MasterBrand (MBC) Valuation Check After Q4 Loss Cautious 2026 Outlook And Cost Cut Plan

MasterBrand Inc MBC | 8.57 8.57 | -1.72% 0.00% Pre |

MasterBrand (MBC) is back on investors radar after reporting a fourth quarter loss, issuing cautious 2026 guidance, and outlining $30 million in annual cost cuts, as demand and new construction markets remain under pressure.

The weak fourth quarter, cautious 2026 guidance and muted buyback activity appear to have weighed on sentiment, with a 7 day share price return of a 13.25% decline and a 1 year total shareholder return of a 30.15% loss, even though the 90 day share price return of 16.16% suggests earlier momentum had been building.

If you are reassessing your watchlist after MasterBrand's latest update, this could be a good moment to widen your search and check out 23 top founder-led companies.

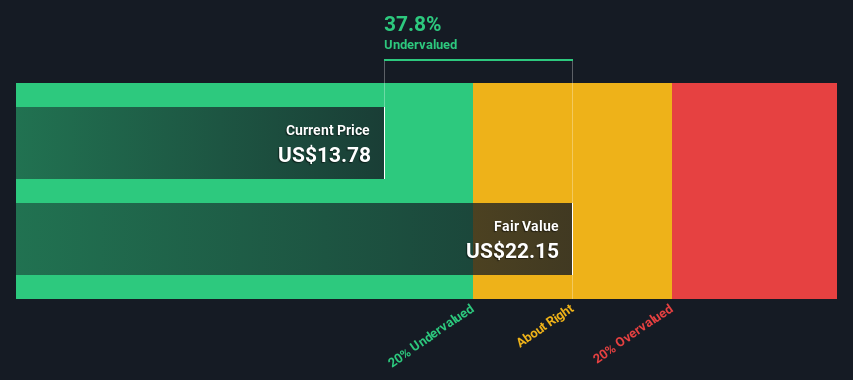

With the shares down over 30% in the past year, trading at US$11.79 and sitting roughly 19% below the current analyst price target, are investors being compensated for the bad news, or is the market already pricing in a rebound?

Preferred P/E of 56x: Is it justified?

On the numbers available, MasterBrand screens as expensive, with a P/E of 56x at a last close of $11.79, compared with both its building industry and peer averages.

The P/E ratio compares the current share price to the company’s earnings per share and, for a manufacturer like MasterBrand, it gives you a quick sense of how much investors are paying for each dollar of earnings. A higher P/E can sometimes reflect expectations for stronger profit growth ahead or a belief that current earnings are temporarily depressed.

Here, the gap is wide. MasterBrand’s 56x P/E sits well above the US building industry average of 23.3x and the peer average of 18.2x. This suggests the shares are pricing in a much richer earnings profile than what the broader group currently carries. With revenue expected to decline by around 0.6% per year over the next three years and profit margins at 1%, this premium raises a clear question about whether the earnings outlook justifies paying more than double the industry multiple.

On top of that, our SWS DCF model points in a different direction. MasterBrand at $11.79 is trading above an estimate of future cash flow value of $4.84. The DCF approach projects future cash flows and discounts them back to today, which can be useful for a business where earnings have been volatile and include one off items, such as the recent $15.2m loss. For a company with declining 5 year earnings, weaker recent margins and interest payments that are not well covered by earnings, it is worth thinking about how much earnings and cash flows would need to improve to justify both a 56x P/E and a price more than double the model’s fair value.

Result: Price-to-Earnings of 56x (OVERVALUED)

However, you still have to weigh the pressure on remodeling and new construction demand, as well as interest costs that current earnings do not comfortably cover.

Another view, cash flows vs earnings

The earnings based view already looks rich at a 56x P/E, but our SWS DCF model adds another layer of concern. On that approach, MasterBrand at $11.79 is trading above an estimate of future cash flow value of $4.84, which points to an overvalued picture rather than a hidden bargain. With earnings declining over 5 years and profit margins at 1%, the question is how much improvement you think is realistic to close that gap.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out MasterBrand for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own MasterBrand Narrative

If you look at these numbers and reach a different conclusion, or you simply prefer to test your own assumptions, you can build a tailored view in just a few minutes, starting with Do it your way.

A great starting point for your MasterBrand research is our analysis highlighting 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, give yourself a chance to spot stronger opportunities by scanning a few focused stock lists that match different approaches to risk and return.

- Target potential value candidates by reviewing our list of 53 high quality undervalued stocks that combine quality fundamentals with more modest pricing.

- Strengthen the core of your portfolio by checking out companies in our solid balance sheet and fundamentals stocks screener (44 results) that put financial resilience front and center.

- Hunt for off the radar opportunities by browsing a screener containing 23 high quality undiscovered gems before everyone else starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.