Is Wells Fargo (WFC) Pricing Reflect Regulatory Progress And Recent Share Price Pullback Accurately

Wells Fargo & Company WFC | 0.00 |

- If you are wondering whether Wells Fargo's current share price lines up with its underlying worth, this article will walk through what the numbers suggest and where the gaps might be.

- The stock last closed at US$80.81, with returns of 1.8% over 7 days, 0.3% over 30 days, an 11.9% return over 1 year, a 128.2% return over 3 years and a 94.7% return over 5 years, while year to date the return stands at a 15.1% decline.

- Recent headlines around Wells Fargo have focused on ongoing regulatory oversight, internal control improvements and the bank's progress on resolving legacy issues that have shaped investor sentiment. These developments give important context for how the market is currently pricing the stock and how investors think about its risk profile.

- Simply Wall St's valuation model gives Wells Fargo a value score of 4 out of 6, which sets up a closer look at how different valuation approaches compare and why another lens on valuation, covered near the end of this article, can add an extra layer of insight.

Approach 1: Wells Fargo Excess Returns Analysis

The Excess Returns model examines how much profit Wells Fargo is expected to generate above its estimated cost of equity, then capitalises those extra returns into an implied share value. It focuses less on raw earnings and more on what the bank earns on shareholders' capital compared with what investors require as a return.

For Wells Fargo, the model uses a Book Value of US$53.21 per share and a Stable EPS estimate of US$7.89 per share, based on weighted future Return on Equity estimates from 18 analysts. The average Return on Equity is 13.23%, while the Cost of Equity is US$4.75 per share. That gap produces an Excess Return of US$3.15 per share, which is the core input to this approach.

