Linde (LIN) Margin Hold At 20.3% Tests Bullish Profit Growth Narratives

Linde plc LIN | 497.94 497.94 | -0.34% 0.00% Post |

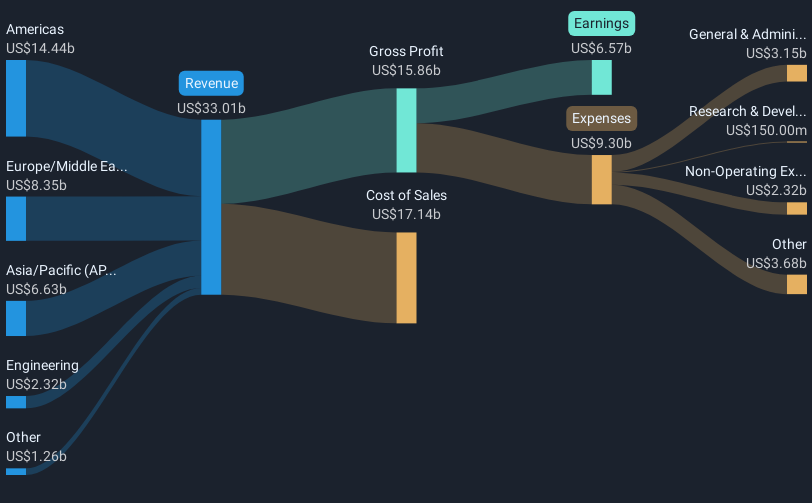

Linde (LIN) closed out FY 2025 with Q4 revenue of US$8.8b and basic EPS of US$3.28, alongside trailing twelve month revenue of US$34.0b and EPS of US$14.69 that frame a steady earnings profile through the year. The company has seen quarterly revenue range from US$8.1b to US$8.8b and basic EPS move between US$3.28 and US$4.11 across 2025, giving investors a clear view of how the topline and per share earnings have tracked into the latest print. With net profit margins at 20.3% and edging higher than a year ago, the story this season is focused on how Linde is holding its pricing power and profitability through the cycle.

See our full analysis for Linde.With the headline numbers on the table, the next step is to see how this earnings profile lines up against the key narratives investors and analysts have been using to explain Linde’s trajectory.

5.1% earnings growth on a US$34.0b base

- On a trailing twelve month basis, Linde earned US$6.9b of net income on US$34.0b of revenue, with earnings up 5.1% over the past year and a five year average earnings growth rate of 18.7% per year.

- What stands out for a more bullish view is that this 5.1% earnings growth is coming off already large profit levels. Forecasts point to earnings growing at about 9.2% per year, which supports the idea of Linde as a long term compounder even though the latest quarterly EPS bounced between US$3.28 and US$4.11 through 2025.

- Supporters can point to trailing net income of US$6.9b versus US$6.6b a year earlier as evidence that profit levels are holding up alongside that 5.1% growth rate.

- At the same time, anyone concerned about growth slowing can see that the five year 18.7% average growth rate is higher than the most recent 5.1%, which adds a bit of tension to the strongest bullish claims.

Margins at 20.3% with steady pricing

- Net profit margin sits at 20.3% on the latest trailing twelve month numbers, compared with 19.9% a year ago, on revenue that moved from US$33.0b to US$34.0b over the same period.

- Bears might argue that a premium priced industrial should be showing sharper margin expansion. Yet the move from 19.9% to 20.3% on roughly US$1.0b of extra revenue suggests Linde is maintaining strong profitability even as quarterly net income ranged between US$1.5b and US$1.9b in 2025, which softens some of the harsher bearish angles around earnings quality.

- Critics highlighting potential pressure on profitability need to weigh that margins ticked higher while quarterly revenue held between US$8.1b and US$8.8b, indicating the company kept a firm grip on per dollar profit across the year.

- On the flip side, anyone expecting a rapid margin surge can see that the change is modest rather than dramatic, so it does not fully back an aggressive bullish push on profitability either.

P/E of 30.3x and price above DCF fair value

- The shares trade at US$448.24 with a P/E of 30.3x, above the US Chemicals industry average of 24.9x but below the peer average of 38.7x, and above an indicated DCF fair value of about US$394.04, while the company also carries a high level of debt.

- What challenges a simple bullish narrative is that while supporters point to multi year earnings growth and a 20.3% net margin to justify paying more than the sector average, the fact that the current price sits above the DCF fair value and the business is described as having high debt means some of that optimism is already reflected in the valuation, even though the stock still screens cheaper than its closest peer group on P/E.

- Investors who focus on the DCF fair value can see a gap of roughly US$54 between the modelled value and the US$448.24 share price, which may be used to argue for a more cautious stance on upside from here.

- Those comparing across peers may counter that a 30.3x P/E below the 38.7x peer average leaves room relative to similar companies, yet the premium to the 24.9x industry level and the mention of high debt keep the risk and reward picture finely balanced rather than one sided.

For a fuller picture of how different investors interpret these growth, margin and valuation trade offs, it is worth reading the shared market view on Linde in more detail: 📊 Read the full Linde Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Linde's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Linde’s slower 5.1% earnings growth, a 30.3x P/E above its DCF fair value, and a high debt load may leave you questioning the risk reward trade off.

If that mix of rich pricing and leverage feels uncomfortable, you may want to quickly scan solid balance sheet and fundamentals stocks screener (45 results) to find companies where strong balance sheets help anchor the valuation story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.