Mastercard (MA) Stock Valuation After Swipe Fee Settlement And AI Agent Pay Launch

Mastercard MA | 0.00 |

Mastercard (MA) is in focus after two major developments: a preliminary approval of a US$38b swipe fee settlement with merchants, and the launch of Agent Pay for Machines, an AI driven automated payments network.

Despite the recent 2% share price lift around the swipe fee settlement news, Mastercard’s short term share price return is still down year to date, while the 3 year and 5 year total shareholder returns of 32.44% and 37.29% point to a stronger longer term track record.

If you are interested in how payments and AI could reshape markets, this is also a good moment to scan for other opportunities through our curated set of 61 profitable AI stocks that aren't just burning cash.

With the stock down about 13% year to date, yet trading with a premium valuation and an indicated intrinsic discount of roughly 59%, is this weakness pointing to a mispricing, or is the market already baking in Mastercard’s future growth?

Most Popular Narrative: 18% Undervalued

According to a widely followed narrative by andre_santos, Mastercard’s fair value of $595.52 sits well above the last close at $489.98. This frames the current pullback as a potential valuation gap rather than just a sentiment swing.

Mastercard has a wide moat displayed on its stellar operating margin. It also shows solid revenue and EPS growth along with a return on its capital 7-8 times more than its estimated cost of capital.

Curious what supports that higher fair value tag? This narrative leans heavily on durable margins, measured growth in revenue and earnings, and disciplined capital assumptions that do not look overly aggressive on paper.

Result: Fair Value of $595.52 (UNDERVALUED)

However, this story can shift quickly if swipe fee economics tighten more than expected or if AI investments fail to translate into meaningful revenue and profit gains.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Premium P/E Signals a Different Story

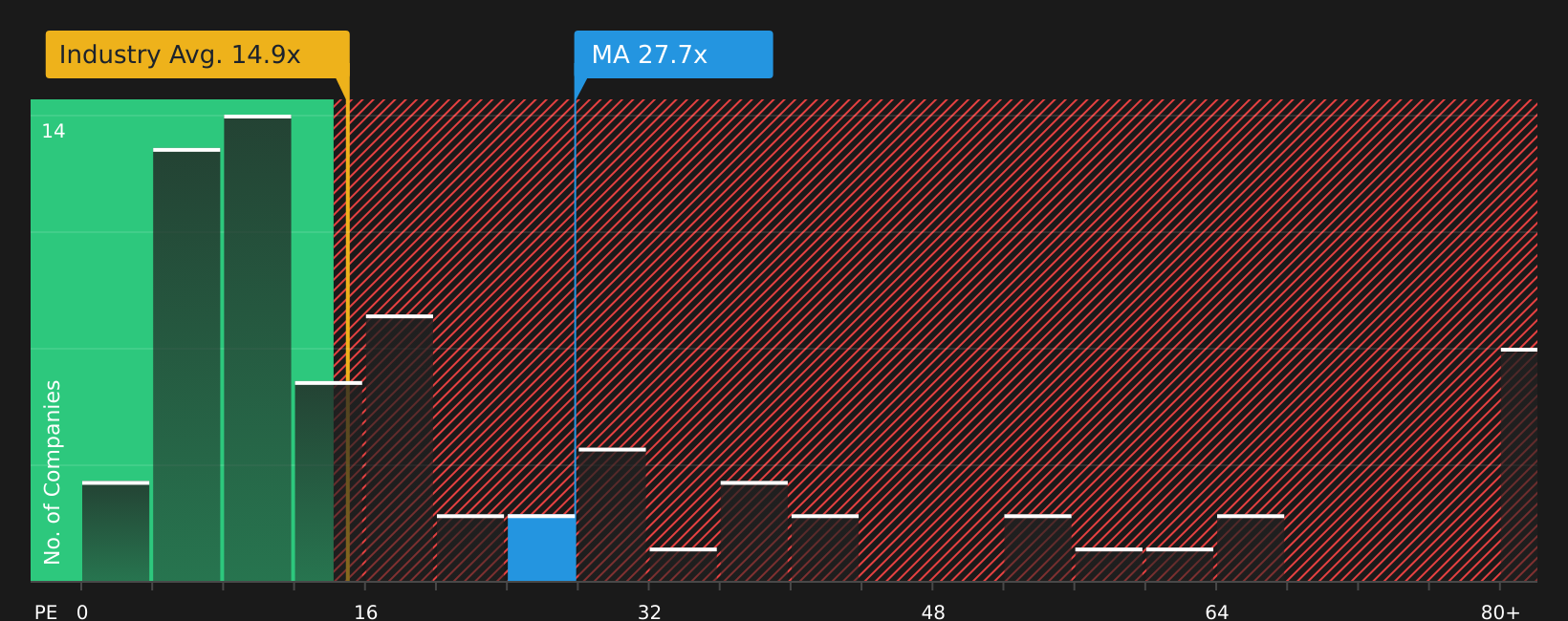

There is a clear tension between the idea of Mastercard trading at a discount to fair value and what the current P/E suggests. The stock trades on 27.8x earnings, compared with 15.1x for the US Diversified Financial industry and 23.9x for peers, while the fair ratio sits lower at 20.8x.

That gap means the market is already paying a higher price for each dollar of Mastercard earnings, which can limit room for error if growth or profitability disappoint. Does this premium reflect lasting strength, or is it extra valuation risk you need to factor in?

Next Steps

With mixed signals on valuation and sentiment, this is a good moment to move quickly, review the numbers yourself, and decide where you stand. To balance the optimism around Mastercard with the concerns that some investors still highlight, check out the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Mastercard no longer feels like the only stock worth your attention, now is the time to broaden your watchlist with a few focused, data driven screens.

- Target stability and income potential by reviewing companies in the 8 dividend fortresses that might better match your risk and yield preferences.

- Hunt for possible mispriced quality by scanning the 44 high quality undervalued stocks and see which stocks the market may not be fully pricing in yet.

- Prioritise resilience by checking the 71 resilient stocks with low risk scores and avoid missing stocks that could offer a smoother ride when volatility picks up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.