Merck (MRK) Stock After 64% One-Year Rally And Terns Deal Is It Priced Fairly?

Merck & Co., Inc. MRK | 0.00 |

- If you are wondering whether Merck at US$125.45 still offers value after its strong run, this article explains what the current price may be implying about the stock.

- Merck's share price performance has been strong recently, with returns of 10.2% over the past 7 days, 4.8% over the past 30 days, 17.8% year to date, 64.5% over 1 year, 21.2% over 3 years and 88.0% over 5 years.

- Recent coverage of Merck has focused on its position in the pharmaceuticals space and how investors are reacting to its pipeline and product portfolio. This backdrop helps explain why some market participants are reassessing what they are willing to pay for the stock.

- On Simply Wall St's valuation checks, Merck currently has a value score of 2 out of 6. The next sections unpack what different valuation methods say about that score and introduce an additional way to assess value at the end of the article.

Merck scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

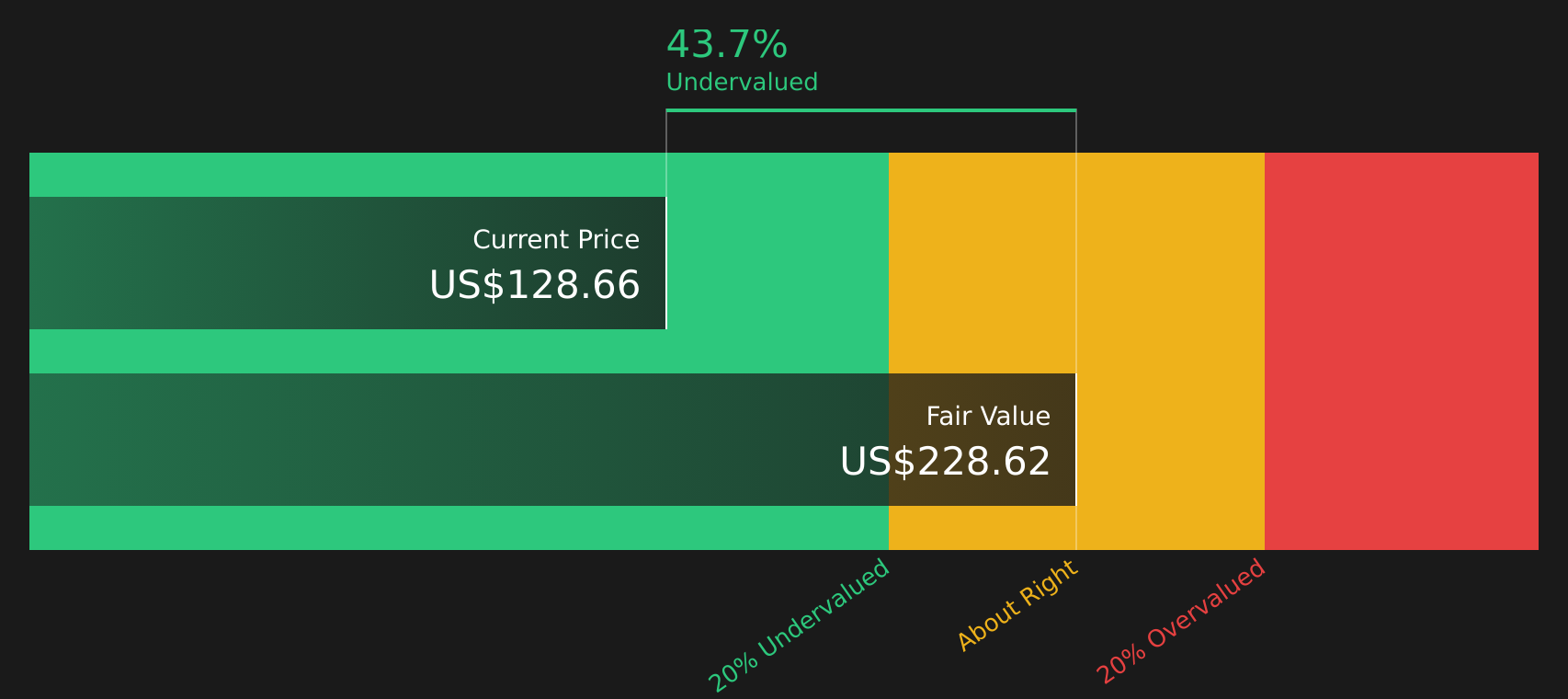

Approach 1: Merck Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what Merck stock could be worth today by projecting future cash flows and then discounting those cash flows back to a present value using a required return.

