Morgan Stanley’s 2026 Playbook: Top Sectors, Themes and Stock Picks to Track Now

NVIDIA Corporation NVDA | 0.00 | |

Microsoft Corporation MSFT | 0.00 | |

Apple Inc. AAPL | 0.00 | |

Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR TSM | 0.00 | |

Constellation Energy Corporation CEGVV | 0.00 |

In its April 2026 update to the year-ahead outlook, Morgan Stanley highlights four dominant forces shaping markets: surging AI compute demand, valuation dispersion driven by AI replicability, a global push for self-sufficiency, and evolving energy geopolitics. The firm reaffirms a four-pillar framework—AI & technology diffusion, the future of energy, a multipolar world, and societal change—and outlines sector rotation and stock ideas.

Core Takeaway: From “AI Everything” to Scarcity & Sovereignty

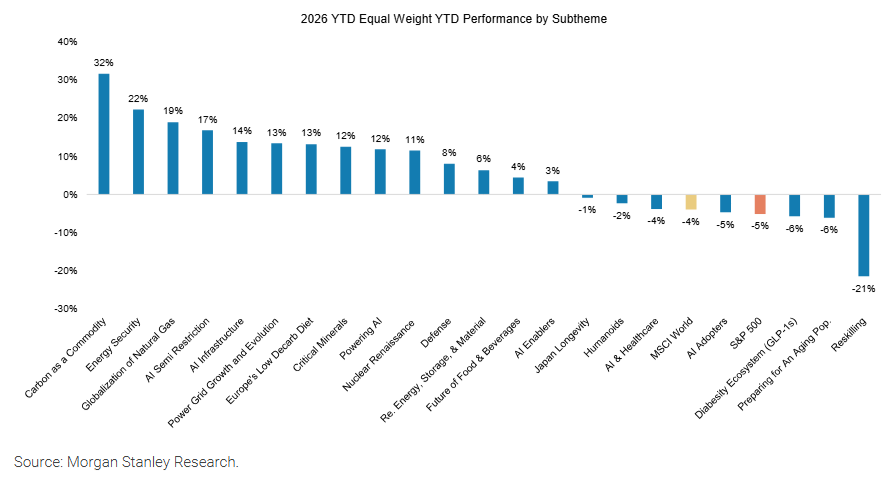

Morgan Stanley’s thematic strategy has continued to generate alpha in volatile markets. Thematic baskets rose 38% in 2025 (outperforming the S&P 500 by 27ppt) and are up ~7% YTD 2026 (beating by 12ppt).

The market focus is shifting from broad AI exposure to two asset types:

Scarce assets: hard-to-replicate physical assets and companies with pricing power

Sovereign/strategic assets: defense, critical minerals, domestic energy

Four-pillar Framework In-depth Analysis

1) AI & Technology Diffusion: Compute Shortage Is the Bottleneck

View: Frontier LLM capabilities in the U.S. are accelerating, while Chinese developers continue to compress application costs. Demand for compute is rising far faster than supply.

Evidence: Token usage for agentic AI has surged; industry commentary suggests compute needs could double every ~6 months.

Implications:

Favor bottleneck solvers: chip supply chain, memory, and data-center essentials (transformers, storage, backup power, construction labor)

Favor “compute merchants” (large cloud providers)

Enterprise AI likely scales before consumer use cases

Themes: AI infrastructure, energy for AI, AI + healthcare

2) The Future of Energy: AI Demand Meets Geopolitics

View: AI infrastructure is driving a step-change in global power demand; energy independence is becoming strategic.

Evidence: U.S. data centers may face 20–30% power shortfalls (2025–2028). AI operators are paying significant premiums for reliable electricity.

Implications:

Favor off-grid/dispatchable solutions: fuel cells, turbines, storage

Favor energy independence enablers: nuclear, renewables, grid optimization, storage

Themes: Energy security, nuclear revival, LNG/global gas, clean energy & storage, Europe’s transition, energy for AI

3) A Multipolar World: Defense & Supply Chains Rewire

View: Nations are reducing dependence in energy, security, and technology. Industrial policy is intensifying; reshoring accelerates.

Evidence: Defense spending is rising globally, targeting drones/counter-drone, electronic warfare, cyber, directed energy, and space. Critical minerals are strategic priorities.

Implications:

Favor defense, especially next-gen capabilities

Favor critical minerals and onshoring beneficiaries

Themes: Defense, critical minerals, AI semiconductor restrictions

4) Societal Change: Longevity, Healthcare & AI’s Labor Impact

View: AI may be deflationary for many services, widen wage dispersion, and increase the value of non-replicable assets. Aging and AI disruption will drive policy and reskilling needs.

Evidence: Rapid growth in GLP-1 drugs (e.g., Semaglutide, Tirzepatide) with peak market estimates raised to ~$150bn. AI + healthcare (drug discovery, smart therapies) is accelerating. “Reskilling” has lagged YTD amid fears AI disrupts education/training.

Implications:

Favor AI adopters with pricing power and defensible moats

Favor healthcare innovation (GLP-1 ecosystem, AI + healthcare, aging)

Be selective on reskilling/education models

Themes: Diabetes/obesity ecosystem (GLP-1), AI + healthcare, aging, longevity, reskilling

Positioning: Selective Rotation to Five Areas

With energy and AI infrastructure already strong YTD, Morgan Stanley suggests rotating toward segments with higher upside or strategic importance:

Defense (~16% median upside)

Healthcare: AI + healthcare (~28%), aging (~26%), diabetes/obesity (~24%)

AI adopters with pricing power (~21%)

AI infrastructure & enabling energy (~15%)

Humanoid robotics (~22%), reflecting the next phase of embodied AI

Stock to Watch

AI Infrastructure & Energy for AI

- NVIDIA Corporation(NVDA.US)

- Microsoft Corporation(MSFT.US)

- Apple Inc.(AAPL.US)

- Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR(TSM.US)

- Samsung Electronics

- Constellation Energy Corporation(CEGVV.US)

- Vistra Corp.(VST.US)

Global Defense

General Dynamics Corporation(GD.US)

RAYTHEON TECHNOLOGIES CORPORATION(RTX.US)

Lockheed Martin Corporation(LMT.US)

Humanoid Robotics

Microsoft Corporation(MSFT.US)

Samsung Electronics

AI Adopters with Pricing Power

Microsoft Corporation(MSFT.US)

Intuitive Surgical, Inc.(ISRG.US)

Risks

Outcomes depend on AI development speed, macro conditions, geopolitics, and policy. Any sharp shift in these variables could materially alter the investment path.

Source: Morgan Stanley, “Revisiting Our 10 Thematic Predictions” (edited and condensed; not investment advice).