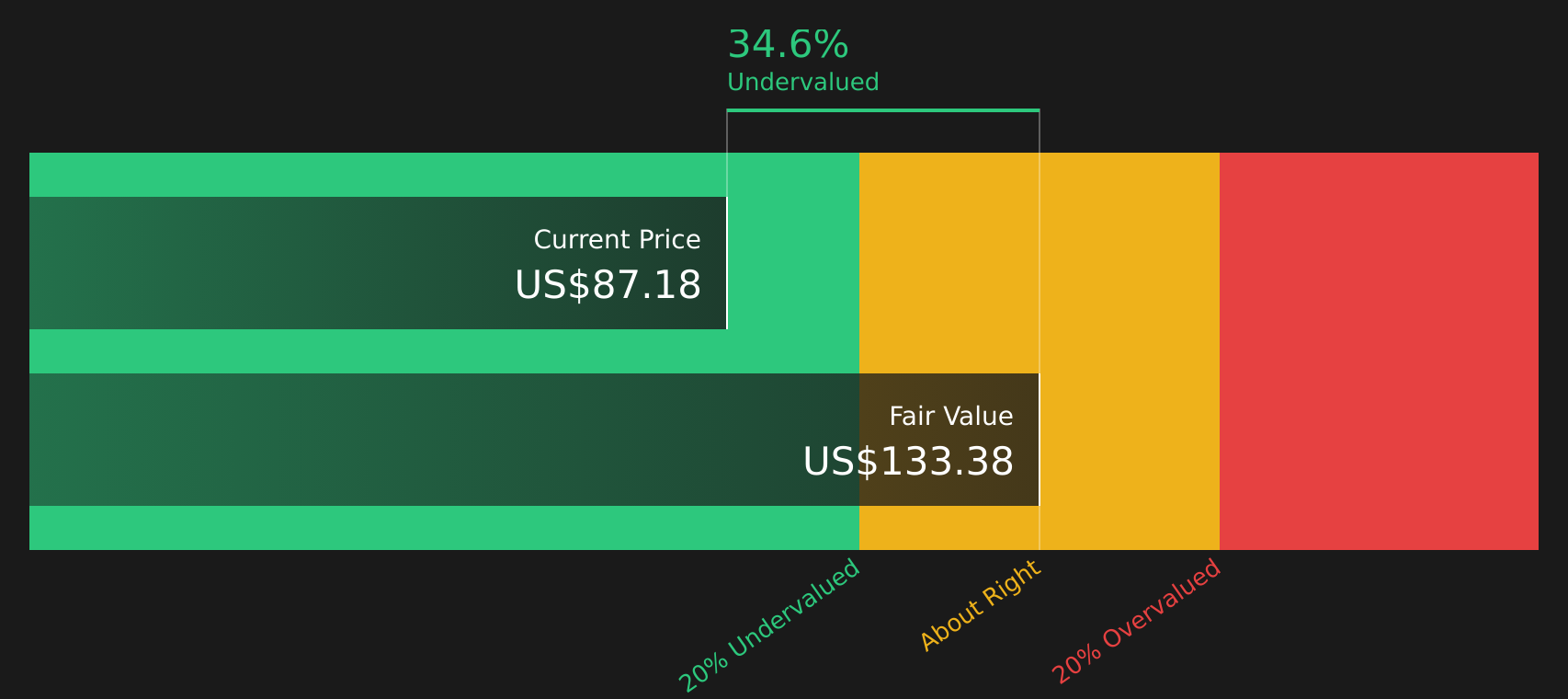

The model also assumes a Stable Book Value of US$59.67 per share, sourced from weighted future book value estimates from 15 analysts, to gauge how the capital base could support future excess returns. Using these inputs, the Excess Returns model arrives at an intrinsic value of about US$128.93 per share, which implies the shares trade at a 37.3% discount to this estimate.

Result: UNDERVALUED

Our Excess Returns analysis suggests Wells Fargo is undervalued by 37.3%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Wells Fargo Price vs Earnings

For a consistently profitable bank, the P/E ratio is a practical way to check how much you are paying for each dollar of earnings. It connects the share price directly to the bottom line, which is especially useful when earnings are a key driver of value.

What counts as a "normal" or "fair" P/E depends on how the market views a company's growth prospects and risk profile. Higher expected earnings growth or lower perceived risk can support a higher P/E, while slower expected growth or higher perceived risk usually points to a lower P/E.

Wells Fargo currently trades on a P/E of 11.96x. That is above the Banks industry average of 11.40x, but below the peer group average of 13.02x. Simply Wall St's Fair Ratio for Wells Fargo is 14.47x. This Fair Ratio is a proprietary estimate of what the P/E could be based on factors such as earnings growth, profit margins, industry, market cap and risk. Because it draws on these company specific drivers, it offers a more tailored reference point than a simple comparison with industry or peers.

Comparing the Fair Ratio of 14.47x with the current P/E of 11.96x suggests Wells Fargo trades below this model based reference.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Wells Fargo Narrative

Earlier a better way to understand valuation was mentioned. Think of a Narrative as your own Wells Fargo story that connects what you believe about its future revenue, earnings and margins to a financial forecast and a fair value. You can then compare that fair value with the current price to help you decide whether the stock looks attractive or not. This is all available within an easy to use tool on Simply Wall St's Community page that updates as news or earnings arrive. One investor can build a cautious Wells Fargo Narrative anchored to a fair value of about US$74.70, while another can build a more optimistic one at about US$96.17, and both can clearly see how their different assumptions lead to different conclusions.

For Wells Fargo however we will make it really easy for you with previews of two leading Wells Fargo Narratives:

Fair value: US$96.17

Implied discount to fair value: 15.9%

Revenue growth assumption: 6.82%

- Analysts expect revenue to reach about US$98.9b by 2029 with earnings of about US$24.3b, supported by a forecast P/E of 12.7x on those earnings.

- The thesis leans on higher balance sheet flexibility after prior regulatory caps, ongoing digital banking investment, and expansion in wealth and advisory services to support fee income.

- Risks include continued regulatory and compliance demands, competition from banks and fintechs, and uncertainty around long term interest rates and deposit costs.

Fair value: US$74.70

Implied premium to fair value: 8.2%

Revenue growth assumption: 3.0%

- This view sees fair value below the current share price, with a future P/E of 10.0x and a profit margin assumption of 28.0% leaving less headroom at today’s valuation.

- It highlights that a lower revenue growth outlook and a higher required return of 6.0% can limit upside if earnings do not track higher than expected.

- The narrative frames Wells Fargo as potentially already pricing in many positives, so investors are encouraged to weigh whether more conservative assumptions fit better with their expectations.

If you want to stress test your own view against these two starting points and see how different assumptions change the outcome, the Community tools let you build a custom Wells Fargo Narrative and compare it side by side with existing ones.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Wells Fargo on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Wells Fargo? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.