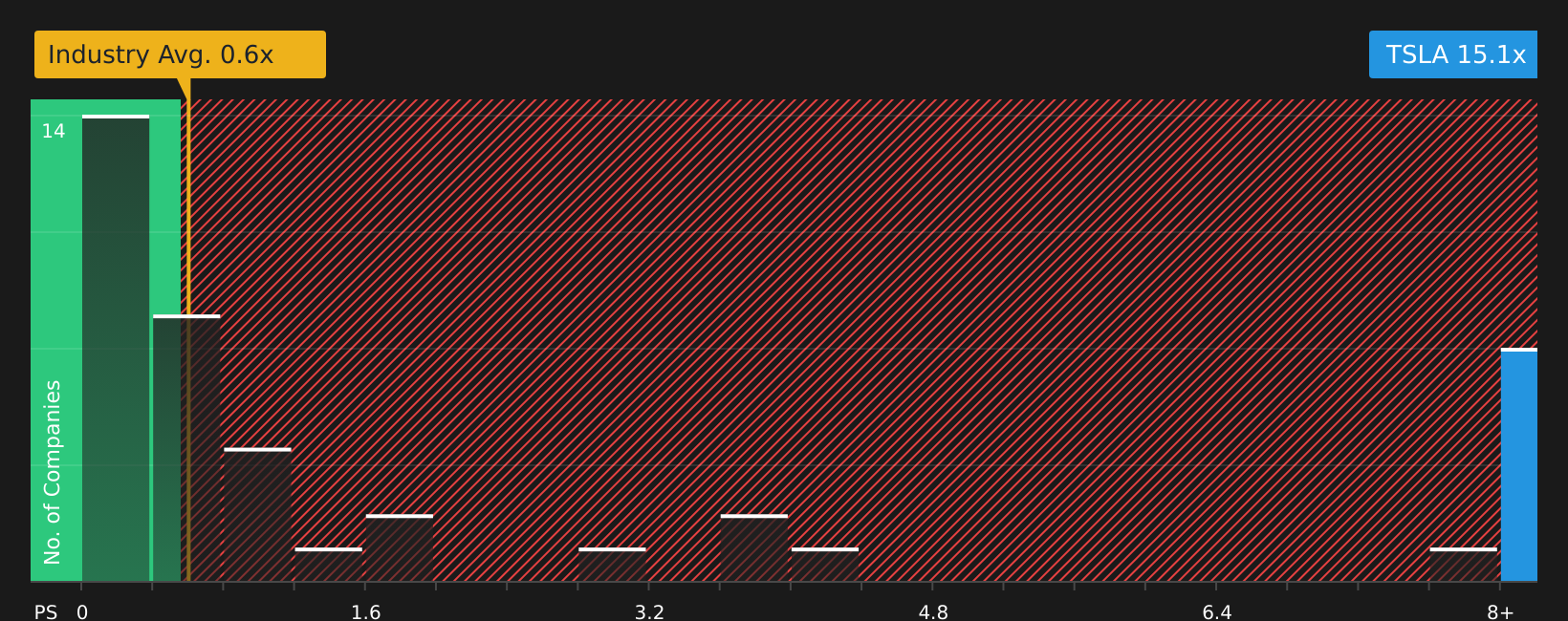

Has Tesla Run Too Far on Sales?

The P/S ratio is a useful way to look at Tesla because much of the debate is about what investors are willing to pay for its current revenue rather than its near term earnings.

Tesla trades on a P/S of 15.1x, compared with an auto industry average of 0.6x and a peer average of 1.4x. The fair P/S ratio from the model is 3.3x, so the current multiple sits several turns above what would typically be implied by Tesla’s size, margins, business mix and risk profile. With such a wide gap, the model is effectively flagging that the stock is pricing in a lot of optimism relative to its fundamental drivers rather than pointing to a precise target multiple.

Despite record vehicle deliveries and expanding energy and AI stories supporting sentiment in recent months, the valuation on this sales multiple still places Tesla at a steep premium to both the sector and the model’s fair range.

On this P/S framework, Tesla stock screens as clearly overvalued.

The Tesla Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Tesla pick up where the valuation puzzle leaves off. They spell out which paths for Tesla’s growth, margins and earnings would need to play out for the stock to be worth materially more or materially less than today’s price. Each narrative connects its number to a particular view on how Tesla’s growth, profitability and risks could evolve, giving you a clear reference point to revisit as fresh information arrives on the Community page.

The Tesla community is split between those treating it as a future "Physical AI" platform and others viewing it as a stretched case study in market optimism.

Bull case: 41% undervalued

"Just as the iPhone created the App Store economy, Optimus is poised to create the "Labor Economy"..."

Bear case: 1212% overvalued

"The company’s price-to-earnings ratio sits at around 330x, it is worth pausing on what this implies..."

Do you think there's more to the story for Tesla? Head over to our Community to see what others are saying!

The Bottom Line

Tesla looks overvalued on the main market multiple framework, with an extreme gap between its current P/S ratio and what the tailored model implies for a company with its profile. That premium effectively reflects very optimistic assumptions about future revenue, margins and execution. From here, what matters most is whether Tesla can deliver the level of growth and profitability that would justify such a rich multiple, or whether expectations eventually reset closer to sector norms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.