For Merck, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $14.0b. Analysts provide explicit forecasts for the next few years, and Simply Wall St then extrapolates those forecasts out to 2035. Within these projections, free cash flow is expected to be $24.6b in 2030, based on a mix of analyst estimates and modelled growth rates.

Bringing all those projected cash flows back to today produces an estimated intrinsic value of $228.62 per share for Merck. Compared with the current share price of $125.45, this DCF output indicates an implied discount of 45.1%, which suggests the stock is trading below this model’s estimate of fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Merck is undervalued by 45.1%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Approach 2: Merck Price vs Earnings

For a profitable company like Merck, the P/E ratio is a useful way to relate what you pay for the stock to the earnings it currently generates. Investors typically accept higher P/E ratios when they expect stronger earnings growth or see lower risk, and look for lower P/E ratios when growth expectations are modest or risks feel higher.

Merck currently trades on a P/E of 34.68x. This is above the Pharmaceuticals industry average P/E of 14.73x and also above the peer group average of 25.35x. On the surface, that suggests the market is assigning a higher price to each dollar of Merck's earnings compared with many other companies in its sector.

Simply Wall St’s Fair Ratio for Merck is 33.84x. This is a proprietary estimate of what Merck's P/E might reasonably be, considering factors such as its earnings growth profile, profit margins, industry, market cap and key risks. Because it blends these company specific inputs, the Fair Ratio can give a more tailored yardstick than a simple comparison against broad industry or peer averages.

Comparing the Fair Ratio of 33.84x with the current P/E of 34.68x suggests Merck is slightly above this tailored estimate, which points to the stock being priced a bit higher than the Fair Ratio implies.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Merck Narrative

Earlier it was mentioned that there is an even better way to understand Merck's valuation. Narratives are simply your own story about the company that ties together your assumptions for future revenue, earnings and margins with an estimated fair value.

On Simply Wall St's Community page, Narratives give you a straightforward tool used by millions of investors to connect the qualitative story you believe about Merck with a set of financial forecasts and a resulting fair value. You can then compare this directly with the current share price to help decide whether the stock looks cheap or expensive to you.

Because Narratives update automatically when new information such as earnings, news or regulatory developments is added to the platform, your Merck view does not stay static. You can quickly see how fresh data affects your fair value versus price gap.

For example, one Merck Narrative on the bearish end currently anchors to a fair value of about US$101.68 per share and places more weight on pricing pressure and patent risk. A more optimistic Narrative aligns with a fair value of about US$150.00 per share and focuses on the oncology pipeline and deals like Terns. Comparing where you sit on that spectrum is a practical way to choose the Merck Narrative that fits your own expectations.

For Merck, however, we will make it really easy for you with previews of two leading Merck Narratives:

Fair value: US$129.74 per share

Implied discount to this narrative: 3.3% below fair value

Revenue growth assumption: 5.15%

- Focuses on Merck's oncology pipeline and the Terns Pharmaceuticals deal as key drivers of future earnings, supported by more than 20 potential new growth assets and a larger late stage pipeline.

- Assumes rising profit margins and steady share count reduction, with a 2029 outcome that would align with analysts' consensus price target if Merck trades on a P/E of 16.1x.

- Flags risks around weaker GARDASIL demand in China, possible tariffs, competition, loss of exclusivity for KEYTRUDA and pricing pressure across major markets.

Fair value: US$101.68 per share

Implied premium to this narrative: 23.4% above fair value

Revenue growth assumption: 3.00%

- Frames Merck as more dependent on a small group of flagship drugs, with pricing pressure, generics, biosimilars and regulation seen as important headwinds for revenue and margins.

- Builds in lower revenue growth than the bullish case and a future P/E of 13.3x, which pulls the fair value estimate toward the lower end of the analyst target range.

- Points out that execution and bidding risk around the Terns acquisition, together with study outcomes and legal exposure, could limit how much upside investors are willing to pay for Merck at today's price.

Once you have a sense of which story feels closer to your own view, you can use Narratives as a starting point and then adjust the key inputs to reflect your expectations for Merck's earnings, margins, risks and, eventually, what you think a fair price per share looks like.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Merck on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Merck? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.