Is Zoetis (ZTS) Now An Opportunity After A 31% Five Year Share Price Drop

Zoetis, Inc. Class A ZTS | 0.00 |

- If you have been wondering whether Zoetis at around US$113.83 is starting to look attractively priced, you are not alone.

- The stock has seen a 3.1% decline over the last week, a 2.1% decline over the last month, and is down 9.6% year to date, adding to a 26.1% decline over 1 year and 33.6% over 3 years.

- These moves have come as investors reassess large pharmaceutical and animal health names in general, with sentiment shifting after changing expectations around growth and regulation. For Zoetis, that reassessment has been reflected in the share price over the past 5 years, with a 31.1% decline across that period.

- Right now, Zoetis scores 5 out of 6 on Simply Wall St's valuation checks, giving it a value score of 5. The rest of this article will break down what that means across different valuation methods, while also pointing to a more complete way to think about valuation at the end.

Approach 1: Zoetis Discounted Cash Flow (DCF) Analysis

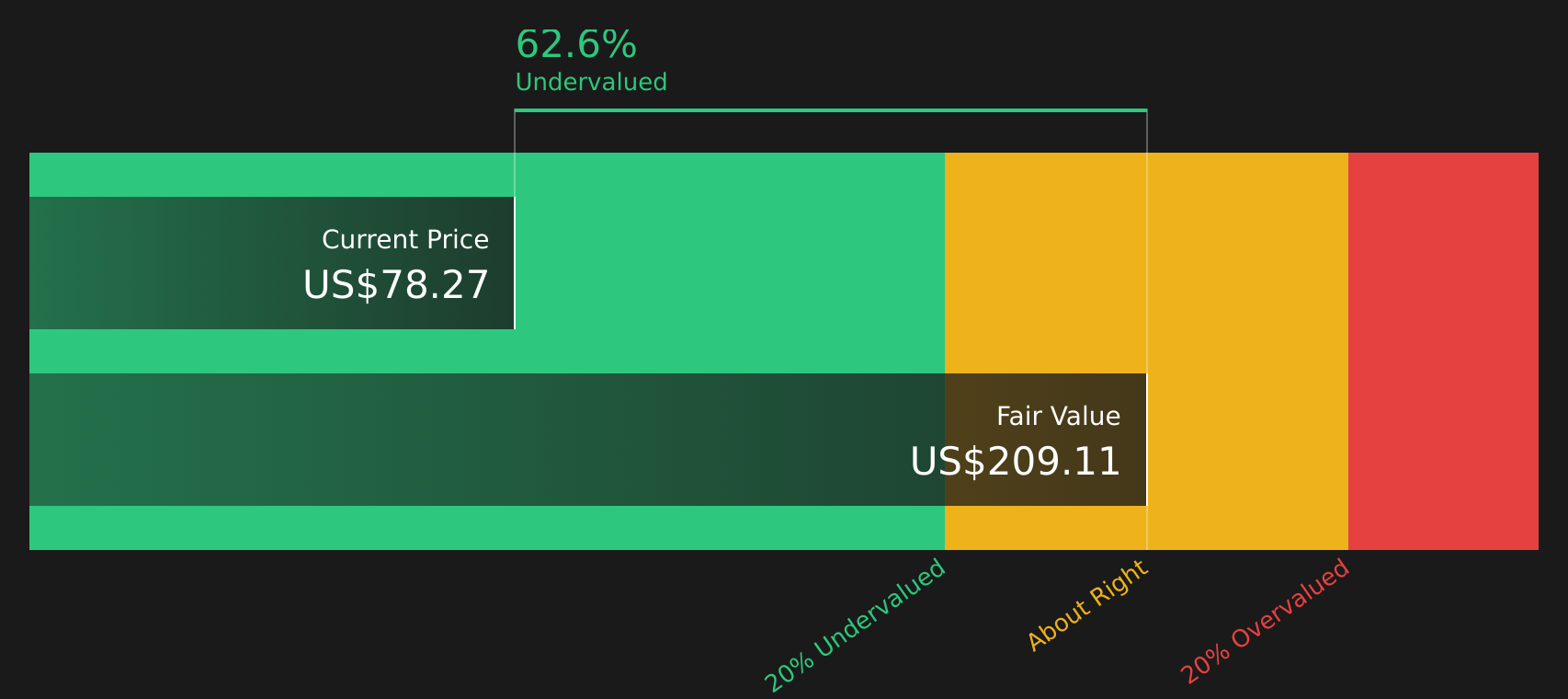

A Discounted Cash Flow, or DCF, model takes projected future cash flows and discounts them back to today using a required rate of return, aiming to estimate what those future dollars are worth in present terms.

For Zoetis, the model used is a 2 Stage Free Cash Flow to Equity approach that starts with current Free Cash Flow of about $2.21b. Analysts have supplied explicit forecasts out to 2030, with Simply Wall St extrapolating beyond the usual 5 year analyst window to create a 10 year path of cash flows that range from about $2.59b in discounted FCF in 2026 to about $2.22b in discounted FCF in 2035.

Pulling those projections together, the DCF model arrives at an estimated intrinsic value of around $212.68 per share. Compared with a share price of about $113.83, this estimate suggests the stock trades at roughly a 46.5% discount to that DCF value on this model alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Zoetis is undervalued by 46.5%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Zoetis Price vs Earnings

For a profitable company, the P/E ratio is a straightforward way to link what you pay today to the earnings the business is currently producing. It lets you see how many dollars investors are paying for each dollar of earnings.

What counts as a “normal” or “fair” P/E depends on how quickly earnings are expected to grow and how risky those earnings are. Higher expected growth and lower perceived risk usually support a higher P/E, while lower growth or higher risk tend to justify a lower one.

Zoetis currently trades on a P/E of 17.91x. That sits above the broader Pharmaceuticals industry average of 15.84x, but below the peer group average of 23.42x. Simply Wall St’s Fair Ratio framework estimates a P/E of 20.77x for Zoetis, based on factors such as earnings growth, industry, profit margins, market cap and specific risks.

This Fair Ratio is designed to be more tailored than a simple comparison with industry or peer averages because it adjusts for company specific qualities rather than treating all firms in the group as identical. Compared with this Fair Ratio of 20.77x, Zoetis’ current P/E of 17.91x suggests the shares are trading below that modelled level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Zoetis Narrative

Earlier sections used DCF and P/E to compare price and value, but Narratives let you go one step further by turning your view of Zoetis into a clear story that links assumptions about future revenue, earnings and margins to a Fair Value. This is all available in an easy tool on Simply Wall St's Community page that updates automatically as new news or earnings arrive. It helps you see, for example, how a cautious Zoetis Narrative with a Fair Value of US$127 and a more optimistic one at about US$187.59 can both be reasonable. Each investor can then compare their chosen Fair Value to the current price to decide whether the stock looks expensive, cheap or roughly in line with their expectations.

Do you think there's more to the story for Zoetis? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.