KKR (NYSE:KKR) Valuation Check As Milan Office Expansion Builds Its Italian Presence

KKR & Co KKR | 0.00 |

KKR (KKR) has announced plans to open a new office in Milan, underscoring its commitment to Italy as a key European market and supporting investment activity across Private Equity, Real Assets, Credit, and Insurance.

Recent news around the Milan office comes after a mixed period for the stock, with the share price down 7.27% over the past month and year to date share price returns down 27.05%. At the same time, the three year total shareholder return of 83.13% and five year total shareholder return of 76.45% still point to solid long term compounding.

If you are weighing KKR alongside other opportunities in finance and infrastructure, it can help to broaden your watchlist and scan 21 top founder-led companies

With KKR stock down over the past year yet still showing strong multi year shareholder returns and trading at a discount to both analyst targets and some intrinsic estimates, is this weakness an opening, or are markets already pricing in future growth?

Most Popular Narrative: 11.3% Overvalued

KKR last closed at $94.03, while the most followed narrative fair value sits at $84.45, so the story currently prices in a premium to that estimate.

Desde un enfoque Buffett puro:

KKR empieza a parecer menos un gestor de private equity y más un “compounder de capital permanente”.

Lectura final:

Valor intrínseco: ~$105–$120 por acción

Basado SOLO en negocio recurrente

Con opcionalidad no valorada

Want to understand why a long term, Buffett style framework can still call KKR overvalued even with recurring earnings and a conservative discount rate baked in.

Result: Fair Value of $84.45 (OVERVALUED)

However, this narrative could be challenged if fundraising slows meaningfully, or if a severe private credit downturn hits fee income harder than current stress tests suggest.

Another Take: DCF Points The Other Way

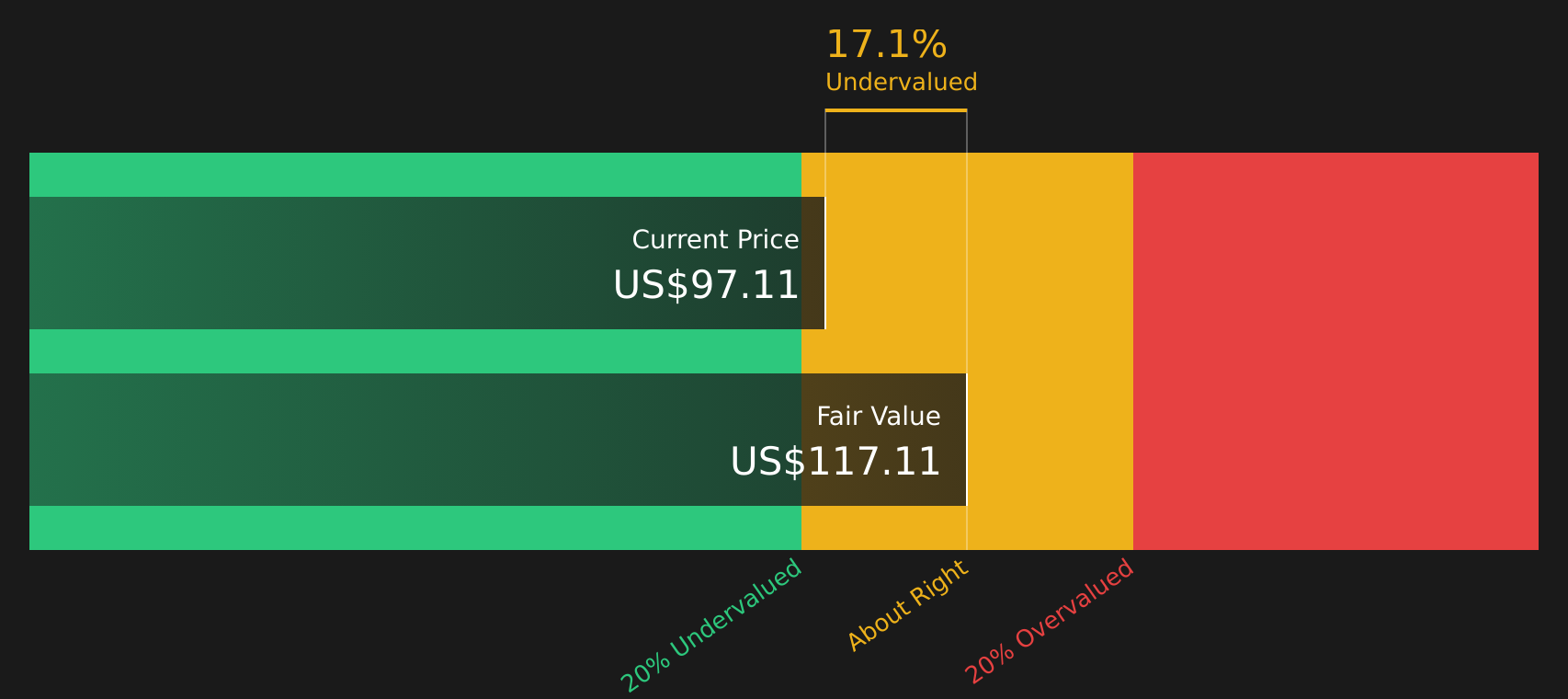

That Buffett style narrative pegs KKR as 11.3% overvalued at a fair value of $84.45, yet our DCF model tells a different story. On those cash flow assumptions, KKR at $94.03 screens at a 15.6% discount to an estimated value of $111.39. Which story do you trust more: cash flows or narrative tension?

To see how our cash flow based view is built and what would need to change for the valuation to shift, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out KKR for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After weighing two different valuation stories, it helps to go back to the numbers, test a few scenarios yourself, and decide where you stand. If you want a quick snapshot of what the current optimism is built on, take a closer look at the 3 key rewards

Ready to hunt for your next idea?

If you stop at just one stock, you risk missing opportunities that might fit your goals even better, so put a few fresh ideas on your radar.

- Target steadier compounding by checking companies that show strong financial footing with the solid balance sheet and fundamentals stocks screener (46 results)

- Spot potential mispriced opportunities early by scanning the screener containing 22 high quality undiscovered gems

- Protect your downside by focusing on companies that rank well in the 64 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.